|

|

|

|

|||||

|

|

|

Inspire Medical Systems INSP is well poised for growth in the coming quarters amid a major product transition. Management emphasized clinical momentum behind Inspire V, improving reimbursement visibility, and disciplined cost control, while acknowledging near-term headwinds tied to inventory conversion, GLP-1 dynamics, and competitive and operational complexities.

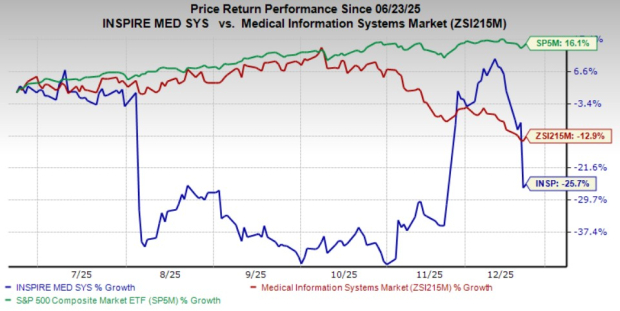

Shares of this Zacks Rank #3 (Hold) company have lost 12.5% over the past six months compared with the industry’s 16.3% decline. The S&P 500 Index has increased 16.3% in the same time frame.

Inspire Medical, a medical technology company focused on the development and commercialization of innovative, minimally-invasive solutions for patients with obstructive sleep apnea, has a market capitalization of $2.81 billion. The company projects a 39.1% earnings decline for the fourth quarter of 2025. However, earnings are expected to return to growth in 2026.

Its earnings surpassed estimates in each of the trailing four quarters, delivering an average surprise of 164.19%.

Strong Inspire V Clinical Performance and Adoption Momentum: The Inspire V launch is emerging as a structural growth driver. Management cited compelling clinical data, including reduced surgical times, high nightly usage, and strong synchronization with patient breathing, reinforcing superior outcomes versus prior generations. With physician training nearing completion and contracting above 90%, adoption of Inspire V has accelerated, reaching more than 75% of implanting centers. Importantly, early evidence shows higher utilization and efficiency at converted centers, with surgeons able to perform more implants per day. This combination of better outcomes, easier implantation, and higher throughput underpins sustained volume growth.

Favorable Reimbursement Outlook Supports Economics: Reimbursement trends are becoming a tailwind. CMS finalized an 11% increase in the physician fee schedule for CPT 64568 effective January 2026, while proposed increases to hospital outpatient and ASC reimbursement further improve site-of-care economics. Coverage already extends to more than 90% of covered lives, including Medicare. These changes should narrow historical reimbursement gaps between Inspire systems and reduce friction for hospital adoption. Improved reimbursement visibility strengthens Inspire V’s value proposition, supports center-level profitability, and should accelerate broader conversion and utilization over time.

Expanding Patient Funnel and Disciplined Execution: Management highlighted that GLP-1 adoption is increasing patient flow into sleep clinics, expanding the top of the funnel for Inspire Medical rather than displacing demand. Sleep physicians increasingly manage GLP-1 patients alongside CPAP, creating a pathway for Inspire Medical referrals as noncompliance emerges or BMI thresholds are met.

Concurrently, Inspire Medical demonstrated operational discipline, delivering earnings upside through gross margin expansion and cost control despite higher marketing spend. Strong cash generation, share repurchases, and tighter territory management position the company to scale profitably as volume growth resumes.

Inspire IV to V Inventory Transition Complexity: The ongoing transition from Inspire IV to Inspire V introduces near-term noise. Some centers will continue using Inspire IV for economic reasons, while international markets still require Inspire IV inventory pending regulatory approvals for Inspire V. This dual-track approach elevates finished goods inventory and complicates forecasting. Management acknowledged potential temporary headwinds from destocking and restocking dynamics, even if implant volumes broadly track revenues. While the transition appears largely complete in the United States, inventory normalization and full global conversion remain execution risks into 2026.

GLP-1 Trialing and Timing Uncertainty: Although management views GLP-1 therapies as complementary over the long term, near-term trialing introduces uncertainty around procedure timing. Patients may delay surgical intervention while attempting pharmacologic weight loss, potentially dampening short-term volume growth. Management’s early-2026 growth outlook reflects prudence around this dynamic. While increased clinic visits and eventual CPAP noncompliance could ultimately benefit Inspire Medical, the pace at which GLP-1 patients convert to hypoglossal nerve stimulation remains difficult to predict, creating variability in near-term demand visibility.

Margin Pressure From Elevated OpEx and Competition: Despite strong gross margins, operating leverage remains constrained by elevated operating expenses, particularly patient marketing and launch-related investments. Year-over-year operating expenses growth continues to outpace revenues, while non-recurring items weighed on reported profitability. Additionally, management acknowledged emerging competitive activity, albeit limited today, and ongoing pricing and site-of-service considerations at certain centers. Sustaining margin expansion will require a careful balance between growth investments and efficiency gains as revenue growth moderates to a low double-digit trajectory.

Inspire Medical Systems, Inc. price | Inspire Medical Systems, Inc. Quote

Inspire Medical is witnessing a stable estimate revision trend for 2025. In the past 30 days, the Zacks Consensus Estimate for earnings is pegged at $1.71 per share.

The Zacks Consensus Estimate for fourth-quarter 2025 revenues and loss per share is pegged at $262.9 million and 70 cents, respectively.

Some better-ranked stocks in the broader medical space that have announced quarterly results are Medpace Holdings, Inc. MEDP, CareCloud CCLD and KORU Medical Systems KRMD.

Medpace Holdings, currently carrying a Zacks Rank #2 (Buy), reported second-quarter 2025 EPS of $3.10, which beat the Zacks Consensus Estimate by 3.3%. Revenues of $603.3 million outpaced the consensus mark by 11.5%. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Medpace Holdings has a long-term estimated growth rate of 11.4%. MEDP’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 13.9%.

CareCloud reported third-quarter 2025 adjusted EPS of 10 cents, which beat the Zacks Consensus Estimate by 25%. Revenues of $31 million surpassed the Zacks Consensus Estimate by 8.3%. It currently carries a Zacks Rank of 2.

CareCloud has an estimated growth rate of 20% for 2025. CCLD’s earnings surpassed estimates in two of the trailing four quarters and missed twice, the average negative surprise being 2.88%.

KORU Medical Systems reported third-quarter 2025 adjusted loss per share of 2 cents, which outpaced the Zacks Consensus Estimate by 33.3%. Revenues of $10 million surpassed the Zacks Consensus Estimate by 7.1%. It currently carries a Zacks Rank #2.

KORU Medical Systems has an estimated growth rate of 83.3% for 2026. KRMD’s earnings surpassed estimates in two of the trailing four quarters, missed once and met in the other, the average surprise being 20.83%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-03 | |

| Aug-03 | |

| Jul-29 | |

| Jul-28 | |

| Jul-27 | |

| Jul-23 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite