|

|

|

|

|||||

|

|

|

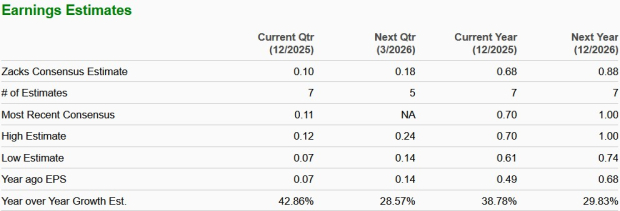

Earnings expectations for Dutch Bros Inc. BROS have strengthened notably, underscoring rising confidence in its growth trajectory. Over the past six months, 2025 EPS estimates have climbed 15.3% to 68 cents, while 2026 projections have advanced 8.6% to 88 cents. This steady upward revision trend signals increasing optimism among analysts and reinforces the market’s bullish outlook on Dutch Bros’ long-term earnings power.

Complementing this upbeat earnings outlook, Dutch Bros is also positioned for robust top-line expansion. Revenues in 2025 and 2026 are projected to rise 26.5% and 25%, respectively, on a year-over-year basis. Even more compelling, earnings are expected to outpace sales growth, with profit estimates indicating a sharp 38.8% increase in 2025, followed by a solid 29.8% rise in 2026, highlighting improving operating leverage and a strengthening profitability profile.

Dutch Bros continues to stand out in the beverage space due to its culture-led operating model, which management repeatedly emphasized as a core competitive advantage. The company’s high-energy service, deep customer engagement and consistent execution by its “Broistas” are translating into strong transaction growth, even in a challenging consumer environment. This people-first approach has helped Dutch Bros deliver five consecutive quarters of transaction gains, reinforcing brand loyalty and making the concept more resilient than traditional QSR peers.

Another major growth engine is the company’s transaction-driving initiatives, particularly Order Ahead and Dutch Rewards. Digital engagement is accelerating, with Order Ahead accounting for a rising share of sales and acting as a gateway into the loyalty ecosystem. Dutch Rewards now drives more than two-thirds of system transactions, enabling targeted, segmented offers rather than blanket discounting. This precision marketing approach is boosting frequency while protecting margins and supporting sustainable same-shop sales growth.

Dutch Bros’ shop expansion strategy is also fueling momentum. New stores are delivering record average unit volumes and demand remains strong across newer regions such as the Midwest and Southeast. Management highlighted a robust development pipeline, supported by improved real estate analytics and capital-efficient build-to-suit leases. These factors provide clear visibility into long-term unit growth and reinforce confidence in the company’s goal of more than doubling its store base by 2029.

Innovation remains a powerful differentiator. Dutch Bros continues to lead with beverage creativity, limited-time offerings and brand activations, keeping the menu fresh and culturally relevant. At the same time, the company is expanding beyond drinks through its evolving food program, which is already generating both ticket and transaction lift in early markets. This layered innovation strategy strengthens customer engagement across multiple dayparts and deepens the brand’s emotional connection with its core audience.

Looking ahead to 2026, several catalysts appear poised to sustain growth. These include an accelerating pace of new shop openings, a full-year benefit from the hot food rollout and continued gains from digital ordering and loyalty-driven personalization. In addition, the planned CPG rollout will extend the brand beyond the drive-thru, while ongoing investments in analytics and throughput efficiency should support higher transactions without sacrificing service quality. Collectively, these levers position Dutch Bros for another year of above-industry growth and expanding brand reach.

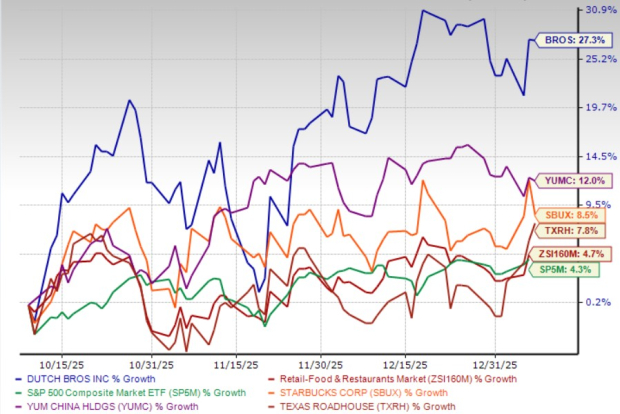

Dutch Bros’ shares have surged 27.3% in the past three months compared with the industry’s growth of 4.7%. In the same time frame, the S&P 500 has gained 4.3%.

Shares of other industry players like Starbucks Corporation SBUX, Yum China Holdings, Inc. YUMC and Texas Roadhouse, Inc. TXRH have gained 8.5%, 12% and 7.8%, respectively, in the same time frame.

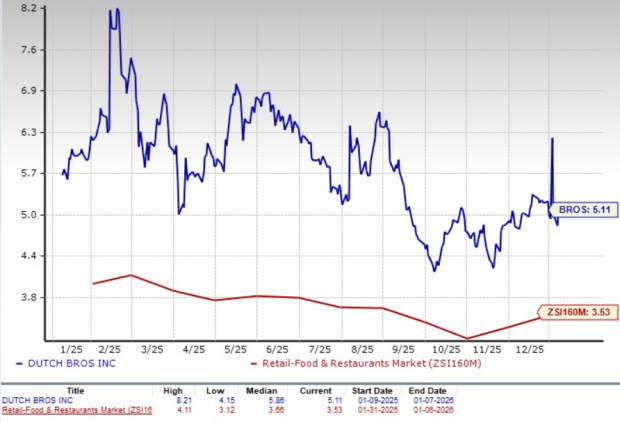

Dutch Bros is trading at a premium to the industry, with a forward 12-month price-to-sales of 5.11X, which is well above the industry average of 3.53X. Meanwhile, Starbucks, Yum China and Texas Roadhouse are trading at P/S ratios of 2.52X, 1.38X and 1.83X, respectively.

Dutch Bros emerges as a differentiated growth story supported by strong execution, expanding customer engagement and improving profitability. The company’s culture-driven operating model continues to drive steady transaction growth, while digital ordering and loyalty programs are strengthening repeat visits without relying on aggressive discounting. At the same time, disciplined shop expansion into new markets, combined with menu and food innovation, is broadening the brand’s appeal and extending its growth runway.

Even though the stock commands a premium valuation, investors may view it as warranted given the company’s long-term visibility, scalable model and ability to compound earnings faster than many peers in the restaurant space.

BROS currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 |

Fast-growing Dutch Bros is buying up to 65 Salad and Go locations

BROS BROS -18.79%

Nation's Restaurant News

|

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite