|

|

|

|

|||||

|

|

|

FuelCell Energy FCEL has staged a notable rebound heading into 2026, supported by rising investor interest in AI-driven power demand and improving earnings estimates. The stock’s recovery has also renewed comparisons with companies, such as Bloom Energy BE and Plug Power PLUG, which investors often track when assessing long-duration clean power and hydrogen-linked technologies. With FCEL still unprofitable, the market is balancing its long-term potential against ongoing financial pressure.

FuelCell Energy sits at the crossroads of clean, always-on power and data center infrastructure. As demand grows for on-site power solutions that can support energy-hungry data centers, the recent rally puts the spotlight on whether the company’s business performance is starting to support the optimism behind the stock.

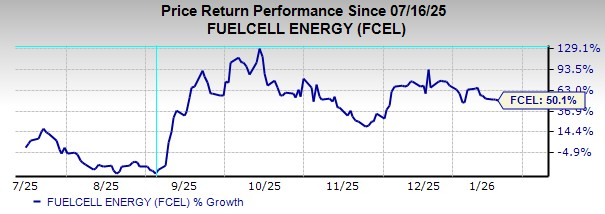

FCEL shares have been volatile but directionally stronger over the past six months. The stock is up 50% during that period, rebounding sharply from levels under $4 in September to around $7.50 recently. Despite this rally, FuelCell still trades nearly 40% below its October highs, highlighting lingering skepticism.

Over the past three months, the stock has remained down more than 30%, underperforming Bloom Energy, which gained 14%, while faring better than Plug Power, which fell 39%.

This mixed performance shows a market that is open to FCEL’s long-term potential tied to AI-driven power demand, but still cautious about the company’s ability to execute. While recent gains suggest renewed interest, sharp pullbacks and relative performance versus Bloom Energy and Plug Power highlight ongoing uncertainty and selective investor positioning.

Management has been explicit that manufacturing scale is central to FuelCell’s path toward positive adjusted EBITDA. The Torrington, CT facility is currently operating at a 41-megawatt (MW) annualized production rate. According to management, positive adjusted EBITDA becomes achievable at roughly 100 MW of annualized output, placing the company about 40% of the way toward that threshold.

The Torrington facility has the physical capacity to expand to as much as 350 MW annually with additional capital investment. This creates operating leverage, as higher utilization allows fixed manufacturing costs to be absorbed more efficiently. Unlike Bloom Energy, which already operates at a much larger scale, FCEL’s profitability remains highly sensitive to execution on utilization gains.

FuelCell Energy is promoting its carbonate fuel cell technology as a way to supply on-site power for data centers, where grid limits and long connection delays are pushing customers to look for other options. Management said that pricing proposals covering hundreds of megawatts are currently under discussion with large data center operators, utilities, and infrastructure partners.

Although these discussions have not yet turned into signed contracts, they show that FCEL is involved in many of the same opportunities driving interest in competitors like Bloom Energy. This creates potential upside if deals move forward, even as competition remains strong. Turning proposals into confirmed orders would likely improve investor confidence.

One of FCEL’s clearest strengths is liquidity. The company exited fiscal 2025 with $278.1 million in unrestricted cash and $63.7 million in restricted cash, supported by aggressive equity issuance. During the fourth quarter alone, the company sold 16.4 million shares, generating $136.9 million in gross proceeds.

This cash buffer materially reduces near-term solvency risk, an important distinction versus Plug Power, which continues to face heavier cash burn pressure. However, the trade-off is dilution. While markets often reward balance sheet stability, ongoing reliance on equity financing can cap upside, particularly when compared with Bloom Energy’s stronger operating profile.

Despite some operational progress, FuelCell Energy remains unprofitable. In fiscal 2025, the company posted a net loss of $191.4 million and negative adjusted EBITDA of $74.4 million. Gross margins are still below zero, highlighting that the business has yet to reach a scale where operations can support themselves.

That said, earnings expectations are steadily improving. Estimates for fiscal 2026 losses have been reduced meaningfully in recent months, and projections for 2027 have improved even more. FCEL has also delivered better-than-expected results in the most recent quarters, suggesting execution is stabilizing. While profitability is still a long-term goal, these trends point to gradual financial improvement and set FCEL apart from some competitors like Plug Power that continue to struggle with consistency.

Finally, FuelCell Energy belongs to the Zacks Alternative Energy – Other industry, which sits in the top 42% of more than 240 Zacks industries. Within this context, improving earnings estimates and strong liquidity support a more constructive view, even as losses persist.

FuelCell Energy offers high upside potential if manufacturing scales and demand from data centers continues to grow, but that opportunity comes with meaningful risks tied to execution and possible dilution. The stock is not without volatility, yet improving earnings trends and rising interest in behind-the-meter power solutions strengthen the longer-term case. Given this balance, FuelCell Energy currently carries a Zacks Rank #2 (Buy). For investors with a higher risk tolerance and a longer time horizon, FCEL offers attractive optionality as the company works toward commercial traction and improved fundamentals heading into 2026.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-20 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-16 | |

| Jul-16 | |

| Jul-15 | |

| Jul-14 | |

| Jul-14 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite