|

|

|

|

|||||

|

|

|

Chipotle Mexican Grill, Inc. CMG is entering a period of accelerated unit expansion, with management guiding to 350-370 new restaurant openings in 2026, marking a notable step-up from 2025 levels and well above the roughly 140 restaurants opened in 2019. As the pace increases, investor focus has shifted toward the potential impact of new units on comparable sales and whether cannibalization risks are intensifying.

During the third quarter of 2025, management indicated that new restaurant openings contributed an approximately 100-basis-point headwind to reported comparable sales, a level described as consistent with historical experience. The company stated that the comparable sales impact was driven by the pace of unit expansion, rather than any weakening in existing restaurant performance. It highlighted strong early economics from new restaurants with first-year sales productivity near 80% and year-two cash-on-cash returns around 60%, thereby reinforcing confidence in site selection and market capacity.

Chipotle also noted that cannibalized restaurants typically recover within roughly 12 to 13 months, a recovery timeline that has remained stable even as the pace of development has increased. Management emphasized that per-store cannibalization metrics have not worsened versus prior years, suggesting that incremental supply continues to be absorbed without causing lasting disruption to the existing base.

Looking ahead, as the company advances toward its long-term goal of 7,000 restaurants in North America, management indicated that the comp impact from new openings could become less pronounced over time as unit growth eventually levels off. While macro-driven traffic pressure remains a near-term consideration, consistent unit-level economics and stable recovery patterns suggest that restaurant expansion remains a structurally supportive element of Chipotle’s long-term operating model.

Shares of Chipotle have plunged 33.2% in the past year compared with the industry’s fall of 6%. In the same time frame, other industry players like Starbucks Corporation SBUX, Sweetgreen, Inc. SG and CAVA Group, Inc. CAVA have declined 3.4%, 77.4% and 41.5%, respectively.

From a valuation standpoint, CMG trades at a forward price-to-sales (P/S) multiple of 3.91, above the industry’s average of 3.47. Conversely, industry players, such as Starbucks, Sweetgreen and CAVA, have P/S multiples of 2.60, 1.15 and 5.48, respectively.

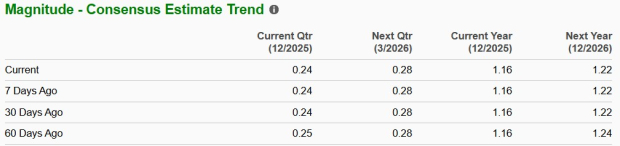

The Zacks Consensus Estimate for CMG’s 2026 earnings per share has declined in the past 60 days.

The company is likely to report strong earnings, with projections indicating a 4.7% rise in 2026. Conversely, industry players like Sweetgreen and CAVA are likely to witness an increase of 15.5% and 10.9%, respectively, year over year, in 2026 earnings. Meanwhile, Starbucks' fiscal 2026 earnings are likely to witness a rise of 9.4%, year over year.

CMG stock currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 21 min | |

| 31 min | |

| 2 hours | |

| 3 hours | |

| 6 hours | |

| 6 hours |

CAVA Earnings Prediction Market Preview: What Will Brett Schulman Say?

CAVA

Benzinga Prediction Markets

|

| 7 hours | |

| 8 hours | |

| 11 hours | |

| 12 hours | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite