|

|

|

|

|||||

|

|

|

lululemon athletica inc. LULU has been witnessing a downtrend in the past year, driven by the soft U.S. demand and margin pressures from promotions and higher costs. While international markets offer support, this is not enough to offset North American weakness, prompting investors to reassess near-term visibility despite the brand’s intact long-term positioning.

LULU’s current forward 12-month price-to-earnings (P/E) multiple of 15.1X reflects a discount relative to the Zacks Textile – Apparel industry’s average of 16.28X, making the stock cheap from a valuation perspective. lululemon’s price-to-sales (P/S) ratio of 1.95X is also below the industry’s 2.35X, adding to investor expectations.

At 15.1X P/E, lululemon is trading at a valuation much lower than its competitors. Its competitors, such as Ralph Lauren Corporation RL, Under Armour, Inc. UAA and NIKE Inc. NKE, are trading at higher multiples. Ralph Lauren, Under Armour and NIKE have forward 12-month P/E ratios of 21.53X, 37.05X and 30.96X — all significantly higher than lululemon.

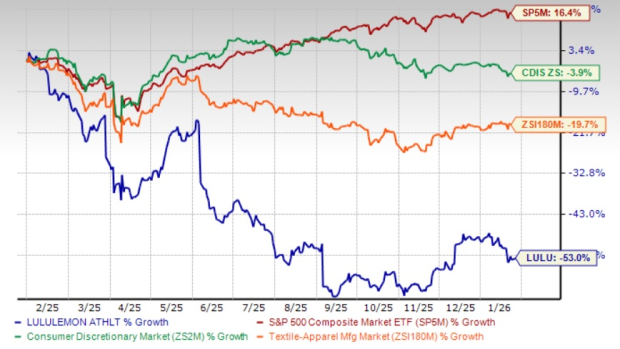

In the past year, LULU shares have lost 53% compared with the broader industry’s decline of 19.7%. The company has also underperformed the Zacks Consumer Discretionary sector’s decline of 3.9% and the S&P 500’s rise of 16.4%.

lululemon’s performance is significantly weaker than Ralph Lauren’s growth of 39.9% in the past year. The LULU stock has also underperformed Under Armour and NIKE, which have declined 22% and 12.5%, respectively, in the past year.

lululemon’s current share price of $192.79 is 54.5% below its recent 52-week high mark of $423.32. Also, the stock trades 21.1% above its 52-week low of $159.25. LULU trades below its 50 and 200-day moving averages, indicating a bearish sentiment.

lululemon’s recent stock decline reflects a fundamental reset in growth and earnings expectations, rather than any deterioration in brand strength or long-term positioning. The company’s recent earnings point to continued softness in the core Americas business, where traffic and conversion have weakened as consumers become more selective in discretionary spending. Management indicated that demand trends became more cautious as the third quarter of fiscal 2025 progressed, reinforcing concerns that the U.S. slowdown may persist longer than previously anticipated.

Profitability pressures have further weighed on sentiment. The company is operating in a more promotional environment, while also absorbing higher product and supply-chain costs. Management has chosen to prioritize inventory discipline and brand health over near-term margin defense, a prudent strategic move but one that clouds short-term earnings visibility. Reduced operating leverage has compounded this effect, limiting lululemon’s ability to offset cost pressures through scale, a shift from its historically strong margin profile.

International markets, particularly China, continue to provide growth support, but the company highlighted moderating momentum due to tougher comparisons and calendar-related factors. Importantly, these regions are not yet large enough to fully counterbalance weakness in North America. Investor caution has also been amplified by leadership transition risks and management’s acknowledgment that a meaningful inflection in the U.S. business may take time.

The Zacks Consensus Estimate for lululemon’s fiscal 2025 EPS has increased 0.2% in the past seven days. The upward revision in earnings estimates indicates that analysts are optimistic about the company’s near-term growth potential. Meanwhile, the EPS estimate for fiscal 2026 declined 0.5% in the past seven days.

For fiscal 2025, the Zacks Consensus Estimate for LULU’s revenues implies 4.6% year-over-year growth, while the EPS estimate suggests a 10.8% decline. The consensus mark for fiscal 2026 revenues indicates 4.7% year-over-year growth, while the earnings estimate suggests a 2.3% decline.

lululemon’s upward trend in fiscal 2025 estimates is driven by improving near-term visibility and growing confidence in the company’s execution, following a stronger-than-expected finish to the holiday season. Management’s recent update pointed to robust holiday demand and results are expected to track toward the high end of the prior guidance, which has helped ease concerns around demand stability, particularly after a challenging year, marked by softer U.S. trends and elevated competition.

The solid holiday performance underscored the resilience of lululemon’s core customer base and the company’s ability to perform in a highly promotional retail environment. This has reinforced expectations that recent demand pressures may be stabilizing rather than worsening. Additionally, management’s decision to hold assumptions for the gross margin, operating expenses and tax rates steady suggests cost discipline and reduced earnings volatility.

Another key driver behind rising estimates is the company’s strong international momentum, which continues to offset weakness in North America. Rapid expansion outside the U.S. is improving lululemon’s growth mix and extending its long-term runway. Together, improved holiday execution, stable margins and accelerating international demand have prompted analysts to raise the fiscal 2025 earnings expectations, reflecting renewed confidence in lululemon’s earnings power and recovery trajectory.

lululemon’s recent stock weakness reflects ongoing pressure from softer U.S. demand, margin headwinds and limited visibility, all of which have weighed on investor sentiment. This underperformance has pushed the stock to a discounted valuation versus peers, partially pricing in these challenges.

However, recent signals have turned more constructive. Strong holiday-season execution, results tracking toward the high-end of guidance and an improving near-term estimate trend point to stabilizing demand and better operational control. International markets continue to support growth, helping offset North American softness. While uncertainties around a sustained U.S. recovery and margin normalization remain, the combination of depressed valuation and improving near-term indicators supports a neutral stance, balancing recovery potential against lingering execution risks. The stock currently has a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 8 hours | |

| 9 hours | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite