|

|

|

|

|||||

|

|

|

The companies operating in the Zacks Oil and Gas – Production Pipeline MLB play a vital role in meeting rising global energy demand by supplying crude oil and natural gas that fuel transportation, industrial activity and households. Their operations strengthen energy security, support economic growth and deliver essential feedstocks for petrochemicals and fertilizers. As consumption continues to grow, these companies remain integral to balancing conventional energy supply while advancing cleaner technologies and carbon-reduction initiatives.

Pipeline operators like Energy Transfer LP ET and ONEOK Inc. OKE, through their infrastructure provides a reliable supply to refineries, power plants and consumers, while lowering costs and minimizing risks compared with rail or truck transport. By enabling producers to explore new opportunities and guaranteeing uninterrupted energy availability, pipeline companies play a pivotal role in economic stability and remain fundamental in supporting both current energy needs and the transition toward a sustainable future.

Energy Transfer presents a compelling investment opportunity supported by its extensive, diversified midstream network across natural gas, natural gas liquids (NGLs), crude oil and refined products. The firm benefits from stable, fee-based cash flows, strategic access to export terminals and disciplined capital allocation, positioning it to capture growth from the rising U.S. energy production and global demand. With an attractive distribution yield, steady EBITDA expansion and ongoing balance sheet strengthening through deleveraging, ET stands out as a strong long-term choice for investors seeking both income and growth in the energy sector.

ONEOK presents a solid investment case driven by its extensive NGL infrastructure and strategically positioned pipeline network across major U.S. energy basins. Supported by stable, fee-based cash flows, limited commodity exposure, disciplined capital allocation and ongoing debt reduction, the company offers earnings visibility and an attractive dividend. Its integrated scale positions OKE for steady, long-term value creation through reliable income and moderate growth in the midstream energy sector.

Both companies operate essential infrastructure in North America that transports, stores and processes natural gas, NGLs and crude oil. Their assets are vital in linking producers in resource-rich regions such as the Permian and Mid-Continent basins to major end markets nationwide. Let’s focus on the fundamental factors of these midstream companies and try to find which one presently has a better possibility to provide higher returns to investors.

The Zacks Consensus Estimate for ET’s earnings per unit in 2025 and 2026 indicates year-over-year growth 3.91% and 15.25%, respectively. Long-term (three to five years) earnings growth per share is pegged at 12.45%.

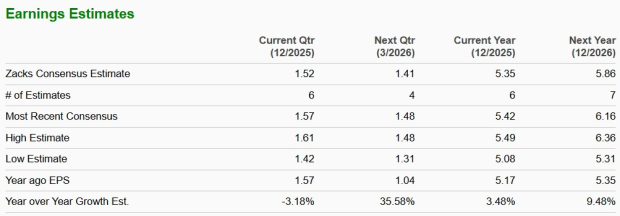

The Zacks Consensus Estimate for OKE’s earnings per unit in 2025 and 2026 implies year-over-year growth 3.48% and 9.48%, respectively. Long-term (three to five years) earnings growth per share is pegged at 3.06%.

The Zacks Consensus Estimate for ET’s sales in 2025 and 2026 implies year-over-year growth 4.42% and 26.64%, respectively.

The same for OKE’s sales in 2025 and 2026 indicates year-over-year growth 62.13% and 17.97%, respectively.

Return on Equity (“ROE”) is an essential financial indicator that evaluates a company’s efficiency in generating profits from the equity invested by its shareholders. It demonstrates how well management is utilizing the capital provided to increase earnings and deliver value.

ET’s current ROE is 10.71% compared with OKE’s 15.12%. OKE’s ROE is better than the industry’s 13.28%.

The oil and energy pipeline sector is highly capital-intensive, requiring substantial and recurring investments to maintain, upgrade and expand infrastructure. Adoption of evolving technologies demands ongoing capital outlays. As a result, companies in this industry typically rely on a combination of internal cash generation and external borrowing to finance their long-term investment programs. Both firms will benefit as the Fed lowers the interest rate to a range of 3.50% to 3.75%.

ET’s current long-term debt-to-capital stands at 58.87% compared with OKE’s 59.08%.

Energy Transfer currently appears to be trading at a discount compared with ONEOK on a forward 12-month Price/Earnings basis.

ET is currently trading at P/E F12M of 10.77X, while OKE is trading at 12.61X compared with the industry’s 12.23X.

ET’s units have declined 0.7% in the past three months against OKE’s rally of 2.7%. The sector has gained 1.4% in the same time period.

Energy Transfer and ONEOK are strategically expanding operations and successfully transferring hydrocarbons from the production region to their end users.

ONEOK’s stronger projected sales growth, higher return on equity and superior price performance, despite only a marginally higher reliance on debt compared with ET, tip the scales in its favor.

Based on the above discussion, ONEOK has an edge over Energy Transfer, despite both stocks carrying a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Jul-31 | |

| Jul-27 | |

| Jul-27 | |

| Jul-23 | |

| Jul-17 | |

| Jul-17 | |

| Jul-15 | |

| Jul-09 | |

| Jul-07 | |

| Jul-06 | |

| Jul-05 | |

| Jul-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite