|

|

|

|

|||||

|

|

|

Responding to signs of slowing economic activity and easing inflation pressures, the Federal Reserve shifted its monetary stance in 2025 by starting to cut interest rates. At its December meeting, the Fed lowered the federal funds target range by another 25 basis points (bps) to 3.50-3.75%, marking its third consecutive rate reduction this year, a move aimed to support economic expansion while keeping inflation trends aligned with the 2% objective.

Looking to 2026, while expectations are mixed, they broadly suggest moderate easing over the course of the year. Fed officials have signaled that future moves will remain highly dependent on incoming economic data.

Either way, the banking industry is poised to benefit from falling interest rates in the coming quarters, with banks like Wells Fargo WFC, Bank of America BAC and Citigroup C likely to gain the most.

Banks generally benefit from falling interest rates as lower borrowing costs tend to stimulate loan demand across consumer and commercial segments. When rates decline, households are more likely to take out mortgages, refinance existing loans and increase spending financed through credit cards or personal loans. Businesses also become more willing to borrow for expansion, inventory and capital investment. This pickup in lending activity helps banks grow loan volumes, which can offset some of the pressure that lower rates place on net interest margin (NIM).

Lower interest rates can also improve credit quality, which is a key positive for bank profitability. As debt servicing costs fall, borrowers find it easier to meet their obligations, reducing the risk of delinquencies and defaults. This results in lower provisions for loan losses and fewer charge-offs, directly supporting earnings. A more stable credit environment thus allows banks to deploy capital more confidently and focus on growth rather than balance-sheet defense.

Additionally, falling rates boost fee-based and market-related income streams for banks. Capital markets activity tends to improve as lower rates encourage debt issuance, refinancing and merger and acquisition activity, benefiting investment banking (IB), trading and advisory businesses. Wealth management and asset management divisions can also gain from stronger market performance and higher client activity.

To sum up, stronger loan growth, healthier credit conditions and increased fee income position banks to perform better in a declining interest rate environment.

Wells Fargo: The company has signaled that interest rate cuts will help stabilize funding costs, making deposit growth a central pillar of its balance sheet strategy. Since lower rates spur loan demand, WFC aims to aggressively grow both consumer and corporate loan assets now that it has been freed from its asset cap. Management expects 2025 net interest income (NII) to be stable year over year, as lower rates support a rebound in loan origination and reduce deposit pricing pressures.

WFC plans to leverage its expanded balance sheet to grow fee-rich franchises (IB, trading, wealth management and payments). This diversification is essential in a rate-cutting cycle, when NIM and NII may face pressure.

Wells Fargo's approach in a declining rate environment is to prioritize organic growth, compete more aggressively for deposits and selectively increase lending while remaining cautious during periods of heightened economic uncertainty. Thus, the bank is expected to see improved profitability and margin resilience as monetary conditions ease.

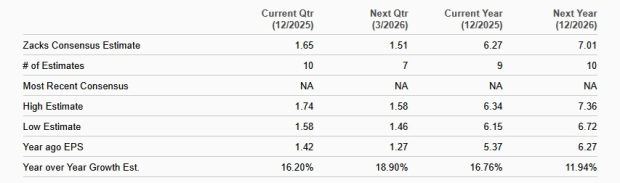

The Zacks Consensus Estimate for WFC’s 2025 and 2026 earnings implies year-over-year growth rates of 16.8% and 11.9%, respectively. Currently, the company carries a Zacks Rank #3 (Hold).

Bank of America: The company, one of the most rate-sensitive banks in the country, is poised to benefit from fixed-rate asset repricing, higher loan and deposit balances and a gradual fall in funding costs. As rates come down, it will boost lending activity. Also, easing regulatory capital requirements will help channel excess capital into loan growth, particularly within resilient commercial and consumer segments. Management expects the bank’s NII to grow 5-7% in 2026, after similar growth this year.

BAC is prioritizing organic, domestic growth through the expansion of its physical and digital presence. The company has laid out an ambitious medium-term plan centered on sustainable growth, digital scale, cost discipline and capital efficiency.

It plans to expand its financial center network and open more than 150 centers by 2027, which, along with the growing adoption of digital tools, will support NII growth and expand cross-sell opportunities.

Over the next three to five years, BAC aims to deliver more than 12% of earnings growth and a return on tangible common equity (ROTCE) between 16% and 18%, while maintaining a Common Equity Tier 1 ratio of 10.5%.

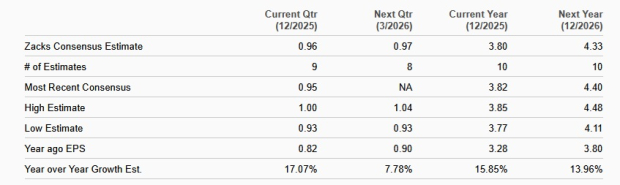

The Zacks Consensus Estimate for BAC’s 2025 and 2026 earnings suggests year-over-year increases of 15.9% and 14%, respectively. The company carries a Zacks Rank #3 at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Citigroup: Improvement in NII has been supporting the company’s top-line growth over the years. The metric witnessed a three-year (ended 2024) compound annual growth rate (CAGR) of 8.4%, with the momentum continuing in the first nine months of 2025. NII is expected to continue expanding on the back of stabilizing funding costs and loan growth. Management projects 2025 NII to rise 5.5% year over year.

Citigroup continues to emphasize growth in core businesses through streamlining consumer banking operations globally. The company has successfully exited from consumer banking businesses in nine countries. These initiatives will free up capital and help the company pursue investments in wealth management and IB operations, which will stoke fee income growth.

Management expects total revenues to exceed $84 billion in 2025, with revenues projected to see a 4-5% CAGR through 2026.

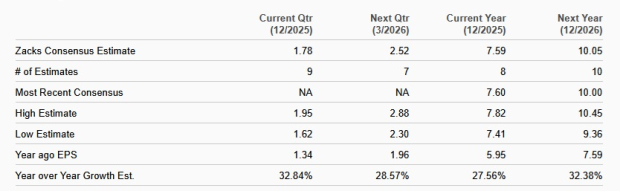

The Zacks Consensus Estimate for Citigroup’s 2025 and 2026 earnings indicate year-over-year growth of 27.6% and 32.4%, respectively. It also carries a Zacks Rank of 3 at present.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 4 hours | |

| Jul-05 | |

| Jul-05 | |

| Jul-05 | |

| Jul-05 | |

| Jul-04 | |

| Jul-04 | |

| Jul-04 | |

| Jul-03 | |

| Jul-03 | |

| Jul-03 | |

| Jul-02 | |

| Jul-02 | |

| Jul-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite