|

|

|

|

|||||

|

|

|

PepsiCo Inc. PEP has seen its shares trend lower in recent months, compressing its price-to-earnings (P/E) multiple to below the Zacks Beverages – Soft Drinks industry average, reflecting growing investor caution around near-term growth and margin pressures. This valuation discount underscores investor concerns about PepsiCo Foods North America’s (“PFNA”) volume softness, margin compression, and ongoing cost inflation and tariff-related headwinds weighing on the company’s near-term performance.

Despite near-term headwinds, PepsiCo appears increasingly attractive at current levels. Its forward 12-month P/E of 16.27X sits below the industry average of 17.5X, suggesting the stock may offer a compelling entry point for long-term investors.

Additionally, the company’s forward 12-month price-to-sales (P/S) ratio of 1.96X is below the industry average of 4.66X.

At 16.27X times P/E, PepsiCo trades at a significantly lower valuation than its competitors, such as The Coca-Cola Company KO, The Vita Coco Company, Inc. COCO and Monster Beverage Corporation MNST, which are delivering solid growth and trade at higher multiples. Coca-Cola, Vita Coco and Monster Beverage have forward 12-month P/E ratios of 21.51X, 34.75X and 33.93X, all significantly higher than PepsiCo.

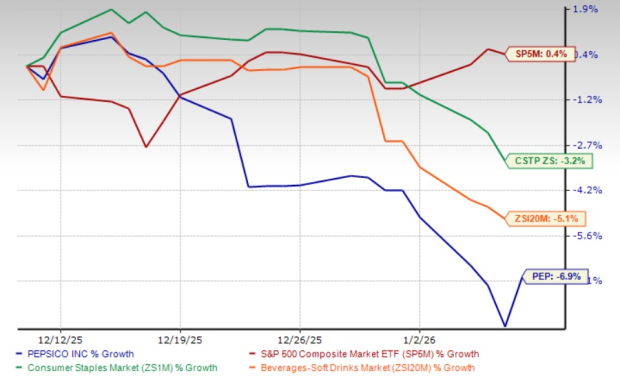

In the past month, PepsiCo’s shares have lost 6.9% compared with the broader industry and the Zacks Consumer Staples sector’s declines of 5.1% and 3.2%, respectively. The company has also underperformed the S&P 500’s rise of 0.4%.

PEP’s performance is weaker than that of its key competitor, Coca-Cola, which has declined 1.2% in the past month. The stock also underperformed Monster Beverage and Vita Coco’s growth of 1.9% and 3.7%, respectively, in the same period.

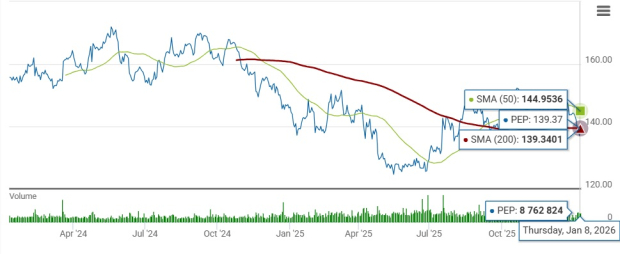

PEP’s current share price of $139.37 is 13% below its recent 52-week high mark of $160.15. Also, the stock trades 9.2% above its 52-week low of $127.60. PepsiCo trades below its 50-day moving average, indicating a bearish sentiment. However, the stock moves slightly above the 200-day moving average, suggesting long-term potential.

PEP’s recent performance has been shaped by a mix of macroeconomic pressures, category-specific challenges and strategic initiatives, as outlined in its third-quarter 2025 results. In North America, constrained consumer budgets have been weighing on packaged food demand, pressuring volumes at PFNA, although margin trends have begun to improve due to aggressive cost optimization and more disciplined trade promotions. Higher supply-chain costs, including sourcing inflation and tariff-related impacts, posed a notable headwind to earnings in the third quarter.

At the same time, PepsiCo Beverages North America (“PBNA”) showed signs of recovery, supported by innovation, zero-sugar offerings and strength in brands like Pepsi Zero Sugar and Mountain Dew. International markets remained a key growth engine, delivering mid-single-digit organic revenue growth despite weather disruptions in certain regions. Portfolio reshaping, price-pack architecture and productivity initiatives remain central to PepsiCo’s efforts to stabilize margins and reignite sustainable growth.

The Zacks Consensus Estimate for PepsiCo’s 2025 EPS has been unchanged in the past 30 days, while the estimate for 2026 EPS moved down 0.3% in the last 30 days. The downward revision in earnings estimates indicates that analysts are losing confidence in the company’s growth potential.

The Zacks Consensus Estimate for PEP’s 2025 sales suggests year-over-year growth of 1.9% and that for EPS indicates a decline of 0.5%. For 2026, the Zacks Consensus Estimate for PepsiCo’s sales and EPS implies 3.7% and 5.4% year-over-year growth, respectively.

PepsiCo’s fundamentals remain largely intact despite near-term pressures, as reflected in third-quarter 2025. The company continues to demonstrate resilience through its diversified portfolio, global scale and disciplined execution. While PFNA faces volume softness amid constrained consumer spending, management has made improving PFNA performance a top priority, supported by cost reductions, portfolio transformation and sharper price-pack architecture. Core operating margin trends in the segment have already shown improvement from the prior quarters.

PBNA delivered accelerating momentum, driven by innovation, zero-sugar offerings and strong performance from brands like Pepsi Zero Sugar, Mountain Dew and emerging platforms such as poppi. International operations remain a clear strength, posting its 18th consecutive quarter of at least mid-single-digit organic revenue growth, underscoring the durability of PepsiCo’s global footprint.

Although higher supply-chain and tariff-related costs have weighed on earnings, the company is actively mitigating these headwinds through productivity initiatives and sourcing flexibility. Overall, PepsiCo’s strong brands, innovation pipeline and margin-recovery actions suggest its long-term fundamentals remain sound.

PepsiCo presents a mixed risk-reward profile at current levels. On one hand, the stock’s valuation discount versus peers suggests an attractive long-term entry point, supported by strong brands, global scale and initiatives to stabilize margins and improve growth. On the other hand, the recent share price weakness, ongoing PFNA softness, cost pressures and downward revisions to earnings estimates highlight meaningful near-term challenges that could continue to weigh on sentiment.

Given this balance, a neutral stance appears warranted. Existing shareholders may be better served holding the stock, as PepsiCo’s fundamentals remain intact and its long-term growth drivers are still in place. However, for new investors, it may be prudent to wait for clearer signs of operational recovery and earnings stabilization before committing fresh capital. PEP currently carries a Zacks Rank #3 (Hold). You can see the complete list of today's Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-09 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite