|

|

|

|

|||||

|

|

|

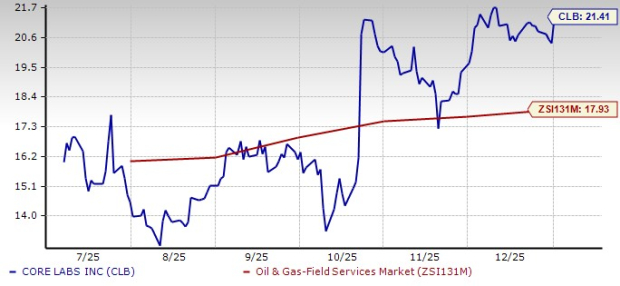

Over the past six months, Core Laboratories Inc. CLB has shown remarkable growth, outpacing both the Oil & Gas Field Services sub-industry (ZS131M) and the broader Oil and Energy sector (ZS12M). CLB's share price surged 48.2%, reflecting strong performance and investor confidence. In comparison, the Oil & Gas Field Services sub-industry grew 25.1%, while the broader Oil and Energy sector experienced a more modest increase of 7.1%. This significant outperformance by CLB highlights its leadership in the industry during this period.

Houston, TX-based oil and gas equipment and services company generates revenues by providing specialized services and products to the oil and gas industry, including reservoir optimization, production enhancement and geological analysis. Its main revenue streams come from laboratory services, equipment sales and data analytics, helping clients make informed decisions about their subsurface assets. CLB also offers proprietary technologies for reservoir management, focusing on fluids, rock properties and enhanced oil recovery.

As the stock gains attention for the strong performance, investors are keen to understand the factors contributing to the company's success and whether it's the right time to invest. Let's delve into the key drivers behind the stock's growth and assess any potential risks.

Consistent Sequential Growth and Margin Expansion: CLB demonstrated solid operational execution in third-quarter 2025 with revenues increasing more than 3% sequentially to $134.5 million. More importantly, the company achieved significant sequential improvement in operating income, operating margins (ex-items) and earnings per share, indicating effective cost management and positive business momentum. This performance suggests the company is successfully navigating a volatile market environment.

Leading Market Position in Reservoir Description: Approximately 80% of Reservoir Description revenues come from international and offshore projects, which are typically long-cycle and less sensitive to short-term commodity price swings. Core Laboratories' dominant position in providing essential rock and fluid analysis for these complex projects creates a stable, high-margin revenue base.

High-Impact Proprietary Technology and Client Solutions: The transcript details specific projects where Core Laboratories' proprietary technologies solved critical client problems, such as an asphaltene stability study in the Middle East and a complex pipe recovery operation in West Africa. These examples demonstrate the company's technical differentiation and its role as a high-value partner, not just a service provider.

Favorable Exposure to International Growth Markets: CLB’s management reports seeing higher planned activity from clients globally, led by the Middle East, followed by the South Atlantic Margin and West Africa, with new momentum in the Asia Pacific. This international diversification reduces reliance on the more cyclical U.S. onshore market and positions the company for growth as investment shifts globally.

Pressure on Product Sales and Input Costs: Product sales, which are more evenly split between North America and international markets, decreased 6% year over year in the third quarter of 2025. Furthermore, the company cited increased costs for imported steel due to tariffs, which pressured margins in the quarter, illustrating sensitivity to raw material costs and trade policies.

Concentration Risk in International Markets: While international diversification is a strength, it also exposes the company to regional economic, political and currency risks in areas like the Middle East, Africa and the Asia Pacific. Unforeseen events in any key region could disrupt project timelines and client payments, affecting financial performance.

Valuation Concerns: CLB's P/E ratio of 21.41, significantly higher than the sub-industry's average of 17.93, raises concerns for investors. This suggests the stock is overvalued, with expectations of strong growth that may be unrealistic. If CLB fails to meet these high expectations, investors could face considerable losses as the stock could drop sharply.

Potential for M&A Integration Challenges: The recent acquisition of Solintec, while strategically sound, carries integration risks. Successfully merging operations, cultures and client relationships to realize the anticipated accretive benefits is a complex process, and any missteps could divert management attention and incur unexpected costs.

CLB has shown strong sequential growth and margin expansion, with a 3% increase in revenues and significant improvements in operating income and margins in third-quarter 2025. The company benefits from its dominant market position in reservoir description, particularly in international and offshore projects, which provides a stable and high-margin revenue base. CLB also stands out for its proprietary technology, which solves critical client problems, and the favorable exposure to international growth markets like the Middle East and West Africa.

However, the company faces challenges, including pressure on product sales, rising input costs and a higher-than-average P/E ratio that raises valuation concerns. Additionally, there are risks associated with international market concentration and potential integration difficulties from its recent acquisition of Solintec. Taking into account both the positive and negative aspects, investors should wait for a more opportune moment before adding this Zacks Rank #3 (Hold) stock to their portfolio.

Investors interested in the energy sector might look at some better-ranked stocks like Oceaneering International OII, Antero Midstream AM and Baytex Energy BTE, each sporting a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Oceaneering International is valued at $2.48 billion. The company is a global provider of engineered services and products to the offshore energy, aerospace and defense industries. OII specializes in underwater robotics, remotely operated vehicles and subsea engineering solutions for offshore oil and gas exploration and production.

Antero Midstream is valued at $8.54 billion. It is a leading midstream energy company that provides natural gas gathering, compression and transportation services. Antero Midstream primarily operates in the Appalachian Basin, focusing on connecting producers with downstream markets, and manages a portfolio of infrastructure assets, including pipelines and processing plants.

Baytex Energy is valued at $2.54 billion. It is an oil and gas company that engages in the exploration, development and production of crude oil and natural gas in North America. Baytex Energy has operations in both the heavy oil sector of Alberta, Canada, and in the Eagle Ford shale of Texas, balancing its portfolio between conventional and unconventional energy resources.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite