|

|

|

|

|||||

|

|

|

Nvidia's rise throughout the artificial intelligence (AI) revolution primarily stems from its thriving data center business.

The company has laid the groundwork to evolve into a multiplatform business beyond data centers.

Nvidia currently trades near its cheapest valuation in three years.

For the last three years, the artificial intelligence (AI) revolution has largely been fueled by a specific piece of hardware: the graphics processing unit (GPU). GPUs are advanced chip accelerators capable of processing complex algorithms at high speeds -- ushering in a wave of new applications powered by generative AI.

Nvidia (NASDAQ: NVDA) had a first-mover advantage in the GPU landscape; hence, demand for the company's chipsets has been off the charts as big tech races to construct AI-equipped data centers.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Since OpenAI commercially launched ChatGPT in November 2022, Nvidia stock has gained roughly 1,000% -- propelling its market cap from $345 billion to $4.6 trillion, making it the most valuable company in the world.

Let's take a look at how influential Nvidia has been to the overall AI landscape so far. From there, I'll outline a few catalysts that I think are flying under the radar as the company evolves from a chip designer and into a more multifaceted platform. Looking ahead, Nvidia could be a very different company by next decade than where it stands today.

Image source: The Motley Fool.

In fiscal 2023 (ended Jan. 29, 2023), Nvidia generated $26.9 billion in revenue -- essentially flat growth compared to the prior year. That year, the largest contribution to Nvidia's revenue base came from its data center segment -- which reported 41% annual growth of $15 billion.

So while the company's total revenue growth wasn't stellar, smart investors were keeping a keen eye on the trajectory of the data center operation.

If we fast-forward to the current day, Nvidia reported total sales of $57 billion during its third quarter of fiscal 2026 (ended Oct. 26). Once again, the data center business stole the spotlight -- growing 66% year over year to $51.2 billion.

In less than three years, Nvidia has grown its data center business from $15 billion in annual revenue to a run rate of nearly $200 billion.

As referenced, the key contributor to this astronomic growth revolves around unrelenting demand for GPUs. Over the last three years, Nvidia's Hopper, Blackwell, and now Vera Rubin chips have been a core line item within the capital expenditure (capex) budgets from hyperscalers like Microsoft, Alphabet, Amazon, Meta Platforms, and Oracle.

While GPUs will continue to be a major tailwind for Nvidia, I'm predicting the next five years will feature far more than data center services. Let's explore what else Nvidia has on the horizon.

The last three years have been about procuring chips and developing generative AI applications powered by large language models (LLMs). But as AI workloads scale and become more sophisticated, Nvidia is positioned to benefit from additional utilities.

By the end of the decade, AI could begin to assume more physical protocols. Specifically, the rise of humanoid robotics from companies like Tesla, as well as AI-powered manufacturing robots employed by the likes of Amazon, could completely revolutionize the labor force.

In addition, autonomous systems including self-driving cars are already being trained using Nvidia's chips. Nevertheless, Nvidia's automotive segment is barely moving the needle for the company's financial profile at this time.

Another catalyst that I think is overlooked is how AI will play a critical role in developing next-generation telecommunications services as businesses like Nokia race to introduce 6G to the masses.

Given Nvidia's investment in Nokia back in the fall, I would not sleep on the company's ability to continue deploying excess capital strategically in an effort to expand its total addressable market (TAM) beyond data centers.

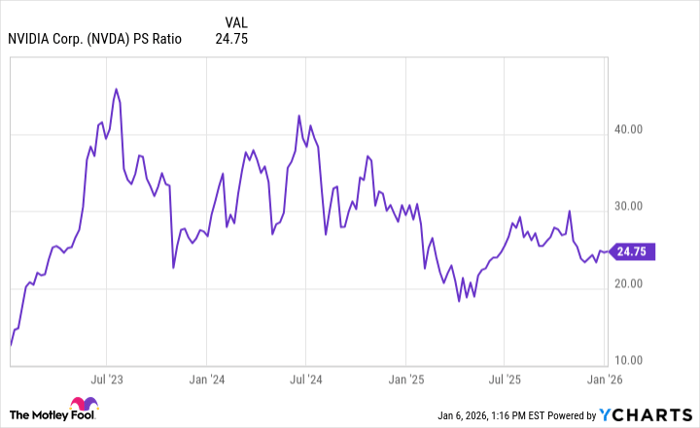

At the moment, Nvidia trades at a price-to-sales (P/S) ratio of roughly 25. Except for the hit Nvidia took last April following President Trump's "Liberation Day" tariff announcement, Nvidia's P/S multiple is hovering near its lowest levels prior to the stock taking off three years ago.

NVDA PS Ratio data by YCharts

In my eyes, investors may be starting to get exhausted by the GPU storyline -- especially since competition from Advanced Micro Devices and Broadcom is emerging. Against this backdrop, Nvidia might not be seen as a growth stock but more of a maturing business in the eyes of some investors.

I am not aligned with this sentiment. If anything, these opportunities make me even more optimistic over Nvidia's growth prospects as the AI infrastructure era begins.

For these reasons, I think meaningful valuation expansion could be in store for Nvidia in the coming years. Taking this a step further, if Nvidia's P/S ratio were to climb back toward its prior highs -- roughly in the 40x range -- the company's implied future market cap would be well north of $7 trillion. That could mean investors could witness gains of at least 50% from current levels.

Given these dynamics, I see Nvidia as a no-brainer opportunity to buy and hold for patient investors, as more upside appears to be in store through 2030.

Before you buy stock in Nvidia, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Nvidia wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $488,222!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,134,333!*

Now, it’s worth noting Stock Advisor’s total average return is 969% — a market-crushing outperformance compared to 196% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of January 9, 2026.

Adam Spatacco has positions in Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, and Tesla. The Motley Fool has positions in and recommends Advanced Micro Devices, Alphabet, Amazon, Meta Platforms, Microsoft, Nvidia, Oracle, and Tesla. The Motley Fool recommends Broadcom and recommends the following options: long January 2026 $395 calls on Microsoft and short January 2026 $405 calls on Microsoft. The Motley Fool has a disclosure policy.

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite