|

|

|

|

|||||

|

|

|

Meta Platforms META is one of the prolific hyperscalers spending massively on AI infrastructure, including data centers that are pivotal to bringing personal superintelligence and a better app experience to everyone across its platforms. These data centers consume huge amounts of electricity, and META is now tapping nuclear energy to fulfill this requirement. The company has signed long-term nuclear power agreements with Vistra VST, TerraPower and Oklo OKLO that are designed to supply up to 6.6 gigawatts (GWs) of nuclear electricity by 2035. The addition of clean and reliable nuclear energy to the grid also provides a boost to META’s ESG profile. So, does META’s expanded energy strategy make the stock attractive for investors? Let’s find out.

The nuclear energy deals with Vistra, TerraPower, Oklo and Constellation (20-year agreement beginning 2027) make Meta Platforms one of the most significant corporate purchasers of clean energy. The deals will help META in securing reliable and stable electricity over long-term thereby reducing risks related to volatility in grid prices, energy shortages, and fluctuating fossil fuel prices that can squeeze margins and cash flow generation ability. Meta Platforms’ 20-year power purchase agreements with Vistra and investments in new reactor projects with Oklo and TerraPower offer a glimpse into META’s sustainable energy plans that will power AI systems like the Prometheus supercluster.

Meta Platforms’ backing of TerraPower’s advanced nuclear technology and Oklo’s Aurora powerhouses drives innovation. META is providing funds to support the development of two new Natrium units capable of generating up to 690 MW of firm power with delivery as early as 2032. The company has the right to gather energy from up to six other Natrium units capable of producing 2.1 GW and targeted for delivery by 2035. Oklo’s advanced nuclear technology campus, expected to come online by 2030, is expected to generate up to 1.2 GW of clean energy.

The energy deals are expected to solve Meta Platforms’ energy issues. The company is spending heavily on AI research, models and infrastructure and now expects 2025 capital spending between $70 billion and $72 billion. Per CNBC, Alphabet GOOGL, Meta Platforms, Amazon and Microsoft on a combined basis are expected to spend roughly $380 billion on developing AI infrastructure in 2025.

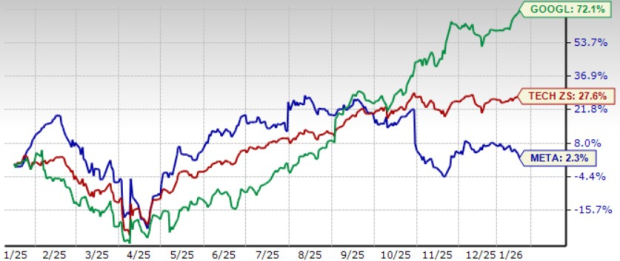

Meta Platforms shares have returned a meager 2.3% in the trailing 12-month period, underperforming the broader Zacks Computer & Technology sector’s appreciation of 27.6% and Alphabet’s return of 72.1%.

META’s prospects have been suffering from huge capital expenditure, growing fears of an AI bubble, regulatory issues (in the European Union and the United States) and stiff competition in the ad market as well as the AI space. For 2026, META expects significant growth in capital expenditure in dollar terms compared with 2025. Growth in operating expenses is expected to be substantial due to higher infrastructure costs and employee compensation costs.

However, Meta Platforms’ growing footprint among young adults, driven by improving recommendations, boosts its competitive prowess. AI usage is making it a popular name among advertisers. This is expected to drive top-line growth.

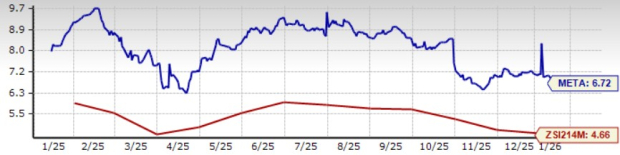

Meanwhile, META shares are overvalued, as suggested by the Value Score of C. In terms of the forward 12-month price/sales (P/S), META is trading at 6.72X, a premium compared with the Internet Software industry’s 4.66X.

The Zacks Consensus Estimate for 2025 earnings is pegged at $23.04 per share, down by 4.3% over the past 60 days, suggesting a 3.4% decline from the figure reported in 2024. The consensus mark for 2025 revenues is pegged at $199.46 billion, suggesting 21.3% growth over 2024.

Meta Platforms, Inc. price-consensus-chart | Meta Platforms, Inc. Quote

The Zacks Consensus Estimate for 2026 earnings is pegged at $30.17 per share, down by 6 cents over the past 60 days, suggesting 30.94% growth from the consensus estimate in 2025. The consensus mark for 2026 revenues is pegged at $235.17 billion, suggesting 17.9% growth over 2025’s consensus estimate.

Meta Platforms is spending heavily on expanding AI infrastructure, and the nuclear energy deals improve earnings visibility over the long term. However, aggressive spending is hurting earnings prospects in the near term. This, along with stiff competition in the ad market and a stretched valuation, is a headwind for prospective investors.

META currently has a Zacks Rank #3 (Hold), which implies that investors should wait for a more favorable entry point to accumulate the stock. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 5 hours | |

| 14 hours | |

| 14 hours |

Dow Jones Futures: Market Triggers Sell Signal; Apple Earnings, Iran News, Fed Meeting In Focus

META

Investor's Business Daily

|

| 14 hours | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

What to watch next week: Big Tech earnings, the Fed, and Consumer Confidence

META GOOGL

Yahoo Finance Video

|

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite