|

|

|

|

|||||

|

|

|

Stryker Corporation SYK reported fourth-quarter 2025 adjusted earnings per share (EPS) of $4.47, which beat the Zacks Consensus Estimate of $4.40 by 1.6%. The bottom line also improved 11.5% year over year. Our model estimate for the metric was pegged at $3.15 per share.

GAAP EPS was $2.22, up 2.8% from the year-ago quarter’s level.

For the full year, adjusted EPS gained 11.8% to $13.63. GAAP EPS was $8.40, up 8.2% from the year-ago level.

Revenues totaled $7.17 billion, which beat the Zacks Consensus Estimate by 0.6%. The top line also improved 11.4% on a year-over-year basis and 10.4% at constant currency (cc). Organically, sales were up 11%. Organic sales growth was driven by a 10.9% increase in unit volume and 0.1% improvement in prices.

The company reported full-year sales of $25.1 billion, up 11.2% on a year-over-year basis. Sales were up 10.7% at cc and up 10.3% on an organic basis.

Revenues in the United States amounted to $5.44 billion, up 11.7% from the prior-year quarter’s level. International sales increased 10.6% year over year to $1.73 billion.

Stryker Corporation price-consensus-eps-surprise-chart | Stryker Corporation Quote

Stryker signed an agreement during the first quarter to sell its U.S. spinal implants business to Viscogliosi Brothers, LLC, a family-owned investment firm specializing in the neuro-musculoskeletal space. The new company will be called VB Spine, LLC. Stryker also plans to sell its related international business. The divestment was completed in April 2025.

The company now reports its Spine enabling technologies results as part of other orthopedics. Interventional Spine results are reported as part of neurocrine. As a result, spinal implants are now reported separately within orthopedics.

MedSurg and Neurotechnology: This segment reported sales of $4.6 billion, up 17.5% year over year and 16.6% at cc.

In the quarter under review, MedSurg and Neurotechnology recorded organic sales growth of 12.6%, which included 13% of U.S. organic growth and 10.9% of international organic growth. Instruments recorded U.S. sales growth of 19.1%, led by high-teens growth in both Surgical Technologies and Orthopaedic instruments businesses. Performance was fueled by strong capital demand in power tools, Steri-Shield, smoke evacuation and Neptune Waste Management.

Endoscopy saw 11.1% U.S. growth on the back of robust double-digit performances in sustainability and Sports Medicine businesses and high single-digit growth in core Endoscopy portfolio. Moreover, continued strong demand for Sports Medicine shoulder products and the 1788 video platform further boosted sales. Medical grew 13.6% organically in the United States, driven by strong Acute Care sales (ProCuity, Vocera, LIFEPAK 35) and Sage business. The company does not expect the supply-chain constraints to continue in 2026.

Vascular grew 4.3% organically in the United States, on the back of strong growth in hemorrhagic business driven by the recent launch of Surpass Elite flow diverting stent, partially offset by competitive pressures in ischemic business.

Meanwhile, including peripheral vascular business added with Inari acquisition, sales growth for Vascular was 115.9% reportedly in the United States. Neurocranial saw 9.9% growth, led by strong double-digit growth in IVS and Craniomaxillofacial businesses.

Internationally, sales were up 10.9%, driven by growth in the Endoscopy and Neurocranial businesses, with especially strong performances in South Korea, Australia, New Zealand and emerging markets. However, the European market remained weak amid a slower capital environment.

Orthopedics: Sales in the segment amounted to $2.61 billion, up 2.2% year over year and 0.9% at cc. Organically, sales were up 8.4%, which included organic growth of 9.6% in the United States and 5.4% internationally. The U.S. knee business grew 7.6% organically, reflecting its market-leading position in robotic-assisted knee procedures and momentum from the continued strength of its new Mako installations.

U.S. hips business grew 5.6% organically, driven by Insignia hip stem’s success and Mako robotic platform’s momentum. Mako’s expanded ability to address more complex primary hip cases as well as hip revisions further boosted sales. Organically, Trauma and Extremities business improved 8.5%, led by strong core trauma and upper extremities growth. U.S. Other Ortho business grew 28.7% organically with strong adoption of Mako 4. International Orthopaedics grew 5.4% organically, with strength in Canada and several emerging markets.

Adjusted gross profit totaled $4.68 billion in the reported quarter, up 11.3% from the year-ago quarter’s level. Adjusted gross margin, however, contracted 10 basis points (bps) to 65.2%. The contraction primarily reflects the impact of tariffs that were mostly offset by business mix and cost improvements.

Total operating expenses were $2.82 billion, down 21.4% from the year-ago quarter’s level.

Adjusted operating income totaled $2.16 billion, up 15.2% from the year-ago level. Adjusted operating margin was 30.2%, up 100 bps.

Stryker exited the fourth quarter with cash and cash equivalents of $4.01 billion compared with $3.26 billion at the end of the third quarter of 2025.

Cumulative net cash provided by operating activities totaled $5.04 billion compared with $4.24 billion a year ago.

Stryker issued its guidance for 2026. The company expects total revenues to grow in the range of 8-9.5% on an organic basis. The Zacks Consensus Estimate for total revenues is pegged at $27.23 billion, implying growth of 8.6%.

SYK expects EPS for full-year 2026 to be in the range of $14.90 to $15.10. The Zacks Consensus Estimate for earnings is pegged at $14.98 per share.

Stryker’s fourth-quarter performance reflected strong execution across its diversified portfolio and continued momentum in key product franchises.

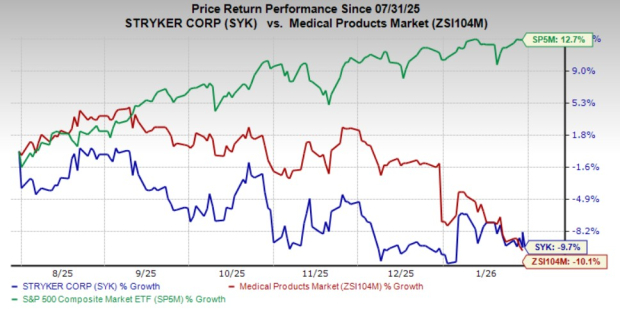

Following a strong quarterly performance, shares of SYK were up 2% during pre-market trading on Jan. 30. However, in the last six-month period, SYK’s shares have lost 9.7% compared with the industry’s 10.1% decline. The S&P 500 increased 12.7% in the same time frame.

Stryker has entered 2026 with one of the most durable growth runways in global MedTech, underpinned by accelerating robotics adoption, a strong capital cycle, and a disciplined pricing and margin framework. Management highlighted that hospital CapEx budgets remain healthy and Stryker’s enters 2026 with an elevated capital order book, providing high visibility for its capital and procedure-linked businesses. This is particularly important for the Orthopaedics franchise, where Mako remains the primary growth engine and a long-term standard-of-care catalyst rather than a cyclical product wave.

Mako adoption continues to deepen. The global installed base now exceeds 3,000 systems, with more than two-thirds of U.S. knees and over one-third of U.S. hips already performed on Mako. Utilization is still rising, and international penetration remains significantly below U.S. levels, creating a long runway for growth. The transition to Mako 4 has been a clear inflection point, driving record placements and strong hospital ROI.

Importantly, new applications — revision hips, spine, and the highly anticipated shoulder platform — are set to be launched on Mako 4 in mid-2026, materially expanding the addressable market. Each new application carries a one-time software or license fee, layering incremental revenues on top of the installed base. The newly launched handheld Mako RPS further broadens Stryker’s robotics portfolio by targeting ASCs and surgeons not yet ready for full robotics adoption.

Pricing is another tailwind. Management expects pricing improvement in 2026 to be similar to 2025, building on prior gains. Meanwhile, new product launches may enter the market at higher price points. Internationally, Stryker sees significant upside as regulatory bottlenecks ease in Europe and Mako adoption accelerates in Japan and other high-growth markets.

Finally, Stryker expects to continue expanding margins despite an estimated $400 million tariff headwind in 2026, reflecting the company’s strengthened operating model and pricing power. With robotics, capital momentum, international expansion, and layered pricing, Stryker is well positioned for another year of above-market growth.

Stryker currently carries a Zacks Rank #3 (Hold).

Some better-ranked stocks in the broader medical space are Boston Scientific Corporation BSX, Phibro Animal Health PAHC and AtriCure ATRC. Each stock presently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Boston Scientific shares have lost 12% in the past six months. Estimates for the company’s fourth-quarter 2025 EPS have remained constant at 78 cents in the past 30 days. BSX’s earnings beat estimates in each of the trailing four quarters, delivering an average surprise of 7.36%. In the last reported quarter, it posted an earnings surprise of 5.63%.

Estimates for Phibro Animal Health’s EPS for second-quarter fiscal 2026 have remained constant at 69 cents in the past 30 days. Shares of the company have risen 50.5% in the past six months compared with the industry’s 11.1% growth. PAHC’s earnings surpassed estimates in each of the trailing four quarters, the average surprise being 20.77%. In the last reported quarter, it delivered an earnings surprise of 23.73%.

AtriCure shares have risen 5.2% in the past six months. Estimates for the company’s fourth-quarter 2025 loss per share have remained stable at 4 cents in the past 30 days. ATRC’s earnings beat estimates in each of the trailing four quarters, delivering an average surprise of 67.06%. In the last reported quarter, it posted an earnings surprise of 90.91%.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-10 | |

| Aug-10 | |

| Aug-05 | |

| Aug-05 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 |

Stryker nets $6.6bn revenue in Q2; highlights resilience following cyberattack

SYK -6.42%

Medical Device Network

|

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite