|

|

|

|

|||||

|

|

|

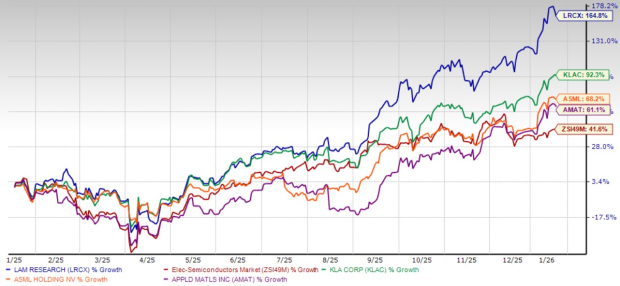

Lam Research Corporation LRCX has witnessed a remarkable run over the past year, showcasing a staggering 164.8% surge in its stock price. The stock has outperformed the Zacks Electronics – Semiconductors industry’s gain of 41.6% in the trailing 12 months.

It has even outpaced major semiconductor manufacturing tool providers, including KLA Corporation KLAC, ASML Holding ASML and Applied Materials, Inc. AMAT. Shares of KLA Corporation, ASML Holding and Applied Materials have rallied 92.3%, 68.2% and 61.1%, respectively.

This outperformance shows investors are becoming increasingly confident in Lam Research’s long-term prospects, even in a volatile market shaped by trade conflicts and geopolitical risks. We believe that LRCX stock will sustain this upward trajectory at least in the near term, making it worth buying for now.

Despite ongoing macroeconomic challenges, geopolitical issues, and trade and tariff wars, LRCX’s financials remain impressive. In the company’s last reported financial results for the first quarter of fiscal 2026, total revenues rose 28% year over year to $5.32 billion and beat the Zacks Consensus Estimate by 2%, primarily driven by continued demand across the Systems and Customer Support Business Group segments.

Lam Research reported first-quarter non-GAAP earnings of $1.26 per share, which beat the consensus mark by 4.1%. The bottom line also increased 46.5% on a year-over-year basis.

Lam Research Corporation price-consensus-eps-surprise-chart | Lam Research Corporation Quote

Expanding its manufacturing operations in Asia has also helped the company lower costs and improve margins. In the first quarter, Lam Research’s non-GAAP operating margin rose to 35%, up 410 basis points from the year-ago quarter, which is impressive, considering the challenging macroeconomic environment.

This strong financial performance reinforces Lam Research’s resilience in navigating an evolving semiconductor cycle. As demand grows for advanced nodes, LRCX’s specialized technology in etch and deposition tools for high-aspect-ratio structures positions it well to capitalize on this trend. The company’s first-quarter results also highlight its effective cost management, which has enabled sustained profitability even amid fluctuating end-market demand.

Lam Research is capitalizing on AI trends. It builds the tools chipmakers need to manufacture next-generation semiconductors, including high-bandwidth memory (HBM) and chips used in advanced packaging. These technologies are vital for powering AI and cloud data centers.

Lam Research’s products are not only critical but also innovative. For example, its ALTUS ALD tool uses molybdenum to improve speed and efficiency in chip production. Another product, the Aether platform, helps chipmakers achieve higher performance and density. These are essential capabilities as demand for advanced AI chips continues to increase.

In 2024, Lam Research’s shipments for gate-all-around nodes and advanced packaging exceeded $1 billion, and management had expected this figure to triple to more than $3 billion in 2025. Additionally, the industry’s migration to backside power distribution and dry-resist processing presents growth opportunities for LRCX’s cutting-edge fabrication solutions.

These trends are aiding Lam Research’s financial performance. The company has demonstrated consistent execution, maintaining quarterly revenues of more than $5 billion for the past two consecutive quarters, reflecting solid demand from leading chipmakers such as Taiwan Semiconductor Manufacturing and Samsung.

With AI-driven investments accelerating, Lam Research’s leading position in etch and deposition makes it a key beneficiary of the ongoing semiconductor spending cycle. The Zacks Consensus Estimate for fiscal 2026 and 2027 revenues implies a year-over-year increase of 14.1% and 12.5%, respectively. The consensus mark for fiscal 2026 and 2027 earnings per share indicates growth of 15.9% and 15.2%, respectively.

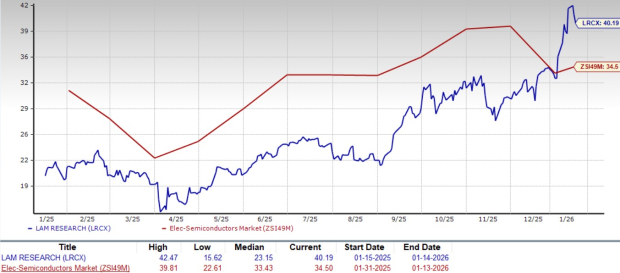

Lam Research stock currently trades at a premium to the industry. Its forward 12-month price-to-earnings (P/E) ratio of 40.19 exceeds the industry’s average of 34.5. However, the company’s strong growth prospects amid AI-driven demand for advanced nodes justify this premium valuation.

Compared with major semiconductor equipment providers, LRCX trades at a lower P/E multiple than ASML, while at a premium to KLAC and AMAT. At present, ASML Holding, KLA Corporation and Applied Materials have forward 12-month P/E multiples of 41.13, 37 and 30.42, respectively.

Lam Research’s solid financial performance, strategic focus on AI-driven growth and reasonable valuation make it a compelling investment option right now. The company’s expanding market share in AI and datacenter fabrication, coupled with innovative product launches, strengthens its competitive positioning.

LRCX carries a Zacks Rank #2 (Buy) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 37 min | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 |

Lam Research Stock Jumps On Fiscal Q4 Beat-And-Raise Report

LRCX -6.40% LRCX +6.40% AH

Investor's Business Daily

|

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite