|

|

|

|

|||||

|

|

|

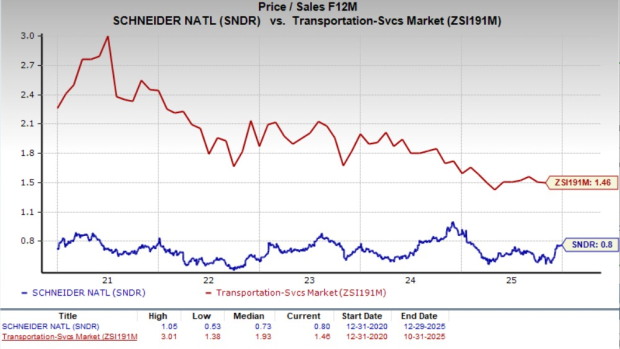

Schneider National, Inc. (SNDR) looks cheap from a valuation standpoint. Considering the forward 12-month price-to-sales ratio (P/S-F12M), Schneider is trading at a discount compared to the industry.

The stock has a forward 12-month P/S-F12M of 0.80X compared with 1.46X for the industry over the past five years. These factors indicate that the stock’s valuation is attractive. Schneider has a Value Score of B.

Now, the question is whether it is worth buying, holding, or selling the Schneider stock at current prices. Let us delve deeper to find out.

Schneider continues to witness a decline in capital expenditures owing to reduced purchases of transportation equipment. During 2024, SNDR incurred net capital expenditures of $380.3 million compared with $573.8 million at the end of 2023. Further, SNDR has reduced its capital expenditure guidance for 2025. The company now expects its 2025 net capital expenditures to be around $300 million, down from the prior guided range of $325-$375 million. Declining capital expenditures bode well for the company's bottom-line growth.

Schneider’s solid balance sheet increases financial flexibility. The company ended third-quarter 2025 with cash and cash equivalents of $194.1 million, higher than the current debt level of $12.4 million. This implies that the company has sufficient cash to meet its current debt obligations. Further, SNDR’s current ratio (a measure of liquidity) at the end of third-quarter 2025 stood at 2.11, which is higher than second-quarter 2024's reading of 1.91, as well as the industry’s figure of 1.28. The favorable comparison with respect to the current ratio looks encouraging. This may imply that the risk of default is less. Also, a current ratio greater than 1.5 is usually considered good for a company.

A strong balance sheet enables the company to reward shareholders with dividends and share repurchases. As a reflection of its shareholder-friendly stance, in 2022, 2023 and 2024, SNDR paid dividends of $55.7 million, $63.6 million and $66.6 million, respectively. As of Sept. 30, 2025, SNDR had returned $50.3 million in the form of dividends to shareholders year to date. Dividend-paying stocks like SNDR are generally safe bets for creating wealth, as these payouts act as a hedge against economic uncertainty, which characterizes current times.

SNDR is also active on the buyback front. In February 2023, SNDR announced the approval of a three-year $150 million share repurchase program. As of Sept. 30, 2025, SNDR had repurchased a total of 4.1 million Class B shares for $103.9 million under the program. Buybacks not only reduce the total outstanding share count, thereby increasing earnings per share, but also signal management's belief in the intrinsic value of the stock. Such shareholder-friendly moves instill investor confidence and positively impact the company's bottom line.

Shares of Schneider have gained 31.2% over the past three months, outperforming the transportation-services industry’s 7.8% increase, as well as that of other industry players, Expeditors International of Washington, Inc. (EXPD) and C.H. Robinson Worldwide, Inc. (CHRW).

Schneider has reduced its 2025 adjusted earnings per share guidance to approximately 70 cents from the prior guidance of 75-95 cents. The adverse effect of insurance-related costs (related to prior-year claims) has led to Schneider’s full-year tempered earnings outlook.

Macroeconomic uncertainty continues to remain an overhang. The company's bottom line is significantly affected by the ongoing inflationary environment and supply-chain disruptions, which are driving up overall costs, particularly in the insurance domain, and directly impacting operating expenses. Increased insurance expense and weakness in the freight market continue to hurt SNDR’s prospects.

Schneider's logistics segment revenues continue to get hurt by lower brokerage volume, despite the benefits of the Cowan Systems acquisition. Market volatility and rising costs continue to challenge SNDR, potentially impacting its growth and earnings in the near term.

What Do Earnings Estimates Say for Schneider?

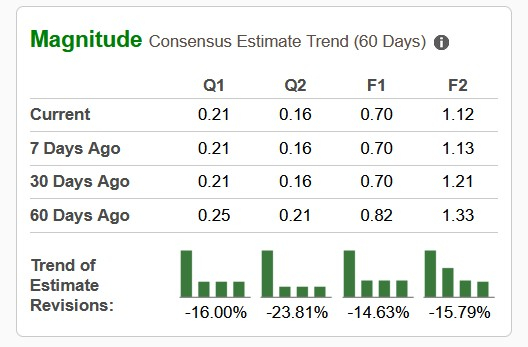

The negative sentiment surrounding Schneider stock is evident from the fact that the Zacks Consensus Estimate for the fourth quarter of 2025, as well as for full-year 2025 and 2026 earnings, has been revised downward in the past 60 days. The consensus mark for first-quarter 2026 earnings has also been projected northward in the past 60 days.

The unfavorable estimate revisions indicate brokers’ lack of confidence in the stock.

Time to Get Rid of Schneider

There is no doubt that the stock is attractively valued, and consistent shareholder-friendly initiatives (in the form of dividends and share buybacks) and declining capital expenditures act as tailwinds for Schneider’s bottom-line growth. Despite such positives, investors should refrain from rushing to buy Schneider now due to the headwinds that it faces.

Schneider’s bottom line continues to grapple with the adverse effect of insurance-related costs (related to prior year claims). This has led to Schneider’s full-year tempered earnings outlook. As a result, SNDR has reduced its 2025 adjusted earnings per share guidance to approximately 70 cents from the prior guidance of 75-95 cents. Lower brokerage volume continues to hurt SNDR's logistics segment revenues. The ongoing volatile macro environment marked by economic uncertainty, shifting tariff regulations and geopolitical tensions also clouds Schneider’s prospects. Collectively, these factors diminish Schneider’s appeal as an investment at this juncture. So, the stock appears to be a risky bet for investors. The stock’s current Zacks Rank #4 (Sell) justifies our analysis.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-22 | |

| Jul-20 | |

| Jul-15 | |

| Jul-07 | |

| Jul-07 | |

| Jul-07 | |

| Jul-06 | |

| Jun-30 | |

| Jun-29 | |

| Jun-29 | |

| Jun-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite