|

|

|

|

|||||

|

|

|

Two key players in the consumer finance space that target the underserved credit segments, such as subprime and non-prime borrowers, are Pagaya Technologies Ltd. PGY and OneMain Holdings, Inc. OMF. However, both have different operating models and revenue streams.

Pagaya represents the next generation of consumer finance, built on an artificial-intelligence (AI)-powered, capital-light platform that partners with banks and lenders rather than holding large loan books itself. In contrast, OneMain is a traditional non-prime lender with a well-established nationwide footprint, originating and servicing unsecured and secured installment loans directly to consumers through physical branches and digital channels.

Though more exposed to macroeconomic cycles and subprime credit risk than Pagaya’s model, OneMain places a strong emphasis on shareholder returns via dividends and buybacks, and benefits from a long record of navigating credit cycles successfully.

Let us see if Pagaya’s AI-powered growth momentum can subdue OMF’s proven marketplace supremacy. While both face headwinds from shifting consumer spending patterns and market uncertainties, let us decipher which stock is better placed for long-term growth.

PGY has a capital-light, flexible operating model, which initially centered on personal lending, but the company has since broadened its reach into auto loans and point-of-sale financing. This expansion has spread risk across multiple asset classes, reducing dependence on any single loan segment and supporting performance through varying economic conditions. On the funding side, PGY has cultivated relationships with more than 135 institutional investors and relies on forward-flow agreements, under which partners commit capital for future loan purchases. These arrangements enhance funding predictability and provide a buffer against market volatility.

A key differentiator is PGY’s proprietary tech and product suite. Its pre-screen solution allows lenders to present pre-approved offers to existing customers without formal applications, helping partners boost credit access and deepen relationships with minimal marketing spend.

Pagaya operates with minimal on-balance-sheet exposure. Loans are typically acquired immediately by asset-backed securities (ABS) vehicles or via forward flow agreements, thanks to capital raised in advance. This approach limits credit and market risk, preserving flexibility during turbulent environments. By relying on forward flow agreements and strategic ABS issuance, Pagaya has maintained liquidity and minimized loan write-downs.

In 2025, Pagaya hit an inflection point with improving fundamentals and profitability. Despite macroeconomic headwinds and regulatory risks, the company posted three consecutive quarters of positive GAAP net income, a dramatic turnaround from substantial losses in the previous years. In the nine months ended Sept. 30, 2025, PGY’s net income was $47.1 million against a net loss of $163.5 million in the prior-year period. The company’s robust results were driven by strong network volume growth, improved monetization, better operating leverage and solid credit discipline, supported by an improvement in capital structure.

Moreover, driven by both portfolio seasoning and structural changes in funding and underwriting, PGY’s credit-related losses and impairments improved drastically from the 2024 reported levels. In the nine months ended Sept. 30, 2025, credit-related impairment losses on investments in loans and securities declined by more than $95 million on a year-over-year basis. Lower impairments reflect better-performing loan vintages, more stable delinquency and charge-off trends, and improved accuracy of PGY’s AI-driven underwriting models.

OMF provides unsecured and secured personal installment loans, often used for debt consolidation, home improvements, medical expenses and other large personal needs, while operating through 1,300 locations across 47 states. It also offers optional credit and non-credit insurance products, such as life, disability and involuntary unemployment insurance.

Revenue growth has been a major strength for OneMain. The company’s revenues witnessed a five-year (2019-2024) compound annual growth rate (CAGR) of 3.6%, with momentum continuing in the first nine months of 2025. Its loan mix of Front Book and Back Book aims for revenue sustainability while maintaining an upside potential in a rapidly changing macroeconomic environment. OMF frequently securitizes portions of its loan book via OneMain Financial Issuance Trust to reduce funding costs and manage balance sheet exposure. Its 2024 acquisition of Foursight Capital LLC expanded its presence into the auto lending business.

As a subprime lender, OMF is more exposed to credit risk and macroeconomic cycles. However, the company employs rigorous underwriting and servicing, supported by centralized data analytics, and has a strong record of managing credit performance, even during downturns.

OMF focuses on sustainable shareholder returns through dividends and buybacks. Since initiating dividends in 2019, it has raised them eight times, with the latest increase of 1% announced in October 2025. The board of directors approved a $1-billion share repurchase program, which will remain in effect until Dec. 31, 2028 (replacing the prior authorization, which had $556.4 million remaining as of Sept. 30, 2025).

Thus, OMF’s efforts to grow credit cards and auto finance businesses, along with lower rates and a diversified product base, are expected to support top-line expansion.

In the past year, shares of Pagaya have performed exceptionally well, given bullish investor sentiments. The stock has skyrocketed 117.1%, whereas OMF has gained 19%. Hence, in terms of investor sentiments, PGY has the edge.

From a valuation perspective, Pagaya is currently trading at a trailing 12-month price-to-book (P/B) of 3.02X, while the OMF stock is trading at a trailing 12-month P/B of 2.30X. So, in terms of valuation, PGY is expensive compared with OneMain.

Pagaya’s return on equity (ROE) of 44.45% is above OneMain’s 22.70%. This reflects that PGY is more efficient in using shareholder funds to generate profits.

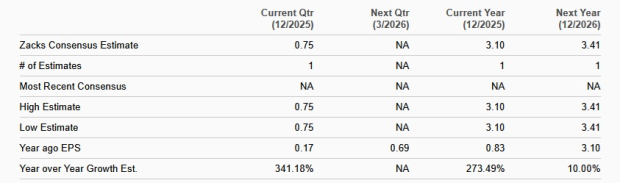

The Zacks Consensus Estimate for PGY’s 2025 and 2026 revenues indicates year-over-year growth of 28.4% and 19.2%, respectively.

The consensus estimate for PGY’s earnings indicates 273.5% and 10% year-over-year growth for 2025 and 2026, respectively.

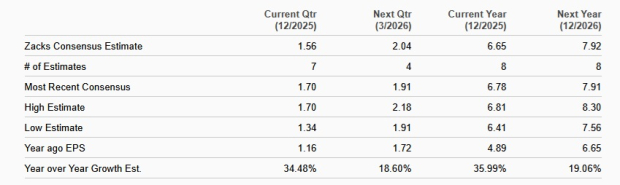

On the contrary, the Zacks Consensus Estimate for OMF’s 2025 and 2026 revenues implies year-over-year increases of just 8.9% and 7.5%, respectively.

Also, the consensus estimate for OneMain’s earnings indicates 36% growth for 2025 and a 19.1% rise for 2026.

Given its strong performance in 2025, resilient business model and capital-efficient funding strategy, PGY stands out in the fintech space. Its AI-driven platform, diversified revenue streams and reliance on forward flow agreements shield it from market volatility and credit risks. Moreover, the company’s significantly stronger revenue and earnings growth prospects than OneMain enhance its appeal as a high-upside investment opportunity.

While OMF boasts a well-established marketplace model and a more attractive valuation, PGY’s compelling growth trajectory makes it better positioned for long-term gains, justifying the premium valuation.

PGY currently carries a Zacks Rank #3 (Hold), whereas OneMain has a Zacks Rank #4 (Sell).

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-23 | |

| Jul-21 | |

| Jul-20 | |

| Jul-16 | |

| Jul-09 | |

| Jul-08 | |

| Jun-30 | |

| Jun-15 | |

| Jun-11 | |

| Jun-10 | |

| Jun-08 | |

| May-27 | |

| May-26 | |

| May-21 | |

| May-11 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite