|

|

|

|

|||||

|

|

|

Both SoFi Technologies SOFI and OppFi Inc. OPFI operate within the fintech lending space.

While SOFI is a one-stop shop digital financial services platform, it serves prime and near-prime borrowers. OppFi specializes in tech-fueled consumer credit solutions, targeting subprime borrowers.

We have analyzed both fintech credit stocks to determine which offers the greater upside.

Innovation continues to underpin SoFi’s competitive positioning. The introduction of SoFi Pay, which enables fast and low-cost international payments through blockchain technology, marks a meaningful expansion into global financial connectivity. Complementing this move, the launch of the SoFi USD stablecoin highlights the company’s intent to integrate blockchain solutions into mainstream financial services.

SoFi has also relaunched its crypto trading platform, allowing users to buy, sell and hold digital assets directly within the app, an offering aligned with renewed investor interest in cryptocurrencies. At the same time, the rollout of SoFi Coach, an AI-powered evolution of its Cash Coach tool, aims to deliver personalized financial insights across customer accounts, strengthening SoFi’s value proposition as a holistic financial platform.

Further enhancing customer engagement, SoFi introduced the SoFi Smart Card, offering cash-back rewards on food purchases alongside credit-building tools and access to competitive borrowing and deposit rates. Collectively, these initiatives deepen ecosystem stickiness, expand wallet share and reinforce brand loyalty.

Marketing partnerships are also supporting growth. The collaboration with NFL MVP Josh Allen to promote SoFi Plus, the company’s premium subscription offering, underscores SoFi’s growing brand visibility and appeal among younger, digitally native consumers.

Since acquiring Galileo Financial Technologies in 2020, SoFi has significantly strengthened its fintech infrastructure. Galileo now powers critical components of SoFi’s ecosystem, including payment processing, buy-now-pay-later capabilities and an AI-driven engagement tool, forming the technological backbone behind SoFi’s seamless user experience.

Operating under a single corporate umbrella allows for deep integration between SoFi’s consumer-facing products and Galileo’s technology stack. This structure eliminates the constraints of third-party dependencies, improving speed to market, operational efficiency, and innovation across digital banking, lending and personal finance.

The relationship also creates a reinforcing feedback loop. While Galileo enables SoFi’s product expansion, it simultaneously benefits from SoFi’s scale and data insights, allowing Galileo to enhance its offerings for external clients. Over time, this acquisition has evolved into a structural advantage, positioning SoFi as a more vertically integrated fintech platform with tighter control over both customer experience and core technology.

OppFi’s recent financial performance highlights how technology-led underwriting is reshaping its operating model. The company’s proprietary AI- and machine-learning-driven underwriting engine, Model 6, has emerged as the primary catalyst behind its record profitability, enabling OppFi to scale earnings far faster than revenues.

In the third quarter of 2025, OppFi delivered 136.9% year-over-year growth in net income, despite revenues increasing at a more modest 13.5%. This widening gap between top-line growth and profitability underscores meaningful gains in operational efficiency. A central driver has been the company’s 79.1% auto-approval rate, up 230 basis points year over year, which materially reduced reliance on manual underwriting. As human intervention declined, total expenses rose just 0.1% year over year, resulting in sharp margin expansion and adjusted EPS growth of nearly 79%.

Further strengthening this efficiency story is OppFi’s ongoing refinement of its credit assessment framework. The Model 6.1 refit represents an incremental but important upgrade aimed at improving risk pricing precision. Early results have been encouraging, with net charge-offs declining 11.2% as a percentage of revenues and 9.5% as a percentage of average receivables for the nine months ended Sept. 30, 2025. These improvements suggest that higher automation is not coming at the expense of credit quality, an especially critical factor given OppFi’s focus on higher-risk borrower segments.

Looking ahead, management views the Loan Origination Lending Application (LOLA) as the next leg of scalability. Designed as a clean, AI-ready architecture, LOLA is intended to support originations, servicing and corporate operations as AI tools evolve. Testing is underway in the fourth quarter of 2025, with a planned migration in early 2026. Early indicators, including rising automated approvals, suggest LOLA could further separate revenue growth from operating costs.

That said, execution risk remains. A full platform migration requires careful oversight to avoid disruptions. Still, management’s confidence in delivering double-digit revenue and adjusted net income growth in 2026 reflects the belief that the combined impact of Model 6.1 and LOLA can sustain high margins across credit cycles.

Overall, OppFi’s ability to pair disciplined credit assessment with rising automation positions the company to maintain strong profitability while scaling loan volumes, an increasingly valuable advantage in a volatile lending environment.

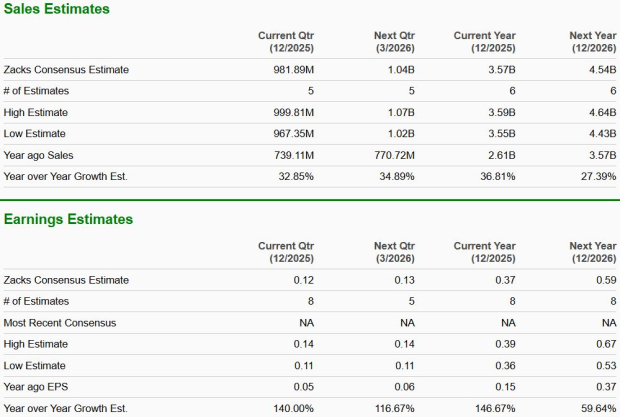

The Zacks Consensus Estimate for SOFI’s 2025 sales and EPS indicates year-over-year growth of 36.8% and 146.7%, respectively. EPS estimates have been trending upward over the past 60 days.

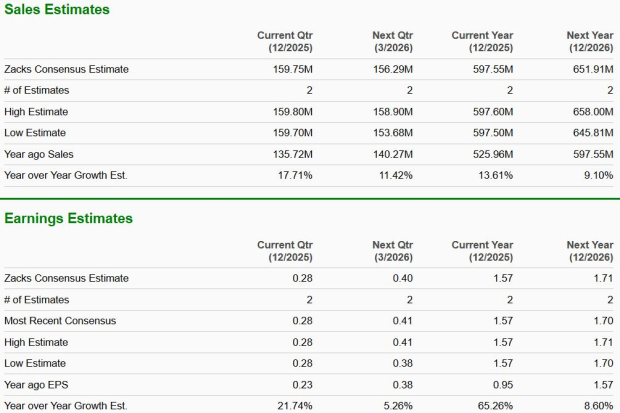

The Zacks Consensus Estimate for OPFI’s 2025 sales and EPS indicates year-over-year rallies of 13.6% and 65.3%, respectively. There have been no estimations lately.

OPFI is currently trading at a forward 12-month P/E ratio of 5.78X, which is lower than the 12-month median of 7.84X. SOFI is trading at 41.91X, which is below the 12-month median of 47.26X. While both stocks are trading at a discount compared with their historical valuations, OPFI appears way cheaper than SOFI.

Between the two fintech lenders, SoFi emerges as the more compelling stock right now, even though both carry a Hold outlook. SoFi’s advantage lies in its diversified, platform-driven model, which reduces reliance on any single lending segment and supports more balanced growth across cycles. Its expanding ecosystem, deep technology integration, and growing engagement tools position it well for long-term scale and resilience. OppFi’s efficiency gains are impressive, but its business remains more tightly linked to subprime credit conditions, which can amplify risk during periods of stress. For investors prioritizing durability, product breadth, and strategic optionality, SoFi offers the stronger overall setup at current levels.

Both SOFI and OPFI have a Zacks Rank #3 (Hold) at present. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 7 hours | |

| 17 hours | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 | |

| Aug-02 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite