|

|

|

|

|||||

|

|

|

Altria Group, Inc. MO is slated to report its fourth-quarter 2025 earnings on Jan. 29, before market open.

The Zacks Consensus Estimate for fourth-quarter revenues stands at $5 billion, indicating a 2% decline from the same period last year. Meanwhile, the consensus mark for earnings has remained the same in the past 30 days at $1.31 per share, indicating 1.6% growth from the year-ago quarter’s reported figure.

Altria has a trailing four-quarter average earnings surprise of 3.1%. In the last reported quarter, the company’s bottom line surpassed the Zacks Consensus Estimate by a margin of 0.7%.

Altria Group, Inc. price-consensus-eps-surprise-chart | Altria Group, Inc. Quote

As investors prepare for Altria’s fourth-quarter announcement, the question looms regarding earnings beat or miss. Our proven model predicts an earnings beat for MO this time. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat, which is exactly the case here. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Altria has an Earnings ESP of +1.54% and a Zacks Rank #3 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

Altria’s fourth-quarter performance is likely to have been shaped by disciplined pricing and effective cost control. While domestic cigarette shipment volumes have been under pressure as inflation-weary consumers traded down, favorable pricing and product mix appear to have helped offset volume declines, supporting earnings stability during the period.

Despite ongoing volume headwinds, Altria appears to have delivered steady profitability, helped by solid revenue management and disciplined cost control. Pricing gains across core smokeable brands seem to have cushioned operating income as shipment volumes softened. This ability to hold margins in a tightly regulated category highlights the company’s defensive characteristics and supports its case as a reliable, cash-generative investment.

A key contributor to Altria’s earnings mix remains its oral tobacco business, supported by the favorable margin profile of smokeless products. Continued consumer adoption of nicotine pouches appears to have aided segment profitability despite competitive intensity. The higher-margin nature of these offerings, combined with disciplined pricing, is likely to have enhanced the company’s performance in the quarter under review.

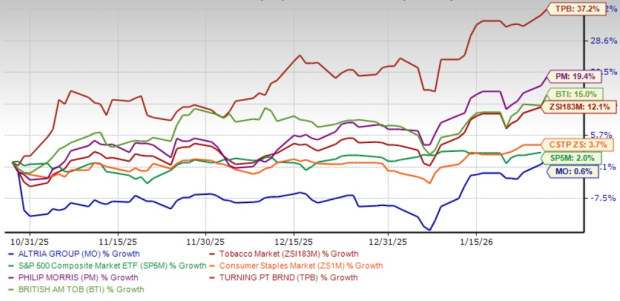

Over the past three months, Altria stock has posted a modest gain of 0.6%, significantly lagging the Zacks Tobacco industry’s strong 12.1% advance and the Zacks Consumer Staples sector’s 3.7% growth, though it slightly underperformed the S&P 500, which rose 2% over the same period. Within its peer group, Altria trailed most competitors. Philip Morris International Inc. PM delivered a solid 19.4% increase, British American Tobacco p.l.c. BTI gained 15% and Turning Point Brands, Inc. TPB emerged as the clear outperformer with a robust 37.2% rally during the period.

From a valuation perspective, Altria’s shares are trading at a discount relative to the industry average. With a forward 12-month price-to-earnings ratio of 11.39, below the industry’s average of 15.48, the stock offers compelling value for investors seeking exposure to the sector.

This valuation gap becomes even more pronounced compared with key competitors. Philip Morris, Turning Point Brands and British American Tobacco trade at a P/E ratio of 21.25, 29.87 and 12.5, respectively, significantly higher than Altria’s multiple.

Altria continues to demonstrate resilience through disciplined pricing strategies and effective cost management, which have helped offset volume pressures in its core cigarette business. The company’s expanding smoke-free portfolio, particularly nicotine pouches, remains an important driver of margin support and earnings stability. Additionally, Altria’s discounted valuation and strong, consistent cash flows enhance its appeal as a defensive consumer staples stock. With stable earnings prospects, investors may consider holding their positions while monitoring progress in smoke-free innovation and overall profitability.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-17 | |

| Jul-16 | |

| Jul-16 | |

| Jul-15 | |

| Jul-14 | |

| Jul-10 | |

| Jul-09 | |

| Jul-03 | |

| Jul-03 | |

| Jul-02 | |

| Jun-30 | |

| Jun-30 | |

| Jun-30 | |

| Jun-30 | |

| Jun-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite