|

|

|

|

|||||

|

|

|

Nebius Group N.V. NBIS and Amazon.com, Inc. AMZN offer different investment profiles within the AI cloud space. NBIS is a focused, high-growth AI cloud provider that gives investors direct exposure to rising demand for AI infrastructure, but its smaller scale and early-stage nature make it a higher-risk proposition. Amazon, led by Amazon Web Services (“AWS”), brings scale, diversification and consistent cash generation, with AI deeply embedded across its cloud, retail and semiconductor strategies. While Amazon appeals to investors seeking stability and long-term compounding, NBIS may attract those willing to accept greater volatility in exchange for potentially higher growth.

According to an IDC report, spending on AI infrastructure is expected to top $758 billion by 2029. This uptrend in spending benefits both Amazon and Nebius, but not equally. They differ sharply in scale and growth trajectory. So, for investors looking to make a smart move in the AI infrastructure space, which stock truly stands out?

Let’s analyze their fundamentals, growth opportunities, market challenges and valuation to assess which one presents a stronger investment opportunity.

Nebius operates in a supply-constrained AI infrastructure market where demand for GPU capacity far exceeds available power and data-center readiness. To capitalize on this imbalance, the company is rapidly scaling its footprint, lifting its contracted power target to 2.5 gigawatts by 2026 from 1 gigawatt earlier, with 800 megawatts to 1 gigawatt of fully connected capacity expected to be operational by the end of 2026.

The company is gaining traction with AI-native customers such as Cursor and Black Forest Labs, while securing large, long-term commitments from hyperscalers. Multi-billion-dollar agreements with Microsoft, valued between $17.4 billion and $19.4 billion, and with Meta, of up to $3 billion, highlight strong confidence in Nebius’ platform, with revenue contributions beginning in the fourth quarter of 2025, with the bulk of revenue estimated through 2026.

Nebius remains focused on building and scaling its core AI cloud business. The company is deepening its enterprise offerings with the launch of the Aether 3.0 cloud platform and the Nebius Token Factory, an inference solution built to run open-source models at scale. In December 2025, Nebius announced the launch of Nebius AI Cloud 3.1, the latest version of its full-stack AI cloud platform designed to address these needs. Recently, Nebius announced the deployment of the NVIDIA Rubin platform across Nebius AI Cloud and Token Factory, which will start in the second half of 2026.

Nebius Group N.V. price-consensus-eps-surprise-chart | Nebius Group N.V. Quote

Apart from these, the company is investing aggressively in expanding its global data center footprint, with a strong focus on securing power capacity well ahead of deployment. Nebius plans to further expand its existing data centers in the U.K., Israel and New Jersey in 2026, while bringing new facilities online across the United States and Europe in the first half. Nebius is also securing multiple large-scale sites, each capable of delivering hundreds of megawatts, with several expected to become operational before the end of 2026. The company is targeting $7–$9 billion in ARR by 2026.

However, the company continues to navigate macroeconomic uncertainty alongside rising operating expenses and heavy capital spending. Nebius raised its capital expenditure outlook from roughly $2 billion to about $5 billion for 2025. Such elevated capex levels increase risk if revenue growth does not keep pace with the company’s capital-intensive strategy, especially as AI demand could fluctuate amid competitive pricing pressures and evolving regulatory conditions. Moreover, scaling aggressively (multiple data centers in various regions) involves execution risk.

Amazon continues to lead the global e-commerce and cloud computing landscape, leveraging its scale, innovation and customer-focused approach. Its retail operations are expanding rapidly, with same-day delivery of groceries and essentials. Innovations like the AI-powered shopping assistant Rufus, Amazon Lens and generative AI tools are enhancing the shopping experience, increasing purchase likelihood and driving incremental sales. Meanwhile, Amazon Ads is delivering strong growth, with its full-funnel advertising capabilities, demand-side platform (DSP) and strategic partnerships with Netflix, Spotify and SiriusXM, enabling advertisers to reach large, engaged audiences effectively.

AWS remains a cornerstone of the company, driving growth and innovation in cloud computing and AI. AWS offers the broadest infrastructure and service capabilities, making it a preferred platform for enterprises and governments to run core workloads. Its AI-focused offerings, such as SageMaker, Bedrock, Strands and AgentCore, simplify the building and deployment of AI models and agents at scale. These platforms help companies create secure, scalable and efficient AI solutions, with examples including enterprise applications in coding, business insights and customer service.

Significant investments in AWS infrastructure, including custom Trainium chips and Project Rainier AI clusters, position Amazon to meet increasing demand for AI workloads. Trainium2 adoption is fully subscribed, and Trainium3 is expected to expand capacity and support a broader customer base. Amazon’s focus on high-performing, cost-efficient infrastructure reinforces its leadership in cloud-based AI.

Amazon's substantial investments in AI infrastructure and talent development create formidable competitive barriers while unlocking innovative capabilities that drive customer engagement, operational excellence and margin improvement across all business segments. However, substantial capital expenditure requirements for AI infrastructure and data centers strain financial resources and compress margins. The company's expanding debt burden reduces financial flexibility amid rising interest rates.

Over the past month, NBIS shares have gained 6.3% while AMZN stock has jumped 2.8%.

Valuation-wise, Nebius is overvalued while Amazon is undervalued, as suggested by the Value Score of F and B, respectively.

In terms of Price/Book, NBIS shares are trading at 4.79X, lower than AMZN’s 6.9X.

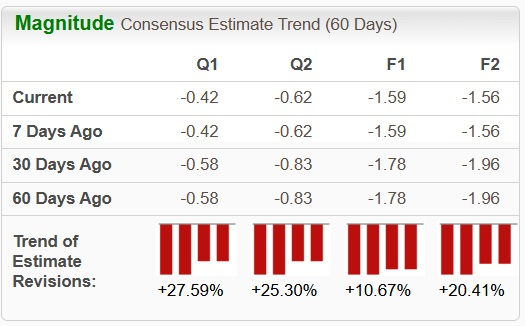

Analysts have significantly revised their earnings estimates upward for NBIS’ bottom line for the current year.

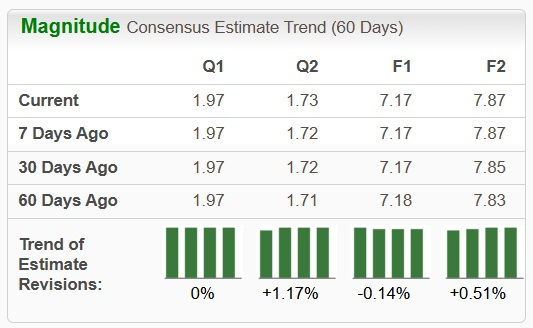

For AMZN, there is a marginal downward revision for the current year.

NBIS carries a Zacks Rank #3 (Hold) at present, while AMZN has a Zacks Rank #2 (Buy). Consequently, in terms of Zacks Rank and valuation, AMZN seems to be a better pick at the moment.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 1 hour | |

| 2 hours | |

| 2 hours | |

| 2 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 4 hours | |

| 5 hours | |

| 10 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite