|

|

|

|

|||||

|

|

|

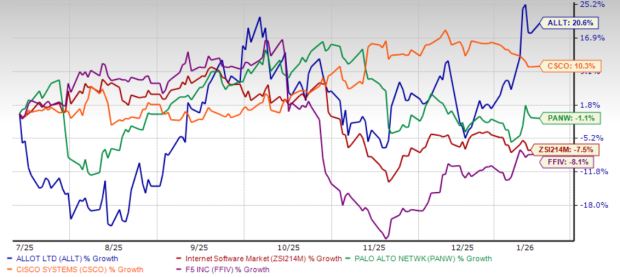

Allot Ltd. ALLT shares have gained 20.6% in the past six months, outperforming the Zacks Internet - Software industry’s decline of 7.5%. The stock has outperformed its peers as well, including Cisco Systems CSCO, F5 FFIV and Palo Alto Networks PANW. In the past six months, shares of Cisco Systems have gained 10.3%, while shares of F5 and Palo Alto Networks have lost 8.1% and 1.1%, respectively.

The outperformance of Allot’s share price raises the question: Should investors continue accumulating ALLT stock?

What’s fueling this strength is strong traction in Allot’s Cybersecurity-as-a-Service (SECaaS) business. Allot’s SECaaS business is scaling rapidly across telecom customers and contributing to total revenue growth.

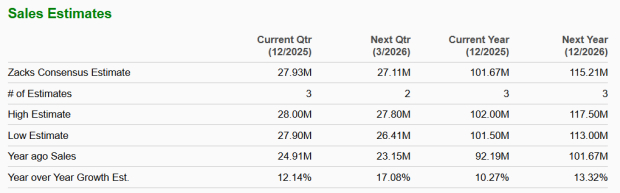

In the last reported financial results for the third quarter of 2025, the company’s net sales soared 14% year over year to $26.4 million and surpassed the Zacks Consensus Estimate of $26 million. Similarly, non-GAAP earnings per share (EPS) jumped to 10 cents compared with the year-ago quarter’s EPS of 3 cents. ALLT’s bottom line beat the consensus mark by 150%.

Considering a strong demand for its solutions and a better-than-expected third-quarter performance, Allot raised its guidance for 2025. The company now expects 2025 revenues to be in the range of $100-$103 million, up from its previous guidance of $98-$102 million. Allot raised its guidance for SECaaS annual recurring revenue (ARR) growth as well. The company now expects SECaaS ARR growth to surpass 60% on a year over year basis, up from its prior guidance of 55-60%.

Allot is seeing steady progress in its SECaaS business, which is becoming the company’s main growth driver. In the third quarter of 2025, SECaaS ARR increased about 60% year over year. The growth was primarily driven by higher adoption from telecom partners and more end users signing up for security services.

SECaaS made up around 28% of Allot’s total revenues in the third quarter. Looking ahead, management expects this share to move closer to 30% if current trends continue, which bodes well for the company's prospects in the upcoming quarters. This is crucial because SECaaS is a subscription-based offering, which makes revenues more predictable. Recurring revenues accounted for 63% of total revenues in the third quarter compared with 58% a year ago, showing a gradual improvement in revenue quality.

During the third quarter earnings call, management outlined a few clear drivers behind SECaaS growth. Large Tier-1 telecom customers that launched services in recent quarters are continuing to add new subscribers, which is driving demand for Allot’s solutions. Existing customers are also buying additional services over time, which supports upselling. Allot is also introducing new offerings, such as OffNetSecure, which allows protection even when users are off the operator’s network. This broadens the use of SECaaS and could help increase revenue per user over time.

If telecom partners continue to scale these services and user adoption remains steady, SECaaS momentum could continue to support ALLT’s ARR growth in the coming quarters. The Zacks Consensus Estimate for 2026 indicates revenue growth of 13.3%.

The Zacks Consensus Estimate for Allot’s 2026 earnings implies a year-over-year increase of 15.9%. The estimates for 2026 have been revised upward by a penny over the past 60 days, indicating that analysts are optimistic about its prospects in 2026.

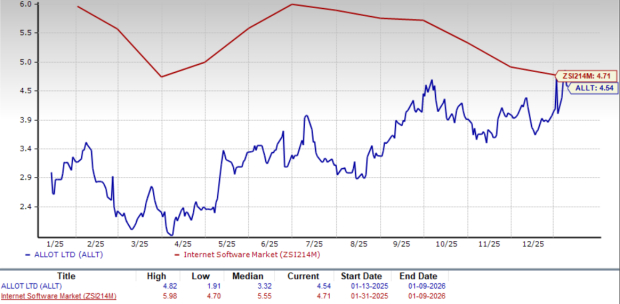

Despite its strong growth, ALLT stock still looks reasonably priced. Allot is currently trading at a lower price-to-sales (P/S) multiple compared to the industry. Allot’s forward 12-month P/S ratio sits at 4.54X, lower than the industry’s forward 12-month P/S ratio of 4.71X.

Allot stock trades at a lower P/S multiple compared with its peers, including Cisco Systems, F5 and Palo Alto Networks. At present, Cisco Systems, F5 and Palo Alto Networks have P/S multiples of 4.74X, 4.93X and 11.82X, respectively. This discount adds to the appeal for long-term investors.

Allot is seeing strong growth in its SECaaS business, which is driving higher revenues, rising recurring income, and better earnings visibility. Rising customer interest in newer cybersecurity offerings, such as OffNetSecure, creates opportunities to sell more services to existing customers, which bodes well for the company's prospects. Allot’s reasonable valuation offers some downside protection as well. This discounted pricing makes ALLT an attractive buy, particularly for investors seeking exposure to cybersecurity growth at a fair price.

Allot currently sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| Aug-03 |

Dell Leaps Amid AI Server Demand Surge; Two More Stocks On Watch For Rising Profit

PANW

Investor's Business Daily

|

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-02 | |

| Aug-01 | |

| Jul-31 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite