|

|

|

|

|||||

|

|

|

Joby Aviation is a leader in eVTOL certification, though it faces notable risks related to its business model and funding.

Future dilution is likely due to high cash burn and upcoming capital needs.

Competition from autonomous eVTOLs, especially Boeing's Wisk, poses a long-term threat, but Joby's potential first-mover advantage is significant.

Electric vertical take-off and landing (eVTOL) company Joby Aviation (NYSE: JOBY) has an exciting future and more potential upside than rivals like Archer Aviation (NYSE: ACHR), but it also carries big risks that need to be addressed before buying the stock. As such, here's a risk/reward analysis of the stock.

While Archer is focused on becoming an original equipment manufacturer (OEM) and selling eVTOL aircraft to third parties, Joby's main aim is to create a vertically integrated transportation services company. In other words, make, own, and operate its aircraft itself.

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

That business model choice creates additional risk on top of the usual Federal Aviation Administration (FAA) certification risk every eVTOL company faces.

Joby is ahead in the certification race and has performed exceptionally well so far, considering that it's largely developing its own technology and components, while Archer is leaning into established companies like Stellantis, Honeywell, and Safran for technology and components.

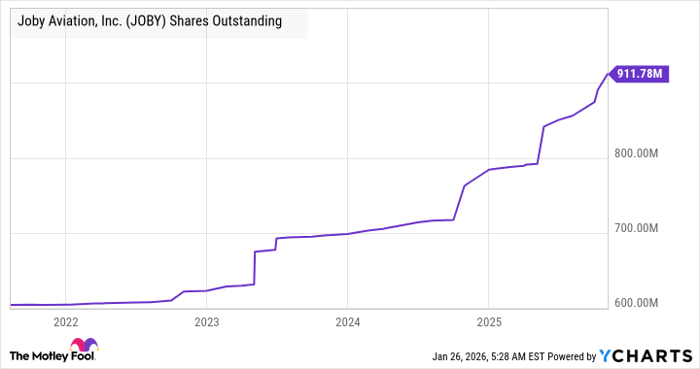

That said, Joby is already in the final stage of certification, during which FAA pilots test the aircraft and the FAA assesses reliability and operational readiness. There's no guarantee that Joby will receive approval. The second risk is that the substantive investment needed to build out its business could significantly dilute existing shareholders' interests.

JOBY Shares Outstanding data by YCharts

Joby needs to invest in ramping up manufacturing capacity and needs to invest in vertiports and build out an operational fleet before it starts generating revenue from air taxis. Moreover, remember that its focus is on generating revenue from services, while Archer aims to generate revenue from the sale of OEM equipment.

Finally, the Wall Street consensus implies Joby will raise cash in 2026, likely through an equity raise. It's hard to see how it will end 2026 with $1 billion in net cash, having burned through $646 million in 2026 and starting the year with just $710 million in net cash.

|

Wall Street Consensus for Joby Aviation |

2023 |

2024 |

2025Est |

2026Est |

2027Est |

|---|---|---|---|---|---|

|

Cash Burn |

$344 million |

$477 million |

$538 million |

$646 million |

$574 million |

|

Net Cash |

$1032 million |

$933 million |

$710 million |

$1034 million |

$925 million |

Data source: marketscreener.com

Joby's business model faces a long-term threat from Boeing's subsidiary, Wisk, which also plans to develop eVTOLs and offer its own air taxi services, but with an autonomous eVTOL that could potentially undercut Joby on pricing because it doesn't require a pilot.

All of that said, the reality is Joby is leading the certification race, and its partnerships and investment from Delta Air Lines (which plans to use air taxis to fly passengers to airports) and Uber (Joby's air taxi services will be on Uber's app), and Toyota is a formidable partner helping Joby with its manufacturing operations. In addition, Joby is working with Nvidia to potentially launch its own autonomous eVTOL in the future.

Image source: Joby Aviation.

Moreover, it's highly likely that Joby will have a first-mover advantage over Wisk, and autonomous eVTOLs pose significantly greater technical, regulatory, and cost challenges (Wisk is planning a ground-based operating network).

Joby is risky, but it also has plenty of upside potential through its vertically integrated business model.

Before you buy stock in Joby Aviation, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Joby Aviation wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $448,476!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,180,126!*

Now, it’s worth noting Stock Advisor’s total average return is 945% — a market-crushing outperformance compared to 197% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of January 31, 2026.

Lee Samaha has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Boeing, Honeywell International, Nvidia, and Uber Technologies. The Motley Fool recommends Delta Air Lines and Stellantis. The Motley Fool has a disclosure policy.

| 3 hours | |

| 4 hours | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 | |

| Aug-10 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite