|

|

|

|

|||||

|

|

|

Altria Group, Inc. (MO) recently made a notable move in its capital allocation strategy, with its management authorizing an expansion of the existing share repurchase program from $1 billion to $2 billion. This 100% increase, which extends the program's expiration to Dec. 31, 2026, signals a significant ramp-up in the company’s commitment to returning value to shareholders.

The decision follows an active period of buybacks in 2025. During the third quarter of 2025, Altria repurchased 1.9 million shares at an average price of $60.13, spending $112 million. Through the first nine months of 2025, the company bought back 12.3 million shares at an average price of $58.08 for a total outlay of $712 million. Against this backdrop, the expanded authorization signals that management expects repurchases to remain a meaningful use of cash well into 2026.

The structure of the expanded program suggests a steady approach rather than an aggressive short-term bet. By spreading repurchases through late 2026, Altria preserves discretion over timing while reinforcing buybacks as a central pillar of its capital return framework.

The expanded buyback may help offset modest earnings per share pressure as cigarette volume declines persist and the impact of prior share reductions moderates. At the same time, it reflects confidence in Altria’s steady cash generation and disciplined capital allocation. Overall, the move underscores the continued role of the core combustibles business in supporting shareholder returns as the company advances its smoke-free portfolio.

Philip Morris International Inc. (PM) is currently prioritizing debt reduction over equity repurchases. Specifically, Philip Morris has stated it expects no share repurchases in 2025 as it targets a net debt to adjusted EBITDA ratio of approximately 2x by the end of 2026. This strategy by Philip Morris reflects an emphasis on balance sheet strength as it advances its global “smoke-free” expansion.

Turning Point Brands, Inc. (TPB) is maintaining a flexible approach to capital allocation. Turning Point Brands announced plans to amend its buyback authorization and ATM prospectus supplement to provide $200 million of capacity under each program, consistent with its policy of keeping active authorizations in place to enhance capital markets flexibility. While Turning Point Brands has no immediate plans to execute repurchases, the authorization provides flexibility around future capital return decisions.

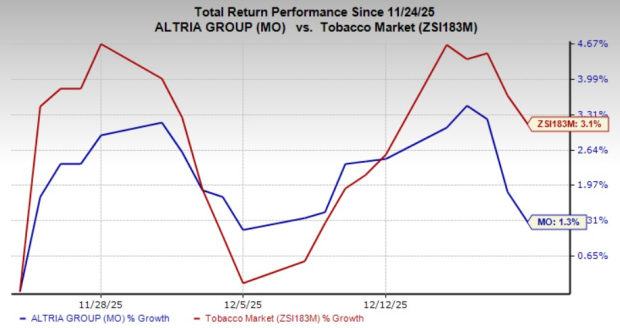

Shares of Altria have gained 1.3% in the past month compared with the industry’s growth of 3.1%.

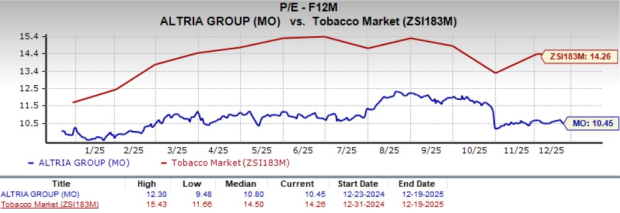

From a valuation standpoint, MO trades at a forward price-to-earnings ratio of 10.45X, down from the industry’s average of 14.26X.

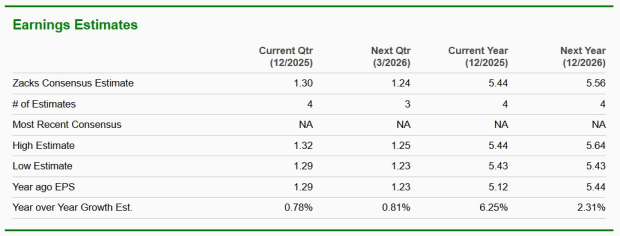

The Zacks Consensus Estimate for MO’s 2025 and 2026 earnings implies year-over-year growth of 6.3% and 2.3%, respectively.

Altria currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite