|

|

|

|

|||||

|

|

|

PayPal Holdings PYPL has seen its stock tumble 23.3% in the past three months, weighed down by macroeconomic uncertainty and heightened competition in the digital payments space. Additionally, tariff-related pressures in Asia have added to near-term volatility.

Rivals like Visa V and Mastercard MA are steadily broadening their services, challenging PayPal’s dominance in digital payments. Visa stock has declined 2.6%, while Mastercard has fallen 1.5% in three months.

Investors are now questioning whether PayPal’s struggles represent a deeper problem or an opportunity to buy into a long-term recovery story. Let’s delve deeper into this.

PayPal is no longer just a payments company; it is steadily evolving into a broader commerce platform. The company announced that it has filed applications to the Utah Department of Financial Institutions and the Federal Deposit Insurance Corporation (FDIC) to establish PayPal Bank, a proposed Utah-chartered industrial loan company.

The company’s new PayPal Ads Manager allows small businesses that use PayPal to become their own retail media networks, creating additional revenue streams. It launched “PayPal links,” wherein users are able to send and receive money easily through a personalized, one-time link that can be shared in any chat or conversation. Additionally, PayPal World further expands its reach by unifying major payment systems and digital wallets on a single platform. These innovations extend PayPal’s relevance well beyond traditional payments, potentially positioning it as a foundational player in next-generation digital commerce.

PayPal is investing in AI-driven e-commerce via “agentic commerce” where autonomous AI agents help consumers discover, compare and buy products. PayPal launched its agentic commerce services in October 2025, featuring Store Sync. This month, the company announced that it has agreed to acquire Cymbio, a platform for multi-channel orchestration that enables brands to sell across agentic platforms like Microsoft Copilot and Perplexity, as well as other e-commerce channels. Moreover, PayPal teamed up with Microsoft to power the launch of Copilot Checkout in Copilot, enabling shoppers to discover, decide and pay entirely within the Copilot interface.

Similarly, PayPal and OpenAI have formed a partnership to enable seamless payments and agentic commerce experiences directly within ChatGPT. The company also partnered with Perplexity to enable agentic commerce on the Perplexity Pro platform, allowing U.S. consumers to check out instantly with PayPal or Venmo.

Venmo stands out as a major growth driver, serving as the top choice for money transfers among young, affluent and tech-savvy users. In the third quarter of 2025, Venmo revenues surged more than 20% year over year, with Venmo Debit Card monthly active account growth of more than 40% and Pay with Venmo TPV soaring approximately 40%. Venmo remains poised to deliver $1.7 billion in 2025 revenues, excluding interest income. This reflects more than 20% growth and a 10-point acceleration from two years ago.

The company’s CFO, Jamie Miller, highlighted that its branded checkout business is expected to grow a couple of points lower in the fourth quarter of 2025 compared with the previous quarter. Per management, in 2026, the company will continue investing, but higher operating expenses (OpEx) will lead to slower growth in both transaction margin dollars and earnings per share compared with 2025. This means OpEx is projected to grow at the same rate as the transaction margin dollar in 2026, instead of at half the rate that was expected before.

In the third quarter of 2025, PayPal’s basket sizes or average order value declined amid cautious consumer spending in the retail category. The company's payment transactions decreased 5% to 6.3 billion, when payment service provider (“PSP”) transactions are included. Transaction losses increased by 50% year over year, primarily due to a rise in fraud incidents from PayPal’s products and services.

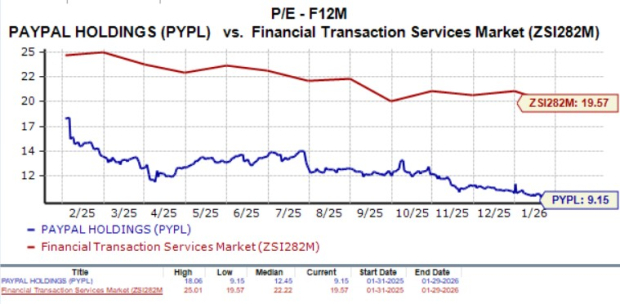

However, with the decline, PayPal shares are trading cheap, as suggested by the Value Score of A. In terms of forward 12-month P/E, PYPL stock is trading at 9.15X compared with the Zacks Financial Transaction Services industry’s 19.57X.

The stock is also cheaper than competitors, including Visa and Mastercard. Shares of Visa and Mastercard are currently trading at P/E of 24.46X and 27.02X, respectively.

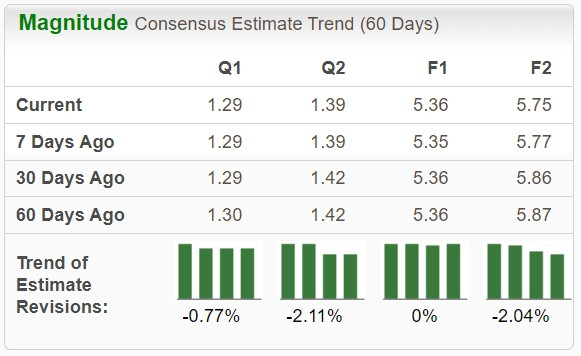

PayPal’s estimate revisions reflect a negative trend for full-year 2026. The Zacks Consensus Estimate for PYPL’s 2026 earnings per share has moved 2 cents downward to $5.75 over the past week.

Although PayPal is transforming into a next-gen ecosystem, investing in agentic commerce and growing the Venmo business, it faces a confluence of challenges that make it an unattractive investment proposition in the current environment. With macroeconomic uncertainty and rising competition, PYPL's Zacks Rank #4 (Sell) reflects the growing downside risk.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Although the recent sell-off has made PayPal’s shares appealing for long-term investors, it’s wise to remain cautious before buying. The stock trades at a significant discount compared to its industry multiples and competitors, presenting a compelling entry opportunity into this global payment leader. Despite a cheap valuation, the stock seems better to sell on downward estimate revisions and wait for stability.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 5 hours | |

| 6 hours | |

| 7 hours | |

| 8 hours | |

| 12 hours | |

| 13 hours | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite