|

|

|

|

|||||

|

|

|

Micron Technology, Inc.’s MU shares soared over 200% in 2025, emerging as one of the standout S&P 500 performers and easily outpacing Wall Street favorite NVIDIA Corporation NVDA. But does Micron still have room to grow, and is now the right time to invest? Let’s see –

Micron’s shares scaled northward in recent times, driven by robust quarterly performances as relentless demand for its high-bandwidth memory (HBM) chips surged. These chips are highly sought after due to their ability to process massive data workloads while significantly reducing power consumption.

Micron’s revenues for the fiscal first-quarter 2026 were $13.64 billion, up 56.8% year over year, and more than analysts’ expectations of around $12.88 billion, as cited in investors.micron.com. All four business segments posted revenue growth, with the coveted cloud memory business unit reporting sales of $5.28 billion, up a stellar 99.5% year over year. The strong revenue performance pushed Micron's non-GAAP net income to $5.48 billion, or $4.78 per diluted share, comfortably surpassing analysts’ expectations of $3.94.

But the surging demand for HBM chips shows no signs of slowing as it remains in short supply amid the AI infrastructure boom. This has reassured investors that Micron’s shares are well-positioned to climb higher, driven by the strong performance of its products. Micron, in fact, expects strong results for its fiscal second-quarter 2026, with revenues expected between $18.3 billion and $19.1 billion, and diluted earnings per share (EPS) estimated at $8.22 to $8.62.

The HBM market itself is expected to grow significantly, and that bodes well for Micron’s growth prospects. According to Market Growth Reports, the HBM market is anticipated to witness a CAGR of 25.5% to $7,721.41 million by 2035 from $1,516.31 million in 2026. Additionally, Micron reported a record cash flow of $3.9 billion in its fiscal first-quarter 2026, giving the company substantial resources to fuel future growth initiatives.

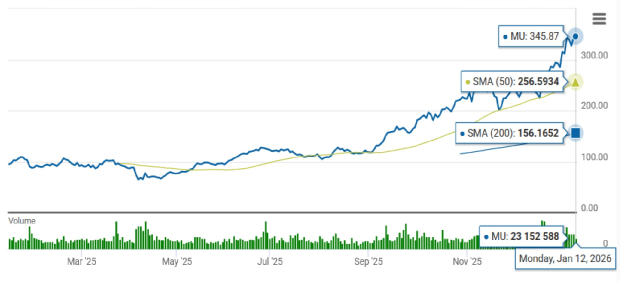

From a technical perspective, Micron’s shares are currently trading well above the long-term 200-day moving average (DMA) and the short-term 50 DMA, signaling an uptrend.

Image Source: Zacks Investment Research

With Micron’s shares well-positioned to climb on strong demand for HBM chips and healthy cash flow positioning, it's prudent for astute investors to buy the stock now. And why not? The stock trading above key moving averages positions it for further gains amid the AI-driven memory boom.

What’s more, Micron is still trading at a discount or remains undervalued. Micron’s forward price-to-earnings (P/E) ratio of 11.03 is less than the Computer-Integrated Systems industry’s average of 17.89. This makes it an alluring growth stock for investors without overpaying.

Image Source: Zacks Investment Research

Currently, Micron has a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 53 min | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 1 hour | |

| 5 hours | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite