|

|

|

|

|||||

|

|

|

Ondas Inc. ONDS, through its Ondas Autonomous Systems (OAS) unit and Ondas Networks private wireless solutions, hosted its OAS Investor Day 2026. The company announced that it successfully launched and executed its core plus strategic growth plan, evolving OAS from a collection of specialized autonomous drone systems into a multi-domain global autonomy platform.

Also, the company issued preliminary financial results for 2025 and provided updated revenue targets for 2026. Ondas expects to report fourth-quarter 2025 revenue in the range of $27–$29 million, representing a 51% increase over its prior revenue target. For the full year ended Dec. 31, 2025, revenue is projected between $47.6 million and $49.6 million, exceeding the company’s earlier guidance by 23%. Notably, the prior revenue targets for both the fourth quarter and 2025 included an anticipated $3–$4 million contribution from Roboteam, which was acquired in December 2025.

Ondas’ backlog was approximately $65.3 million as of Dec. 31, 2025, marking a 180% increase from $23.3 million reported on Nov. 13, 2025, reflecting strengthening demand and improved revenue visibility. The company also ended the year with a pro forma cash balance exceeding $1.5 billion, adjusted for its recently completed equity offering of approximately $1 billion, providing substantial financial flexibility.

For 2026, Ondas has raised its revenue outlook to a range of $170–$180 million, representing a 25% increase over its previous target of $140 million, which included an estimated $30 million contribution from Roboteam. This upward revision underscores management’s confidence in accelerating growth across its autonomous systems and integrated platform strategy.

OAS is the company’s primary growth driver, which is benefiting from increased deployments of Iron Drone Raider and Optimus autonomous platforms, along with initial revenue contributions from recently acquired businesses such as Apeiro Motion.

Management stated that it expects strong results in the counter–unmanned aerial systems (C-UAS) segment, led by the Iron Drone and Sentrycs platforms. Momentum is also building across its ground robotics offerings, particularly within the Unmanned Ground Vehicle (UGV) portfolios from Roboteam and Apeiro, as customer adoption deepens and demand continues to mature. Additionally, management projects 4M Smart Demining to deliver solid performance as demining activity accelerates.

Red Cat Holdings, Inc. RCAT recently announced preliminary unaudited revenue results for the fourth quarter and full year ended Dec. 31, 2025, reflecting strong operational execution and surging demand. Fourth-quarter 2025 revenue is expected to range between $24 million and $26.5 million, significantly up from $1.3 million reported in the prior-year period, while 2025 revenue is projected to be between $38 million and $41 million, up about 153% from $15.6 million posted in 2024. Management attributed this robust performance to heightened demand from defense and government customers, expanding program wins and the company’s ability to rapidly scale production. For 2026, Red Cat expects continued growth supported by a stronger pipeline, improving operating leverage and its expanding role as a trusted supplier of next-generation unmanned systems.

Draganfly Inc. DPRO is a Canada-based developer of drone solutions and systems that is steadily strengthening its presence across defense, security and commercial markets. In the third quarter 2025, the company’s revenue was driven by strong momentum across defense, government and public safety markets, supported by expanding product adoption, new program wins and improved production scalability.

Key contributors included rising demand for NDAA-compliant drones, growing military orders (including FPV and heavy-lift platforms), border security deployments, reseller expansion through Drone Nerds and strategic partnerships that enhanced payload, AI and autonomy capabilities. The company also benefited from increased manufacturing capacity and its ability to support large, mission-critical defense contracts at scale. Management indicated that demand remains robust, with a rapidly expanding pipeline, expectations of significantly higher military contribution to revenue and capacity set to increase further in 2026, positioning the company for continued revenue growth going forward.

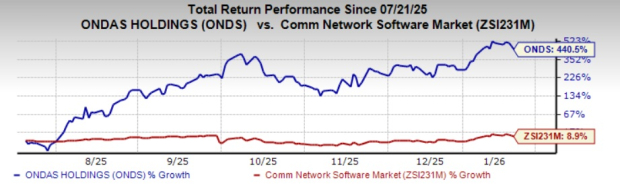

Shares of ONDS have surged 440.5% in the past six months compared with the Communication - Network Software industry’s growth of 8.9%.

In terms of the forward 12-month Price/Sales ratio, ONDS is trading at 31.03, considerably higher than the Communication - Network Software industry’s multiple of 2.25.

The Zacks Consensus Estimate for ONDS’ earnings for the current year has been revised north over the past 60 days.

ONDS currently has a Zacks Rank #3 (Hold).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-03 | |

| Aug-03 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-28 | |

| Jul-28 | |

| Jul-27 | |

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite