|

|

|

|

|||||

|

|

|

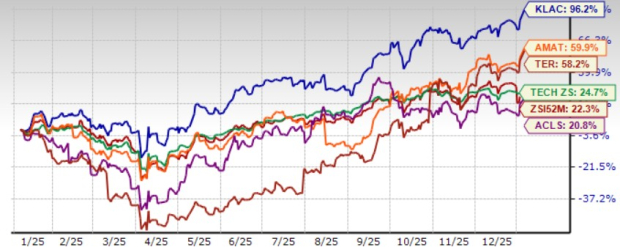

KLA Corporation KLAC shares have jumped 96.2% in the trailing 12 months, outperforming the Zacks Computer and Technology sector’s return of 24.6% and the Zacks Electronics-Miscellaneous Products industry’s appreciation of 22.3%. KLA is benefiting from its dominant process control market share, strong AI infrastructure investment and momentum in advanced packaging.

The company has outperformed peers, including Applied Materials AMAT, Teradyne TER and Axcelis Technologies ACLS, in the past year. Shares of Applied Materials, Teradyne and Axcelis have returned 28.78%, 58.2% and 20.8%, respectively, over the same timeframe.

These factors justify a premium valuation as suggested by a Value Score of F.

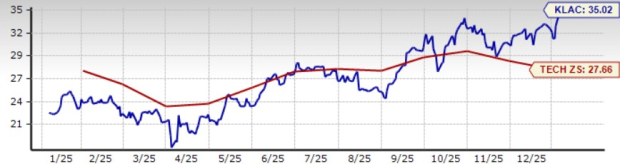

In terms of the forward 12-month price-to-earnings (P/E), KLAC is trading at 35.02X, higher than the broader sector and peers. The broader sector is trading at 27.66X while Applied Materials and Axcelis trade at 28.78X and 19.57X, respectively. However, Teradyne is pricey with a P/E multiple of 43.04.

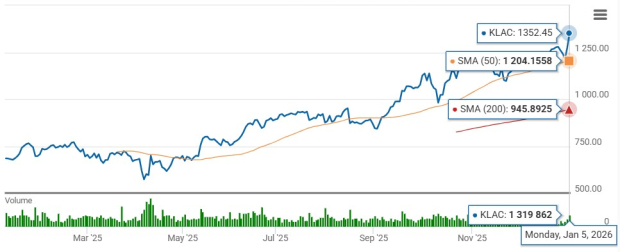

Technically, KLA is currently trading above the 50-day and the 200-day moving averages, indicating a bullish trend.

KLA is benefiting from strong demand for leading-edge logic, high-bandwidth memory (HBM) and advanced packaging, which is driving top-line growth. Advanced packaging revenues are expected to exceed $925 million in calendar 2025, up roughly 70% from calendar 2024. Strong investments in WFE and advanced packaging represent a strong growth opportunity for the company. Growth of advanced packaging supporting heterogeneous chip integration has become a new market for KLA, which is currently worth $11 billion and growing faster than core WFE.

KLA’s robust portfolio and its leadership in process control systems are enabling customers to manage increasing design complexity. Process control accelerates time to results by resolving process integration challenges during the fab ramp-up phase to optimize time to market for a diverse mix of semiconductor designs.

Moreover, the growing investment in custom silicon, particularly among hyperscalers developing their own custom chips, has led to a proliferation of unique device designs. This has put customers under pressure to deliver performance, volume and time to market, resulting in strong demand for advanced process control. This aids KLA’s prospects as each new chip design requires rigorous inspection, metrology and yield optimization solutions. This bodes well for KLAC’s top-line growth.

KLAC expects to meaningfully outperform the mid-to high single-digit WFE growth rate estimated in 2025, driven by rising process control intensity, inclusive of the significant growth of the advanced packaging market. The advanced packaging market is also expected to grow more than 20% in 2025 compared to last year. For 2026, HBM is expected to grow faster than overall logic/foundry growth next year. Over the long term, KLAC targets to deliver 40% to 50% incremental non-GAAP operating margin leverage on strong revenue growth.

KLA generates solid cash flow, which allows management the opportunity to invest in product innovations, acquisitions and business development. The company ended the first quarter of fiscal 2026 with $4.7 billion in total cash, cash equivalents and marketable securities and $5.9 billion in debt. The company has a flexible and attractive bond maturity profile.

In the first quarter of fiscal 2026, operating cash flow was $1.16 billion, whereas the free cash flow was $1.07 billion. In the fiscal first quarter, KLAC repurchased $545 million worth of shares and paid $254 million in dividends.

The Zacks Consensus Estimate for fiscal 2026 earnings is pegged at $35.44 per share, up a couple of cents over the past 30 days and indicating 6.5% growth from 2025’s reported figure. The consensus mark for fiscal 2026 revenues is pegged at $13.04 billion, suggesting 7.3% growth from the 2025’s reported figure.

KLA Corporation price-consensus-chart | KLA Corporation Quote

The Zacks Consensus Estimate for second-quarter fiscal 2026 earnings is pegged at $8.75 per share, unchanged over the past 30 days and indicating 6.7% growth over the year-ago quarter’s reported figure. The consensus mark for third-quarter fiscal 2026 revenues is pegged at $3.24 billion, suggesting 5.4% growth from the year-ago quarter’s reported figure.

KLA benefits from strong demand for leading-edge logic, HBM and advanced packaging. These factors are expected to help the stock continue its momentum in 2026.

KLA currently has a Zacks Rank #2 (Buy) and a Growth Score of B, a favorable combination that offers a strong investment opportunity, per the Zacks Proprietary methodology. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-19 | |

| Jul-17 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite