|

|

|

|

|||||

|

|

|

Owlet, Inc. OWLT has delivered one of the strongest stock performances in the small-cap consumer health space, with shares up more than 82% over the past six months. The rally has sharply outpaced the Zacks Electronics - Miscellaneous Products industry, Zacks Computer and Technology sector and the S&P 500 Index, as shown below, reflecting a combination of improving fundamentals, regulatory clarity and rising investor confidence in Owlet’s transition from a hardware-driven baby monitor company into a data-enabled pediatric health platform. With the stock now trading near its recent highs, the key question for investors is whether the recent momentum still supports a Buy thesis.

OWLT Share Price Performance

Owlet’s recent rally is also supported by strengthening technical signals. The stock is trading near $15.83, comfortably above both its 50-day simple moving average of $12.87 and its 200-day simple moving average of $8.26, confirming a sustained uptrend. The widening gap between the 50-day and 200-day averages reflects improving medium- and long-term momentum, suggesting that recent gains are not purely short-term in nature.

Importantly, this move has not been driven by speculation alone. Management delivered a standout fiscal third-quarter 2025, marking the strongest quarter in the company’s history across revenue, profitability and operating leverage.

Revenue reached a record level in the quarter, driven by strong demand for the Dream Sock franchise and the launch of the Dream Sight camera. Gross margins expanded above the 50% level despite higher tariffs, and Owlet posted its first-ever quarterly operating profit. These results reinforced the view that the company has moved beyond survival mode and is now scaling with discipline.

One of the most important developments supporting Owlet’s longer-term outlook is regulatory differentiation. The company remains the first and only FDA-cleared over-the-counter infant monitoring device on the market. This distinction gained added relevance after the FDA issued a safety communication cautioning against unauthorized infant monitors. Management characterized this moment as a clear line of separation between regulated and unregulated products, strengthening Owlet’s brand credibility and reinforcing barriers to entry.

For parents, retailers and healthcare partners, FDA clearance enhances trust. For investors, it supports the idea that Owlet’s market share gains may be more durable than those of unregulated competitors, particularly as consumer awareness around safety increases.

Beyond hardware, Owlet is building a recurring revenue layer through its Owlet360 subscription. Paying subscribers have surpassed 85,000, with attach rates exceeding 25% by the end of the fiscal third quarter. Management emphasized that this opportunity is still early, given a global installed base of more than 650,000 active devices. Subscription momentum is expected to broaden as Owlet rolls out services internationally and layers in camera-based features tied to Dream Sight’s onboard AI capabilities.

Looking into 2026, Owlet plans to pilot generative AI features designed to deliver personalized sleep insights and coaching. These initiatives aim to increase engagement, retention and customer lifetime value, shifting the business mix further toward higher-margin software and services.

International expansion is another meaningful growth lever. Third-quarter international revenue surged sharply year over year, supported by new product launches and distributor load-ins. Regulatory approval in India opens an additional large market starting in early 2026, adding to Owlet’s growing list of international clearances.

At the same time, the company is making early progress in healthcare channels. The launch of hospital partnerships and remote patient monitoring initiatives introduces an insurance-reimbursed use case that could materially expand Owlet’s addressable market over time. While still early, management views healthcare as a long-term growth pillar rather than a near-term revenue driver.

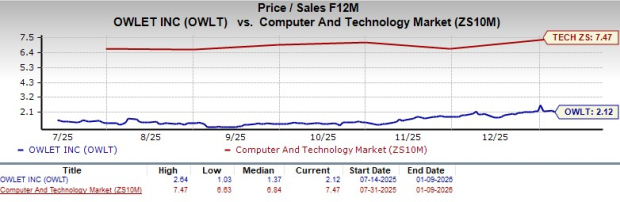

Despite the stock’s sharp rise, valuation remains relatively modest. Owlet trades at a forward 12-month price-to-sales multiple well below the broader technology sector average, suggesting the market is not fully pricing in the company’s improving margin profile, subscription upside or healthcare optionality. This valuation backdrop provides some cushion if execution remains on track.

Estimate revisions further support the bullish narrative. Over the past month, the Zacks Consensus Estimate for 2026 losses has narrowed meaningfully (as shown below), while revenue estimates point to continued double-digit growth (21.1% growth). These trends reflect growing confidence in Owlet’s path toward sustained profitability.

While the outlook has improved, risks remain. Tariff pressures continue to weigh on margins, and management has acknowledged that elevated import costs will persist into upcoming quarters. Consumer demand can also be sensitive to broader macro conditions, particularly for discretionary baby products. Execution risk around subscription expansion, international scaling and healthcare partnerships remains, especially as the company invests in new technology and regulatory pathways.

Competition in connected infant monitoring and digital health remains intense, with brands such as Masimo MASI, iRhythm Technologies IRTC and Koninklijke Philips N.V. PHG shaping different parts of the market. Masimo is a leader in medical-grade pulse oximetry and patient monitoring, and Masimo’s deep hospital relationships highlight the complexity of scaling regulated monitoring solutions. While Masimo operates primarily in clinical environments, its presence underscores the high regulatory and technical bar Owlet must continue to meet as it expands healthcare partnerships.

iRhythm Technologies operates in remote cardiac monitoring, but it offers a useful comparison in terms of subscription-driven, data-centric monitoring models that scale through reimbursement pathways. Meanwhile, Koninklijke Philips remains a broad-based healthcare technology provider with monitoring solutions spanning hospitals and consumer wellness, though its infant-focused offerings are not as specialized as Owlet’s.

Owlet’s differentiation lies in combining FDA-cleared consumer hardware with a growing subscription ecosystem focused specifically on infant health. Against Masimo, iRhythm Technologies and Koninklijke Philips, Owlet remains more narrowly focused, but that specialization may support deeper engagement and longer customer lifetimes if execution remains strong.

Owlet’s 82% rally over the past six months reflects real progress rather than hype. Strong execution, regulatory leadership, improving margins and a favorable estimate revision trend support the stock’s momentum. While risks tied to tariffs and execution remain, valuation remains reasonable relative to growth prospects. With a Zacks Rank #1 (Strong Buy), the stock continues to offer an attractive risk-reward profile for investors willing to tolerate small-cap volatility. You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-21 | |

| Jul-17 | |

| Jul-16 | |

| Jul-08 | |

| Jul-03 | |

| Jun-30 | |

| Jun-22 | |

| Jun-17 | |

| Jun-16 | |

| Jun-09 | |

| Jun-09 | |

| Jun-09 | |

| Jun-09 | |

| Jun-09 | |

| Jun-08 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite