|

|

|

|

|||||

|

|

|

Ovintiv Inc. OVV is a major independent oil and gas producer with a diversified asset base spanning the United States and Canada. Historically weighted toward natural gas, the company has deliberately repositioned its portfolio toward liquids, prioritizing crude oil to enhance margins and cash flow stability. This transition has strengthened its standing among leading North American exploration and production companies, supported by core holdings in two of the continent’s most attractive undeveloped basins — the Permian Basin in Texas and the Montney formation in Western Canada.

Against a backdrop of shifting macroeconomic signals and changing energy market trends, stock selection has become increasingly consequential for investors. Ovintiv’s ongoing portfolio realignment, efforts to fine-tune its commodity mix and improving operational momentum introduce both opportunity and uncertainty into the investment case. These moving parts underscore the need for a careful reassessment of the company’s risk-return balance. Whether considering a new position, maintaining current exposure or realizing gains, investors would benefit from a closer look at Ovintiv’s strategic priorities and its path for earnings growth.

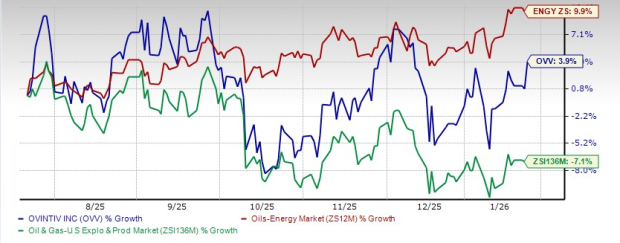

Over the past six months, Ovintivhas delivered a 3.9% gain in its share price, outperforming its sub-industry’s fall of 7.1%. However, it lagged behind the broader sector’s gain of 9.9%. A closer look at Ovintiv’s financial position, industry outlook and long-term prospects can help determine the most prudent course of action for the stock.

Meanwhile, the Zacks Consensus Estimate for Ovintiv’s 2025 earnings is pegged at $4.31 per share, indicating a 26.1% year-over-year decline. The consensus mark for its revenues is pegged at $8.7 billion for 2025, also implying a 5% year-over-year decline, indicating an unfavorable outlook.

The Zacks Consensus Estimate for Ovintiv’s 2025 earnings has been revised about 4% downward over the past 60 days. A downward revision suggests analysts have become more cautious about the company’s near-term outlook. Even a modest cut can dent confidence and create hesitation among investors considering new positions.

High Absolute Debt Level Still a Structural Risk: Although leverage ratios are reasonable, Ovintiv still carries over $5.2 billion in long-term debt, which remains substantial in absolute terms. In a prolonged commodity downturn, servicing this debt could constrain capital returns or force reductions in buybacks and dividends. The company’s leverage target assumes mid-cycle pricing, which may not hold in sustained low-price environments.

Asset Divestiture Uncertainty Around Anadarko Sale: The planned sale of Anadarko assets is central to Ovintiv’s debt reduction strategy, but timing, valuation and market conditions remain uncertain. A weaker buyer environment or lower-than-expected proceeds could delay deleveraging or reduce future capital return capacity. Until the transaction is completed, investors face uncertainty around portfolio composition and balance sheet outcomes.

Natural Gas Pricing Remains a Margin Headwind: Ovintiv continues to face margin pressure from weak natural gas pricing, which remains well below oil-equivalent economics and long-term mid-cycle expectations. Given the company’s meaningful exposure to gas-weighted assets in the Montney, its cash flow profile remains sensitive to broader North American gas market dynamics. If subdued pricing conditions persist, margins could remain compressed, limiting free cash flow generation and reducing capital allocation flexibility, even with risk management and hedging strategies in place.

Forward-Looking Guidance Carries Execution and Market Risk: Raised production guidance assumes continued operational execution, stable service costs and supportive commodity pricing. Any disruptions — such as cost inflation, regulatory changes or infrastructure constraints — could prevent Ovintiv from meeting targets. As with all E&P companies, forward guidance is inherently sensitive to external variables beyond management control, adding forecast risk for investors.

Capital Intensity Limits Downside Flexibility: Ovintiv’s upstream model requires over $2.1 billion annually in capital investment to sustain production and growth. While efficient, this capital intensity reduces flexibility during downturns when cutting spending too aggressively could impair future volumes. Investors seeking low-maintenance cash-flow assets may view Ovintiv’s reinvestment requirements as a structural disadvantage versus royalty or infrastructure businesses.

Ovintiv’s consensus estimates point to declining earnings and revenues in 2025, with recent downward estimate revisions dampening investor confidence. High absolute debt, uncertainty around the Anadarko asset sale, persistent natural gas price pressure and capital-intensive operations limit financial flexibility. With guidance sensitive to volatile commodity markets and execution risks, investors may prefer reallocating capital to energy names with clearer growth visibility and stronger balance sheets. Ovintiv’s near-term risk profile outweighs its upside, making a suitable case for selling the stock.

Currently, OVV has a Zacks Rank #4 (Sell).

Investors interested in the energy sector may consider some top-ranked stocks like Cenovus Energy Inc. CVE, Oceaneering International, Inc. OII and TechnipFMC plc FTI. While Cenovus Energy and Oceaneering International currently sport a Zacks Rank #1 (Strong Buy) each, TechnipFMC carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Calgary, Canada-based Cenovus Energy is a leading integrated energy firm. The company’s operations comprise marketing the produced oil, natural gas and natural gas liquids. The Zacks Consensus Estimate for CVE’s 2025 earnings indicates 26.2% year-over-year growth.

Houston, TX-based Oceaneering International is one of the leading suppliers of offshore equipment and technology solutions to the energy industry. The Zacks Consensus Estimate for OII’s 2025 earnings indicates 76.3% year-over-year growth.

Newcastle & Houston-based TechnipFMC is a leading manufacturer and supplier of products, services and fully integrated technology solutions for the energy industry. The Zacks Consensus Estimate for FTI’s 2025 earnings indicates 24.7% year-over-year growth.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-03 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-28 | |

| Jul-24 | |

| Jul-24 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite