|

|

|

|

|||||

|

|

|

Centerra Gold Inc. CGAU and IAMGOLD Corporation IAG are two North American gold-focused miners that continue to attract investor attention as the broader precious metals sector benefits from strong gold prices, improving cost structures and expanding production pipelines.

Gold prices have skyrocketed to unprecedented levels, driven by global economic uncertainties and trade and geopolitical tensions. Against this backdrop, comparing these two miners is particularly relevant for investors seeking exposure to the precious metals sector.

Let’s dive deep and closely compare the fundamentals of these two Canada-based miners to determine which one is a better investment now.

Centerra Gold posted a strong third quarter, underpinned by consistent production, meaningful cash generation across its core assets and favorable metal prices. The company benefited from solid operating results by producing 49,234 ounces at the Öksüt Mine, where higher grades and smooth plant performance supported strong quarterly output. At the flagship Mount Milligan Mine, the company produced 32,539 ounces of gold and 13.4 million pounds of copper. Gold and copper production remained steady, even as the team navigated areas of more complex mineralization.

A key development during the period was the advancement of Mount Milligan’s long-term permitting and technical work, which reinforced the asset’s importance by extending operational visibility to 2045, increasing reserves and authorizations for a 10% processed throughput expansion by 2028. Complementing these operational achievements, Centerra continued to advance its growth pipeline, notably the Goldfield District Project in Nevada, which is moving toward construction following strong economic study results, and ongoing evaluation work at the Kemess property.

Mount Milligan has secured an amended environmental assessment and all related permits, allowing the continuation of its operations through 2035. CGAU continues to advance engineering and other studies to support future permit authorizations needed to achieve the mine life extension of Mount Milligan to 2045.

At the end of the third quarter, CGAU’s cash and cash equivalents were around $561.8 million. Its long-term debt-to-capitalization was 2.3%. Free Cash Flow in the third quarter was about $99 million. Also, it had an undrawn credit facility of $400 million, bringing total liquidity to nearly $962 million, which provides flexibility to fund operations, growth projects and potential strategic initiatives without the need for additional debt.

IAMGOLD delivered a robust operational performance in the third quarter of 2025, with total attributable gold production of approximately 190,000 ounces. The company’s flagship Côté Gold Mine in Ontario was the standout performer, witnessing a record quarterly output of about 106,000 ounces on a 100% basis (75,000 attributable ounces) as mill throughput and recoveries improved significantly over the prior year, supported by ramp-up progress and processing optimization efforts.

At the Essakane Mine in Burkina Faso, attributable production reached 92,000 ounces, despite operational headwinds linked to lower grades earlier in the year and higher mining costs, while the Westwood Complex in Quebec contributed approximately 23,000 ounces amid efforts to address geological and operational challenges affecting grade and throughput.

The company recently reported preliminary 2025 attributable gold production of 765,900 ounces, achieving the mid-point of its guidance on record quarterly production across its operations. Côté Gold achieved the top end of its guidance, producing 87,200 attributable ounces in the fourth quarter and 279,900 attributable ounces in 2025. IAG sees total attributable gold production of 720,000 to 820,000 ounces in 2026.

At the Côté Gold mine, the company reached a major milestone in June 2025, with the processing plant operating at sustained nameplate capacity, supporting higher output, lower costs and additional optimization investments such as expanded crushing capacity. In Québec, IAMGOLD expanded its exploration footprint by acquiring Northern Superior Resources, consolidating the Philibert, Chevrier and Croteau deposits into the new Nelligan Mining Complex, and by purchasing Mines d’Or Orbec, adding the Muus Project to its portfolio. Continued drilling at Nelligan and Monster Lake has extended mineralization and improved resource potential in a tier-one jurisdiction.

At the end of the third quarter, IAG’s cash and cash equivalents were around $314 million. The long-term debt-to-capitalization was 21.3%. Mine-site free cash flow in the third quarter was a record $292 million.

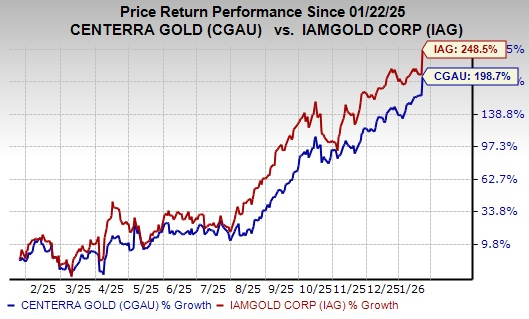

CGAU stock is up 198.7% in the past year, and IAG is up 248.5%.

CGAU is currently trading at a forward 12-month sales multiple of 2.91X, whereas IAG is presently trading at a forward 12-month sales multiple of 4.47X.

The Zacks Consensus Estimate for CGAU’s fiscal 2026 EPS suggests a 47.8% year-over-year rise. EPS estimates for fiscal 2026 have been trending higher over the past 60 days.

The consensus estimates for IAG’s fiscal 2026 EPS imply a year-over-year rise of 98.1%. EPS estimates for 2026 have been trending northward over the past 60 days.

Centerra Gold holds a stronger edge over IAMGOLD in the current macro and micro setup. Gold prices remain well supported by geopolitical and trade uncertainties, and expectations of a more dovish Federal Reserve, a backdrop that generally rewards companies with stronger balance sheets and cash flows. CGAU benefits significantly from this environment, given its lower leverage, higher liquidity, disciplined cost structure and diversified production base across Mount Milligan and Öksüt, which together provide more stable margins and predictable output. In contrast, IAG offers meaningful upside potential through the continued ramp-up of the Côté Gold project, which could transform its production profile, but this introduces considerable execution and cost-overrun risk.

Additionally, IAG’s leverage remains higher and its valuation less compelling compared to CGAU. While both companies may benefit from elevated gold prices, Centerra’s operational stability, cleaner balance sheet and lower geopolitical exposure collectively position it as the more reliable and attractive choice in the current market environment.

CGAU currently sports a Zacks Rank of #1 (Strong Buy), while IAG carries a Zacks Rank of #3 (Hold).

You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-23 | |

| Jul-15 | |

| Jul-14 | |

| Jul-13 | |

| Jul-09 | |

| Jul-07 | |

| Jul-06 | |

| Jul-06 | |

| Jun-26 | |

| Jun-19 | |

| Jun-17 | |

| Jun-12 | |

| Jun-02 | |

| Jun-01 | |

| Jun-01 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite