|

|

|

|

|||||

|

|

|

Sterling Infrastructure, Inc. STRL is gaining from robust data center–related site development and mission-critical projects, which are operated through its E-Infrastructure Solutions segment. These projects comparatively carry structurally higher margins due to their complexity, tighter timelines and the premium customers place on execution certainty. During the third quarter of 2025, revenues from the data center market grew year over year by a whopping 125%, with the E-Infrastructure segment’s revenues increasing 58% (including the CEC acquisition).

Management has emphasized that Sterling’s project selection discipline and focus on negotiated or repeat-customer work, rather than low-bid contracts, are central to protecting margins even as volumes rise. Besides, the company is additionally benefiting from standardized processes, strong cost controls and experienced project teams that limit rework and schedule overruns. This execution advantage has allowed STRL to scale revenues while still expanding margins, rather than facing the typical dilution that accompanies rapid growth in construction.

Notably, the CEC acquisition, closed in the third quarter of 2025, is catalyzing Sterling’s growth prospects as this buyout expands its electrical capabilities that complement site development work, increasing self-perform content and cross-selling opportunities, both of which are margin-accretive over time.

Although a large project scale can introduce complexity, labor availability constraints and competitive intensity in data center infrastructure, STRL’s strong visibility in high-margin end markets and efficient execution are encouraging for the near and long-term growth. Thus, it can be highlighted that Sterling appears well-positioned to defend margins near the 25% level in the upcoming period.

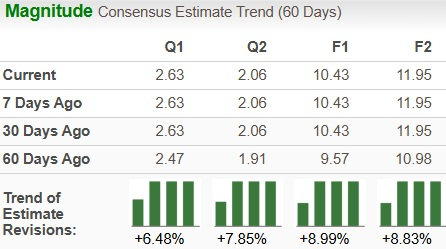

STRL’s earnings estimates for 2025 and 2026 have moved north in the past 60 days. The analysts’ optimism is expected to have been boosted by the ongoing strong trends, especially in the data center market, and its exceptional operational execution.

The estimated figures for 2025 and 2026 imply year-over-year growth of 71% and 14.6%, respectively.

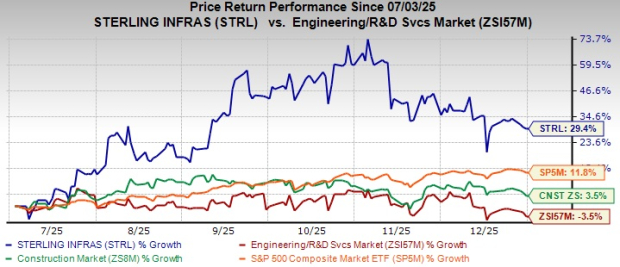

Shares of this Texas-based infrastructure services provider have gained 29.4% in the past six months, significantly outperforming the Zacks Engineering - R and D Services industry, the broader Construction sector and the S&P 500 index.

Notably, firms like Granite Construction Incorporated GVA and KBR, Inc. KBR offer substantial competition to Sterling across large-scale infrastructure & industrial projects and transportation infrastructure projects. In the past six months, shares of Granite have moved up 22.8% while KBR has tumbled 15.6%, underperforming STRL.

STRL stock is currently trading at a premium compared with its industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 29.35, as shown in the chart below.

Notably, Granite and KBR are currently trading at a forward 12-month P/E ratio of 19.16 and 10.55, respectively.

Sterling stock currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 8 hours | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-03 | |

| Aug-03 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite