|

|

|

|

|||||

|

|

|

RingCentral trades at $28.85 per share and has stayed right on track with the overall market, gaining 11.6% over the last six months. At the same time, the S&P 500 has returned 11.5%.

Is there a buying opportunity in RingCentral, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

We're cautious about RingCentral. Here are three reasons there are better opportunities than RNG and a stock we'd rather own.

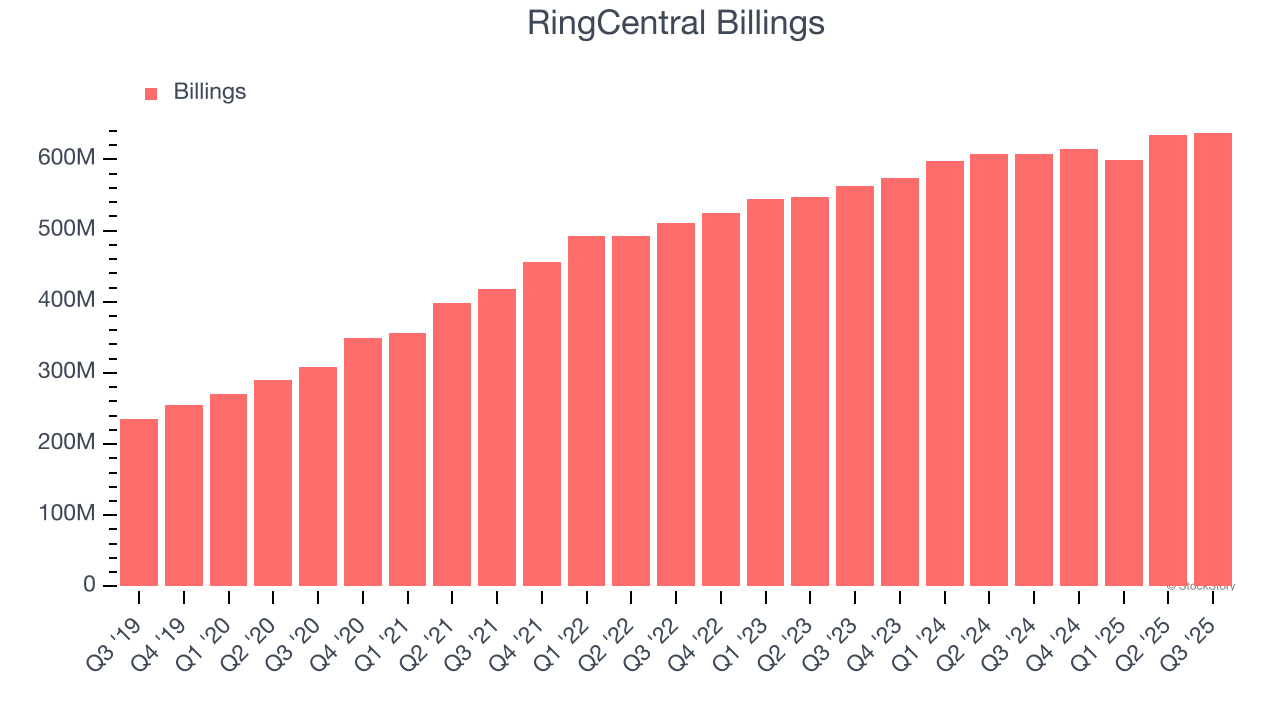

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

RingCentral’s billings came in at $637.7 million in Q3, and over the last four quarters, its year-on-year growth averaged 4.2%. This performance was underwhelming and suggests that increasing competition is causing challenges in acquiring/retaining customers.

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect RingCentral’s revenue to rise by 4.4%, a deceleration versus its 17.7% annualized growth for the past five years. This projection doesn't excite us and implies its products and services will face some demand challenges.

The customer acquisition cost (CAC) payback period represents the months required to recover the cost of acquiring a new customer. Essentially, it’s the break-even point for sales and marketing investments. A shorter CAC payback period is ideal, as it implies better returns on investment and business scalability.

RingCentral’s recent customer acquisition efforts haven’t yielded returns as its CAC payback period was negative this quarter, meaning its incremental sales and marketing investments outpaced its revenue. The company’s inefficiency indicates it operates in a highly competitive environment where there is little differentiation between RingCentral’s products and its peers.

RingCentral falls short of our quality standards. That said, the stock currently trades at 1× forward price-to-sales (or $28.85 per share). While this valuation is reasonable, we don’t see a big opportunity at the moment. There are more exciting stocks to buy at the moment. Let us point you toward a dominant Aerospace business that has perfected its M&A strategy.

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.

| Jul-27 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-21 | |

| Jul-16 | |

| Jul-09 | |

| Jul-09 | |

| Jul-09 | |

| Jun-23 | |

| Jun-08 | |

| Jun-02 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite