|

|

|

|

|||||

|

|

|

Is NVIDIA Corporation’s NVDA current sky-high valuation, amid trade risks and fierce competition, a reason for caution? Or, does its strong growth potential make it a worthy investment? Let’s see in detail –

NVIDIA is currently trading at a forward price-to-earnings (P/E) ratio of 41.07, well above the Semiconductor - General industry’s average of 28.99. This stretched valuation makes the NVDA stock volatile if growth expectations are not met.

Image Source: Zacks Investment Research

A potential U.S.-China trade war could hurt NVIDIA’s chip sales, a concern compounded by stiff competition from Intel Corporation INTC and Advanced Micro Devices, Inc. AMD, especially as data center capital spending accelerates.

Despite these concerns, the market appears unfazed, as indicated by NVIDIA’s elevated P/E ratio, which implies confidence in the company’s future growth and positions it as comparatively less risky within the volatile cyclical chip industry.

Let’s acknowledge that the U.S.-China trade complications are currently easing. China has authorized the purchase of NVIDIA’s H200 AI chips for several of NVIDIA’s Chinese customers for the first time. Some of the major tech players, including ByteDance and Alibaba Group Holding Limited BABA, have received initial approvals worth around $10 billion. With the Trump administration already authorizing the shipment of H200 chips to China, NVIDIA’s sales are expected to receive a significant boost.

NVIDIA also expects data center capital spending globally to reach between $3 trillion and $4 trillion annually by 2030, presenting significant opportunities for the company to sell its computing hardware and drive sales. Additionally, the strong demand for NVIDIA’s next-generation Blackwell chips and cloud graphics processing units (GPUs) is likely to further drive the company’s future revenues.

NVIDIA expects fiscal fourth quarter 2026 revenues to reach nearly $65 billion, with a plus or minus 2%, according to investor.nvidia.com. For the fiscal third quarter of 2026, NVIDIA has already reported revenues of $57 billion, up 62% year over year and 22% quarter over quarter.

NVIDIA’s strong growth outlook, driven by easing U.S.-China trade tensions, increasing data center spending, and booming demand for its chips, justifies its high valuation, keeping it an attractive investment.

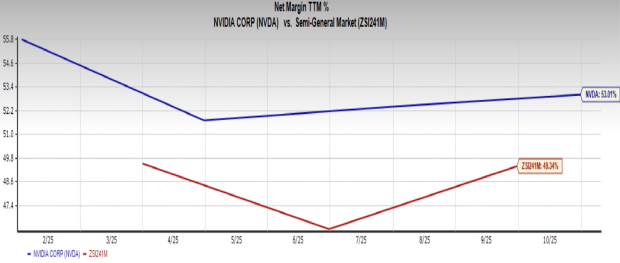

Moreover, NVIDIA’s lofty valuation is backed by strong fundamentals and not speculation, suggesting that the stock is not in a bubble. NVIDIA has a net profit margin of 53%, more than the industry's 49.34%, clearly indicating significant growth.

Image Source: Zacks Investment Research

NVIDIA, thus, currently has a Zacks Rank #1 (Strong Buy), and its $4.66 Zacks Consensus Estimate for earnings per share implies growth of 10.7% year over year. You can see the complete list of today’s Zacks #1 Rank stocks here.

Image Source: Zacks Investment Research

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 54 min | |

| 1 hour | |

| 1 hour | |

| 5 hours | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-09 | |

| Aug-08 | |

| Aug-08 | |

| Aug-08 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite