|

|

|

|

|||||

|

|

|

These companies have seen their growth rates decline significantly in recent years.

Neither company is profitable and both generate just single-digit gross profit margins.

Challenging economic conditions could make things even worse for these businesses in the near future.

Inflation has made eating out much more challenging for consumers to afford a decent meal while keeping their budgets intact. Trying to eat healthy is even more difficult, as paying for fresh ingredients can raise prices further.

It may not come as much surprise, then, to learn that two companies that have focused on healthy eating alternatives have performed so poorly last year. In 2025, shares of Sweetgreen (NYSE: SG) and Beyond Meat (NASDAQ: BYND) were both down nearly 80%.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now. Continue »

Both of these stocks come with risks, but which one is the better buy today? Let's take a closer look.

Image source: Getty Images.

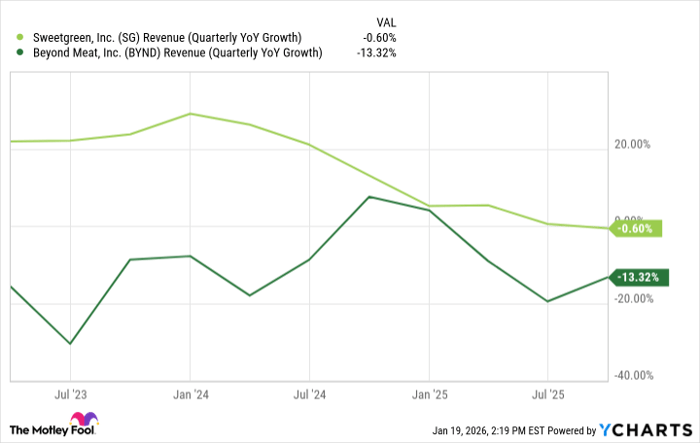

Both Sweetgreen and Beyond Meat experienced declines in their growth rates in recent quarters, and that's been a key reason behind their abysmal stock performances.

Fast-casual restaurant chain Sweetgreen has become known as the company that sells $20 salads, while Beyond Meat's alternative meat products have been facing tremendous competition, and there have been growing concerns about just how healthy its heavily processed products really are. The end result hasn't been pretty for either of these companies or their respective growth rates.

SG vs BYND: Revenue (Quarterly YoY Growth) data by YCharts

Sweetgreen gets the edge in terms of growth, simply because it hasn't gone deep into the negative.

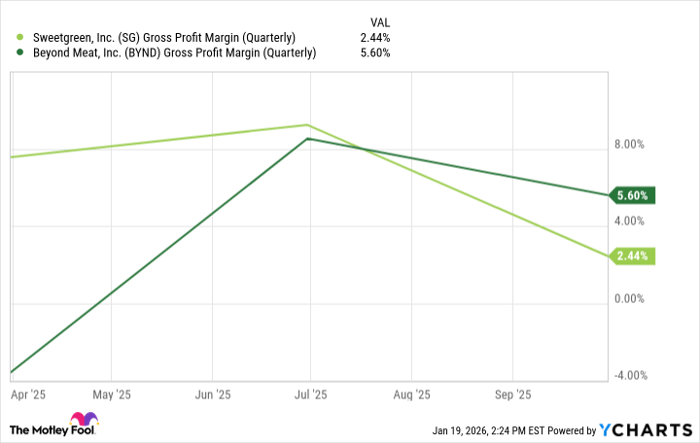

Both of these companies have been incurring losses in recent quarters. However, one number that may be of key importance to investors moving forward is the gross profit margin, which can provide an indication of which company may be better poised to get back to profitability in the near future.

SG vs BYND: Gross Profit Margin (Quarterly) data by YCharts

Beyond Meat has done better of late, but Sweetgreen also hasn't reported negative gross margins in recent quarters, which is a horrendous sight for investors. But with both companies' margins being incredibly low, I don't see one being in a terribly better position than the other; this looks like a tie.

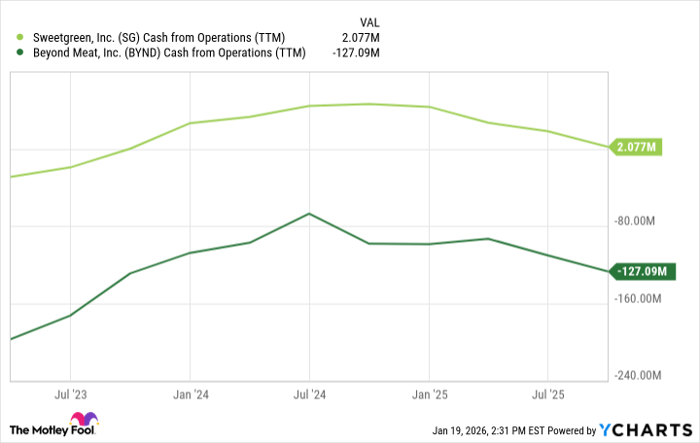

The biggest concern I'd have with businesses that are in such a troubled situation is whether they have strong enough financials to survive the next few years. If the economy is heading for a recession, things may get even worse before they get better for these businesses.

A key number to focus on here is operating cash flow. If a business is burning through a lot of cash, investors may need to brace for significant stock offerings (i.e., dilution), which will undoubtedly weigh down the share price.

SG vs BYND: Cash from Operations (TTM) data by YCharts

Sweetgreen has been generating positive cash flow over the trailing 12 months and has a clear advantage over Beyond Meat in terms of risk.

What's even more trouble for Beyond Meat is that its cash and cash equivalents balance as of the end of September was just $117 million. Without a slowdown in its burn rate, the company could conceivably burn through its cash in the next 12 months. While it can always take on debt or issue stock, neither option is an attractive one for investors.

If I were to invest in one of these stocks as a potential turnaround play, I'd pick Sweetgreen, easily. With stronger fundamentals and positive operating cash flow, it's a less risky option than Beyond Meat, which has struggled to grow even as it has been reducing prices and offering value packs -- a huge red flag.

While both of these stocks could very well struggle this year, if you're choosing a contrarian stock to go with, Sweetgreen may have a better chance of turning things around than Beyond Meat.

Before you buy stock in Sweetgreen, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Sweetgreen wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $474,578!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,141,628!*

Now, it’s worth noting Stock Advisor’s total average return is 955% — a market-crushing outperformance compared to 196% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of January 20, 2026.

David Jagielski, CPA has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Beyond Meat. The Motley Fool recommends Sweetgreen. The Motley Fool has a disclosure policy.

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-17 | |

| Jul-16 | |

| Jul-16 | |

| Jul-15 | |

| Jul-14 | |

| Jul-10 | |

| Jul-09 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite