|

|

|

|

|||||

|

|

|

Walmart Inc. WMT and Target Corporation TGT are two of the most influential names in U.S. big-box retail, each leveraging a large store base and expanding omnichannel capabilities to capture consumer spending across income cohorts.

Walmart, the world’s largest retailer with a market capitalization of about $929.4 billion, continues to lean on its everyday low-price model, scale advantages and diversified profit streams spanning e-commerce, advertising and membership income. Target, with a market cap of roughly $46.2 billion, remains a predominantly U.S.-focused retailer known for its design-led assortment and private-label strength.

This face-off is especially timely as both retailers navigate a cautious consumer environment marked by value-seeking behavior and discretionary spending pressure. While Walmart continues to see steady customer traffic and strong digital growth, Target is still in the middle of a multi-quarter turnaround focused on improving its product mix, shopping experience and operations.

Walmart’s business model is built on steady execution and continued investment across its operations. The company’s everyday low-price strategy continues to appeal to value-focused consumers, especially as discretionary spending remains selective. This positioning has supported consistent traffic and helped Walmart gain share in both grocery and general merchandise.

E-commerce remains a key growth driver. Walmart continues to expand faster delivery options, including same-day and next-day fulfillment, improving convenience and customer engagement. These efforts are closely tied to Walmart’s large store network, allowing the company to use its physical footprint to strengthen its omnichannel platform. Walmart is also increasing its use of artificial intelligence and generative AI tools across merchandising, search, customer service and fulfillment to improve personalization, demand planning and efficiency.

Higher-margin businesses are becoming more important to overall results. Walmart Connect continues to benefit from solid advertiser demand, while membership programs — led by Sam’s Club in the U.S. — support customer loyalty and provide more stable revenues. These strengths help offset near-term headwinds such as higher labor costs, shrink and a competitive pricing environment.

Walmart continues to invest in technology, automation and supply-chain improvements to drive long-term productivity. Strong cash generation allows the company to fund growth initiatives while maintaining a healthy balance sheet, reinforcing its position as a relatively defensive retailer. International operations and marketplace expansion add additional long-term upside. While results vary by market, Walmart remains focused on areas with clearer return potential. Growth in third-party sellers and digital services expands assortment and improves platform economics, supporting a constructive long-term outlook.

Target is executing a multi-year transformation centered on design-led merchandising, more curated assortments and trend-driven owned brands that reinforce its style-and-value positioning. Digital engagement remained healthy in the third quarter of fiscal 2025, supported by convenience-focused services such as same-day delivery and order pickup. Target Plus and Roundel continue to scale, contributing to marketplace expansion, retail media monetization and a gradually improving margin mix.

Technology-led initiatives remain an important area of focus. Target has been testing and expanding AI-enabled shopping and discovery tools designed to improve browsing, personalization and fulfillment flexibility. These efforts are aimed at enhancing convenience, improving demand forecasting and strengthening in-stock execution over time. Capital spending is expected to increase meaningfully in fiscal 2026 to support store remodels, larger formats and fulfillment upgrades, positioning the business for longer-term relevance.

Target is also leveraging advanced analytics to improve demand forecasting, assortment planning and speed to market. Internal tools, including data-driven trend identification and consumer testing capabilities, are helping the company identify emerging trends earlier and refine product decisions. Management noted improvements in on-shelf availability for key items during the fiscal third quarter, reflecting better inventory planning and execution.

Despite these operational efforts, demand recovery remains uneven as macroeconomic pressures continue to weigh on discretionary spending. Softer consumer behavior has affected store traffic and merchandise performance, with categories such as Home and Apparel remaining under pressure. This weakness has been more pronounced in higher-margin discretionary areas, limiting near-term operating leverage. On its third-quarter earnings call, Target guided for low-single-digit declines in both sales and comparable sales for the fiscal fourth quarter, reflecting a cautious near-term outlook.

The Zacks Consensus Estimate for Walmart’s current fiscal-year sales and earnings per share (EPS) implies year-over-year growth of 4.5% and 4.8%, respectively. The consensus estimate for EPS for the current fiscal year has remained unchanged over the past 30 days. The consensus mark for the next fiscal-year sales and EPS suggests 4.5% and 12.3% growth from the respective year-ago period figures. The consensus estimate for EPS has seen upward revisions in the past 30 days.

The Zacks Consensus Estimate for Target’s current fiscal-year sales and EPS implies year-over-year declines of 1.6% and 17.6%, respectively. However, the consensus mark for the next fiscal-year sales and EPS suggests a 2.3% and 5.9% increase year over year. The Zacks Consensus Estimate for Target’s EPS for the current fiscal year has moved up 1 cent, while the estimate for the next fiscal year has remained unchanged over the past 30 days.

Over the past year, shares of Walmart have rallied 17.9%, while Target has tumbled 27.6%. While WMT has easily outpaced the Zacks Retail – Wholesale sector’s return of 4.7%, TGT has underperformed the same.

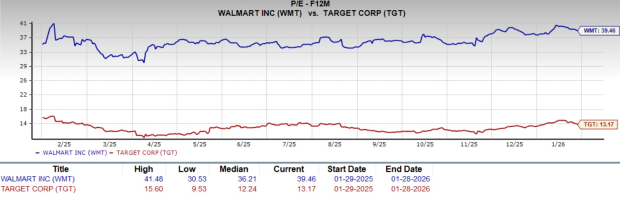

Walmart’s forward P/E of 39.46 is above its one-year median of 36.21, reflecting a valuation premium related to its scale, earnings visibility and defensive profile. Target trades at a forward P/E of 13.17, slightly above its one-year median of 12.24, suggesting modest expectations for stabilization, though its lower multiple still reflects ongoing concerns around discretionary demand and margin recovery.

At this stage of the retail cycle, Walmart is the better bet. Its value-led positioning, consistent execution and diversified growth engines provide greater visibility and resilience in a cautious consumer environment. Walmart is benefiting from steady traffic, strong omnichannel integration and incremental profit streams that help offset cost and competitive pressures. Target, while making progress on a strategic reset and investing to strengthen its long-term positioning, remains more exposed to discretionary spending volatility and is still working through a recovery phase. As a result, Walmart offers a more balanced risk-reward profile in the near to medium term, while Target may appeal more to investors willing to wait for a clearer and sustained turnaround.

Walmart currently holds a Zacks Rank #2 (Buy), whereas Target carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-09 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite