|

|

|

|

|||||

|

|

|

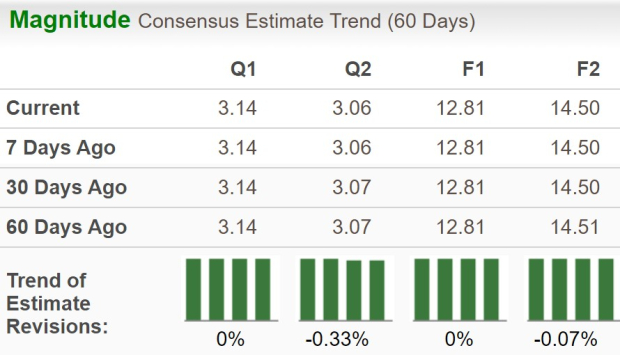

Visa Inc. V is set to report its first-quarter fiscal 2026 results on Jan. 29, 2026, after market close. The Zacks Consensus Estimate for the to-be-reported quarter’s earnings is currently pegged at $3.14 per share on revenues of $10.68 billion.

The estimate for fiscal first-quarter earnings has remained stable over the past 60 days. The bottom-line projection indicates a year-over-year increase of 14.2%. The Zacks Consensus Estimate for quarterly revenues suggests year-over-year growth of 12.3%.

For fiscal 2026, the Zacks Consensus Estimate for Visa’s revenues is pegged at $44.44 billion, implying a rise of 11.1% year over year. The consensus mark for EPS is pegged at $12.81, suggesting a jump of around 11.7% on a year-over-year basis.

The payments juggernaut has a robust history of surpassing earnings estimates. It beat estimates in each of the last four quarters, with the average being 2.7%. This is depicted in the graph below:

Visa Inc. price-eps-surprise | Visa Inc. Quote

However, our proven model does not conclusively predict an earnings beat for the company this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy), or 3 (Hold) increases the odds of an earnings beat, but that is not the case here.

Visa has an Earnings ESP of -0.23% and a Zacks Rank #3. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate suggests a 6.4% increase in total Gross Dollar Volume from the previous year, while our model predicts 6.2% growth. The growing adoption and popularity of digital payment methods are likely to contribute positively to Visa's overall fiscal first-quarter results.

As the company draws revenues as a set percentage of total transaction value every time a customer makes payments with a debit/credit card, higher spending means more revenues in the form of transaction processing fees. The Zacks Consensus Estimate for fiscal first-quarter total processed transactions indicates 9.5% year-over-year growth.

The consensus mark for total payment volumes indicates an 8.6% year-over-year increase. We expect the metric for U.S. operations alone to jump 6.7% year over year. Similarly, our model predicts 10% year-over-year growth in Latin America and 15% in CEMEA.

The Zacks Consensus Estimate for data processing revenues indicates 14.6% growth in the fiscal first quarter from the year-ago level of $4.7 billion, while our estimate suggests a 14.9% increase. Similarly, the consensus mark for service revenues suggests 11.2% year-over-year growth, whereas we expect the metric to grow by 9.2% from $4.2 billion.

Furthermore, the consensus estimate for international transaction revenues indicates 11.8% growth from a year ago, whereas our model predicts a 10.8% increase. Continuous growth in cross-border volumes is expected to have supported the metric.

The factors stated above are expected to have positioned Visa for strong year-over-year growth in the fiscal first quarter. However, rising expenses and client incentives (a contra-revenue item) are likely to have partially offset the positive impact of higher volumes.

We expect adjusted total operating expenses for the quarter under review to increase 12% year over year due to increased Personnel, Professional Fees and Network and Processing expenses. Also, the Zacks Consensus Estimate for client incentives is pegged at $4.4 billion for the to-be-reported quarter.

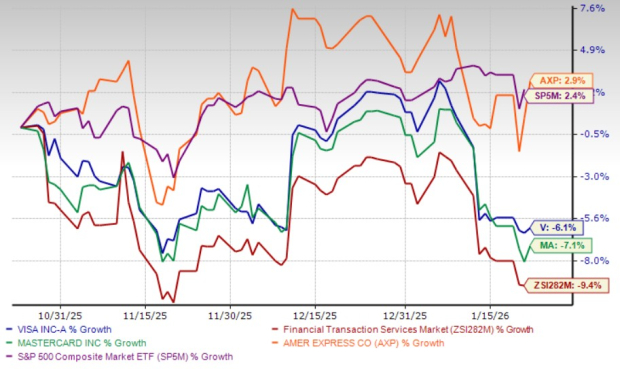

Visa's stock has declined 6.1% in the past three months. It shed less value than the industry’s 9.4% fall butunderperformed the S&P 500’s rise of 2.4%. In comparison, its peers like Mastercard Incorporated MA and American Express Company AXP have decreased 7.1% and gained 2.9%, respectively, during this time.

Now, let’s look at the value Visa offers investors at current levels.

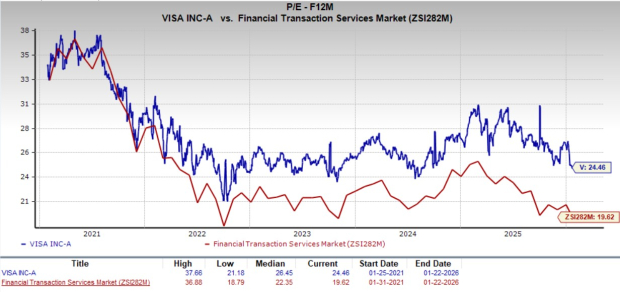

The company’s valuation looks somewhat stretched compared with the industry average. Currently, Visa is trading at 24.46X forward 12-month earnings, above the industry’s average of 19.62X.

In comparison, Mastercard is even less attractively valued, trading at 27.71X forward 12-month earnings. American Express, on the other hand, is trading at 20.80X, offering a better value at the moment.

Visa remains a high-quality compounder, backed by its asset-light model, resilient transaction volumes, expanding value-added services, and long-term relevance in global payments. Structural tailwinds, from cross-border recovery, stablecoin enablement and emerging AI-led commerce, support its long-term growth outlook.

However, near-term risks are rising. Expense growth and higher client incentives are pressuring margins, regulatory scrutiny is intensifying across key markets and competitive threats from potential large-merchant stablecoins could weigh on transaction economics. Despite a recent pullback, Visa’s valuation remains elevated versus the industry, limiting near-term upside.

Given these factors, Visa looks fundamentally strong but not compellingly priced. Investors may be better served waiting on the sidelines for a more attractive entry point, either through further price correction or clearer visibility on cost and regulatory pressures.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Why investors should be 'really excited' about this form of agentic AI trading

V

Yahoo Finance Video

|

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite