|

|

|

|

|||||

|

|

|

Haemonetics Corporation’s HAE impressive potential of the Plasma franchise is poised to drive growth in the upcoming quarters. The robust uptake of the Hemostasis Management Franchise bodes well for its long-term growth. However, a dull macroeconomic scenario and fierce competitive pressure remain concerns for HAE’s operations.

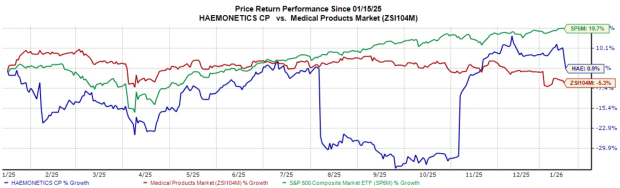

In the past year, this Zacks Rank #3 (Hold) company’s shares have gained 0.9% against the industry decline of 5.4%. The S&P 500 composite has grown 19.7% in the same time frame.

The global provider of blood and plasma supplies and services has a market capitalization of $4.08 billion. HAE beat on earnings in three of the trailing four quarters and matched once, delivering an average surprise of 6%.

Let us delve deeper.

Potential Upsides of Plasma Franchise: Haemonetics’ Plasma business unit focuses on the collection of source plasma for pharmaceutical manufacturers using apheresis devices that only collect plasma. In fiscal 2025, the company signed new long-term agreements with BioLife and Grifols, reinforcing its continued close partnership and highlighting the ability to bring innovation to plasma collections.

Meanwhile, Haemonetics achieved meaningful progress, transitioning both domestic and international customers to Persona and Express Plus. In line with this, it now has 40 million collections on Persona and over 1 million on Express Plus.

The ongoing enhancements in the NexSys platform are expanding its competitive advantage as the global industry standard for plasma collection. Haemonetics was also named the exclusive plasma collection partner for the Japanese Red Cross, later expanding to include Fresh Frozen Plasma.

Huge Potential of Hemostasis Management Franchise: One of the principal product lines in the company’s Hospital business, the hemostasis diagnostic systems portfolio enables clinicians to holistically assess a patient’s coagulation status in point-of-care or laboratory settings. The company markets four viscoelastic testing systems — the TEG 5000 hemostasis analyzer system, the TEG 6s hemostasis analyzer system, the ClotPro hemostasis analyzer system and the HAS-100 hemostasis analyzer system — to hospitals and laboratories as an alternative to routine blood tests.

In the fiscal second quarter, the business achieved 12% revenue growth in the United States, primarily driven by higher TEG disposable utilization and the ongoing rapid adoption of the global HN cartridge. Transfusion Management also achieved double-digit growth, supported by heightened demand for transfusion safety and efficiency.

Image Source: Zacks Investment Research

Dull Macroeconomic Scenario: The ongoing geopolitical constraints in China, Taiwan, Russia, Ukraine, the Middle East and other foreign jurisdictions where the company operates are materially affecting its operational results. Despite implementing cost-containment measures, selective price increases, and other actions to offset inflationary pressures in its global supply chain, the company is sometimes unable to fully offset increases in its operating costs. In addition, climate change could raise supply costs — including energy and transportation or freight-related expenses — or reduce the availability of raw materials.

Competitive Landscape: Haemonetics operates in a very competitive environment, both for manual and automated systems. Slower-than-expected product adoption by customers, especially the American Red Cross, might reduce the company’s revenues and profits.

The Zacks Consensus Estimate for fiscal 2026 earnings has remained unchanged at $4.93 per share in the past 30 days.

The Zacks Consensus Estimate for fiscal 2026 revenues is pegged at $1.32 billion, which indicates a 3.2% decrease from the year-ago reported number.

Some better-ranked stocks in the broader medical space are Phibro Animal Health PAHC, Boston Scientific BSX and Envista NVST.

Phibro Animal Health has an earnings yield of 7.4% compared with the industry’s 0.2% yield. Shares of the company have surged 86.2% in the past year against the industry’s 5% decline. PAHC’s earnings outpaced estimates in three of the trailing four quarters and missed on one occasion, the average surprise being 20.8%.

PAHC sports a Zacks Rank #1 (Strong Buy) at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Boston Scientific, currently carrying a Zacks Rank #2 (Buy), has an estimated long-term earnings growth rate of 16.4% compared with the industry’s 13.9% growth. Its earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, with the average surprise being 7.36%. BSX shares have surged 130.2% compared with the industry’s 5.2% growth in the past year.

Envista, carrying a Zacks Rank #2 at present, has an earnings yield of 5.4% compared with the industry’s 2.8% yield. Shares of the company have jumped 13.9% compared with the industry’s 5.2% growth. NVST’s earnings surpassed estimates in each of the trailing four quarters, with the average surprise being 12.8%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-03 | |

| Jul-31 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite