|

|

|

|

|||||

|

|

|

In a market increasingly shaped by artificial intelligence (AI) and digital lending platforms, investors are closely watching companies that sit at the intersection of technology and consumer finance. Pagaya Technologies Ltd. PGY and LendingTree, Inc. TREE both play pivotal roles in this ecosystem, but their business models and risk profiles differ meaningfully.

While Pagaya’s primary focus is leveraging AI and machine learning to optimize credit underwriting and diversify funding sources, LendingTree operates a more traditional online lending marketplace to monetize borrower-lender connections.

Now, let us understand how PGY’s AI-powered growth momentum competes with TREE’s proven marketplace supremacy. Comparing the fundamentals of the two stocks will help us determine which stock offers the more compelling risk-reward setup heading into the next phase of the fintech cycle.

With an adaptable business model and capital-efficient structure, PGY, which initially focused on personal loans, has expanded into auto lending and point-of-sale financing over time. This helped the company reduce exposure to any single loan type and improve resilience across economic cycles.

To diversify its funding, PGY has built a network of more than 135 institutional partners and utilizes forward flow agreements — pre-arranged deals in which investors commit to buying future loans. These agreements offer funding stability, especially during market disruptions.

After a challenging period in the last couple of years, Pagaya hit an inflection point in 2025 with improving fundamentals and profitability. Despite macroeconomic headwinds and regulatory risks, the company posted three consecutive quarters of positive GAAP net income this year, a dramatic turnaround from substantial losses in the previous years. In the nine months ended Sept. 30, 2025, its year-over-year network volume growth was 10.5%, a trend the company is expected to sustain in the near term. For 2025, PGY expects network volume of $10.5-$10.75 billion.

A key differentiator for Pagaya is its proprietary tech and product suite. Its pre-screen solution allows lenders to present pre-approved offers to existing customers without formal applications, helping partners boost credit access and deepen relationships with minimal marketing spend.

Additionally, Pagaya operates with minimal on-balance-sheet exposure. Loans are typically acquired immediately by asset-backed securities (ABS) vehicles or via forward flow agreements, thanks to capital raised in advance. This approach limits credit and market risks, preserving flexibility during turbulent environments. This model proved effective from 2021 to 2023 amid rising rates and tighter markets. By relying on forward flow agreements and strategic ABS issuance, Pagaya maintained liquidity and minimized loan write-downs.

TREE is a key player in the growing digital lending space. It is an online marketplace that connects consumers with financial service providers for mortgages, loans, credit cards and insurance. The company’s operating strategy has been evolving, with a notable shift in focus toward boosting the top line by diversifying into non-mortgage products, particularly in the consumer segment.

Over the years, TREE has expanded its services to include credit cards and widened its loan offerings by providing personal, auto, small business and student loans. LendingTree entered the branded credit market in 2023 with the launch of the WinCard, its first consumer credit product, in partnership with Upgrade. The company’s initiatives, including SPRING (previously MyLendingTree) and TreeQual, are bolstering its cross-selling opportunities.

LendingTree has also been leveraging data and technology to augment user experience and monetization. The company’s investment in EarnUp (in early 2022), a consumer-facing payments platform, demonstrates its commitment to building a more comprehensive, tech-enabled ecosystem for financial health management.

TREE intends to continue adding offerings for consumers, small businesses and network partners to its online marketplace to expand and diversify its revenue sources. Over the past three years, the company’s non-mortgage revenue streams have witnessed a compound annual growth rate of 3.3%.

In third-quarter 2025, LendingTree’s adjusted EBITDA increased 48% year over year, fueled by strong revenue growth across all three business segments. For 2025, adjusted EBITDA is projected to be $126-$128 million, up from the prior stated $119-$126 million. Total revenues are expected between $1.08 billion and $1.09 billion, up from the previously mentioned $1-$1.05 billion.

In the past six months, shares of Pagaya have gained 6.3%, whereas the TREE stock has jumped 46.5%. Hence, in terms of investor sentiments, TREE has the edge.

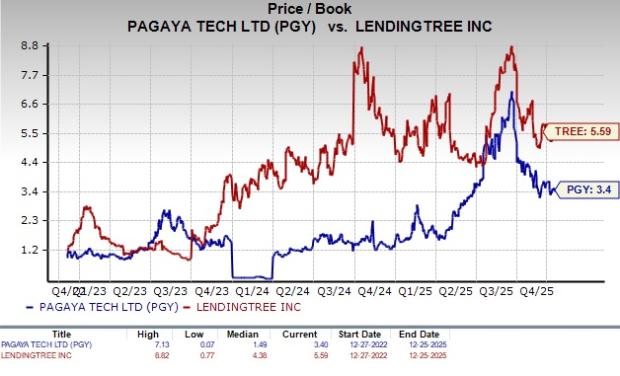

From a valuation perspective, Pagaya is currently trading at a 12-month trailing price-to-book (P/B) of 3.40X, which is below TREE’s current trailing 12-month P/B of 5.59X.

Thus, currently, the PGY stock is inexpensive compared with LendingTree.

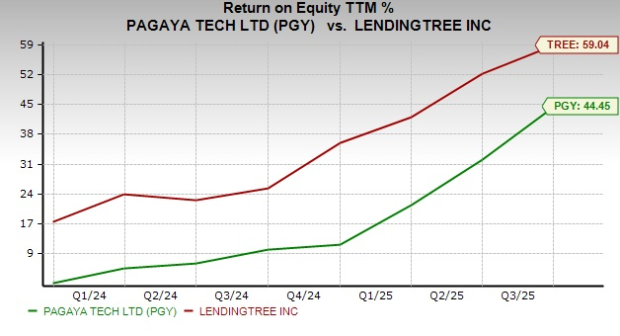

Pagaya’s return on equity (ROE) of 44.45% is below LendingTree’s 59.04%. This reflects that TREE is more efficiently using shareholder funds to generate profits compared with PGY.

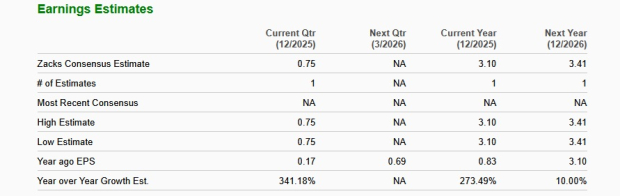

The Zacks Consensus Estimate for PGY’s 2025 and 2026 revenues is pegged at $1.32 billion and $1.57 billion, respectively, implying year-over-year growth rates of 28.4% and 19.2%.

The consensus estimate for PGY’s earnings for 2025 and 2026 indicates year-over-year growth of 273.5% and 10%, respectively.

On the contrary, the Zacks Consensus Estimate for TREE’s 2025 and 2026 revenues is pegged at $1.08 billion and $1.15 billion, implying year-over-year growth rates of 20.5% and 5.7%, respectively.

Also, the consensus estimate for LendingTree’s earnings indicates 50.2% year-over-year growth for 2025 and 5.7% growth for 2026.

PGY is a profitable fintech leader with fast-growing revenues, an impressive yearly performance, a resilient business model, a capital-efficient funding strategy and strong institutional support. Its AI-driven platform, diversified revenue streams and reliance on forward flow agreements shield it from market volatility and credit risks.

Alternatively, TREE boasts a well-established marketplace model and an ROE that is superior to PGY. Its focus on non-mortgage product offerings will continue to support revenue growth. Also, its cost-control efforts are expected to aid profitability.

While LendingTree has relative operational maturity and stability, PGY has a significantly stronger revenue and earnings growth outlook, along with a better valuation.

Currently, PGY carries a Zacks Rank #2 (Buy) and LendingTree sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 3 hours | |

| Aug-03 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-27 | |

| Jul-23 | |

| Jul-21 | |

| Jul-20 | |

| Jul-16 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite