|

|

|

|

|||||

|

|

|

Starbucks Corporation SBUX is scheduled to release first-quarter fiscal 2026 results on Jan. 28.

The Zacks Consensus Estimate for SBUX’s first-quarter fiscal 2026 earnings per share (EPS) is pegged at 58 cents, indicating 15.9% decline from 69 cents reported in the prior-year quarter. The consensus mark for earnings has witnessed downward revisions in the past 60 days.

SBUX earnings have missed the Zacks Consensus Estimate in the trailing three out of four quarters and beat on the remaining occasion, with an average miss of 10.1%.

The consensus mark for first-quarter fiscal 2026 revenues is pegged at $9.65 billion, indicating a 2.7% increase from the year-ago quarter’s reported figure.

Our proven model does not predict an earnings beat for Starbucks this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat, which is not the case here.

SBUX’s Earnings ESP: Starbucks has an Earnings ESP of -2.01%. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Starbucks Zacks Rank: The company carries a Zacks Rank #4 (Sell) at present.

You can see the complete list of today’s Zacks #1 Rank stocks here.

The company’s revenues in first-quarter fiscal 2026 are likely to have been aided by a tangible improvement in customer traffic as its operational reset gained traction. During the last quarter conference call, management highlighted that U.S. company-operated comparable sales turned positive in September and stayed positive into October, signaling momentum entering the fiscal first quarter. This recovery was largely transaction-led rather than price-driven, reflecting improved service execution, better order sequencing and more consistent staffing during peak hours. As service times shortened and reliability improved across café, drive-thru and mobile channels, Starbucks was able to recapture visits across dayparts, particularly in the morning, which historically anchors its revenue base.

Menu innovation and brand re-engagement are also likely to have supported top-line growth. The fall launch, including the introduction of protein-based beverages and cold foam options, is expected to have helped attract less-frequent customers while encouraging customization across a broad range of drinks. These offerings resonated with health and value-conscious consumers and were positioned as incremental rather than promotional, allowing Starbucks to drive revenue without heavy discounting.

International operations are likely to have further bolstered consolidated revenue growth in the quarter. Starbucks entered fiscal 2026 with strong momentum across several key markets, including China, Japan, the United Kingdom and Mexico, all of which delivered positive comparable sales exiting fourth-quarter fiscal 2025. China benefited from transaction growth and expanding delivery adoption, while disciplined unit expansion added incremental sales. Combined with robust performance in Channel Development, driven by ready-to-drink and global coffee partnerships, these factors provided geographic and channel diversification that supported overall revenue growth in first-quarter fiscal 2026.

Despite improving revenues, earnings in the first quarter of fiscal 2026 were pressured by elevated cost structures tied to Starbucks’ turnaround investments and external inflation. Labor expenses rose as the company fully annualized incremental staffing and hours under the Green Apron Service model, while assistant store manager roles began scaling. At the same time, commodity headwinds, particularly persistently high coffee prices and tariff impacts, are likely to have weighed on margins. Management was clear that these costs would precede earnings recovery, reinforcing that fiscal 2026 would remain a transition year in which profitability lagged top-line improvement.

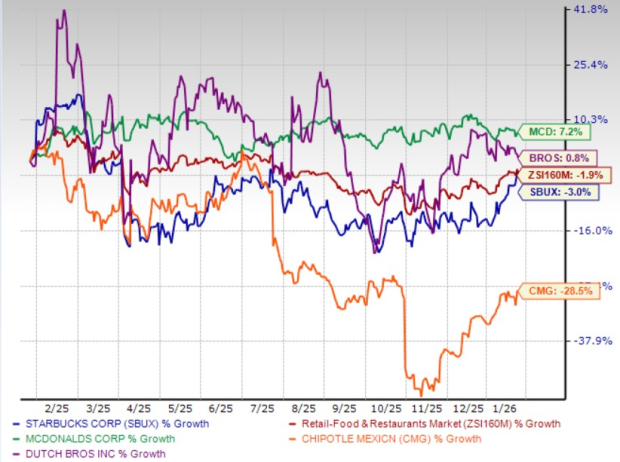

Shares of Starbucks have lost 3% in the past year compared with the industry’s decline of 1.9%. In the same time frame, other industry players like McDonald's Corporation MCD, Dutch Bros Inc. BROS and Chipotle Mexican Grill, Inc. CMG have gained 7.2%, 0.8% and down 28.5%, respectively.

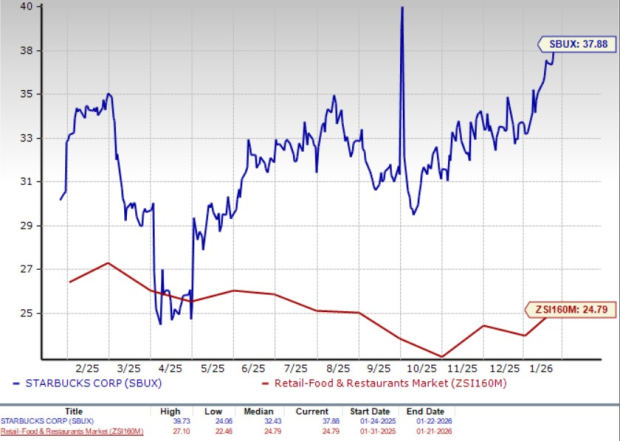

From a valuation standpoint, SBUX trades at a forward price-to-earnings (P/E) multiple of 37.88, above the industry’s average of 24.79. Conversely, industry players, such as McDonald's, Dutch Bros and Chipotle, have P/E multiples of 22.9, 67.79 and 33.5, respectively.

Investors may want to stay on the sidelines ahead of Starbucks’ first-quarter earnings release as the near-term risk-reward remains skewed to the downside. While customer traffic and revenues appear to be stabilizing, earnings momentum is still weak, with profitability pressured by elevated labor costs, ongoing turnaround investments and commodity inflation that management has already signaled will weigh on results before any meaningful recovery.

The stock’s recent earnings history also raises caution, as Starbucks has struggled to consistently meet expectations, which increases the risk of volatility around the print. Adding to this, the shares trade at a premium valuation relative to most peers despite underperforming the broader restaurant group, leaving little margin for error. Until there is clearer evidence that revenue improvements are translating into sustained margin expansion, avoiding the stock ahead of earnings may be the more prudent approach.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 13 min | |

| 1 hour | |

| Apr-29 | |

| Apr-29 | |

| Apr-29 | |

| Apr-29 | |

| Apr-29 | |

| Apr-29 | |

| Apr-29 | |

| Apr-29 | |

| Apr-29 | |

| Apr-29 | |

| Apr-29 | |

| Apr-29 | |

| Apr-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite