|

|

|

|

|||||

|

|

|

AI infrastructure spending is set to soar again in 2026, which is great news for this chip designer.

The growing demand for custom AI processors has supercharged this company's growth.

This company's attractive valuation and earnings growth potential suggest that it could fly higher in 2026 and beyond.

Artificial intelligence (AI) infrastructure stocks are likely to deliver another year of solid growth in 2026. Market research firm Gartner estimates that AI infrastructure spending could jump to almost $1.4 trillion this year, up by 41% from last year's levels.

While investing in the usual suspects -- such as Nvidia, Broadcom, TSMC, or Micron Technology -- can help investors capitalize on this terrific growth, there is another AI infrastructure company that hasn't received much love on the market: Marvell Technology (NASDAQ: MRVL).

Where to invest $1,000 right now? Our analyst team just revealed what they believe are the 10 best stocks to buy right now, when you join Stock Advisor. See the stocks »

Let's look at the reasons why this overlooked AI name could be a big winner this year.

Image source: Getty Images

Marvell Technology makes application-specific integrated circuits (ASICs), which are in terrific demand right now as they are being used in AI data centers. The cost and performance advantages that ASICs enjoy over graphics processing units (GPUs) are why they are expected to corner a significant share of the AI accelerator market in the long run.

Bloomberg estimates that the market for custom ASICs deployed in AI data centers could grow at a compound annual growth rate (CAGR) of 27% through 2033, generating $118 billion in revenue. Marvell is expected to control 20% to 25% of this market by the end of the forecast period. That would translate into annual revenue of $23.6 billion to $29.5 billion for the company, according to Bloomberg's estimates, more than triple the revenue Marvell generated in the past year.

Bloomberg points out that Marvell's relationships with Amazon and Microsoft for its custom AI processors would enable it to capture a nice chunk of this lucrative opportunity. And Marvell could do better than that. That's because Marvell doesn't just make custom AI processors; it also makes networking and storage components that go into data centers.

The company estimates that its addressable market could increase at a 35% CAGR through 2028, reaching $94 billion after three years. Even better, Marvell seems firmly on track to capitalize on this massive opportunity. Its custom AI processors are used by four of the top hyperscalers in the U.S., along with emerging hyperscalers. It supplies 18 custom processor designs to these customers and estimates that it could expand those design wins to more than 50.

So, it won't be surprising to see Marvell sustaining its remarkable growth.

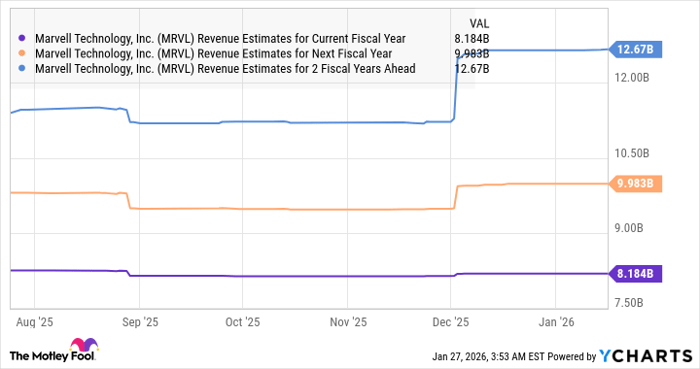

MRVL Revenue Estimates for Current Fiscal Year data by YCharts

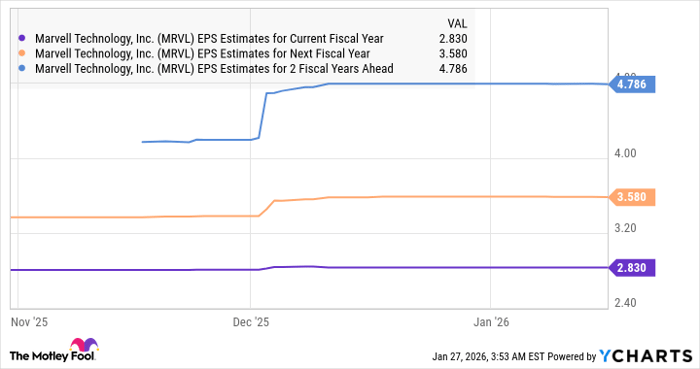

Marvell trades at an attractive 22 times forward earnings estimates. That's a slight discount to 26 multiple of the tech-laden Nasdaq-100 index. Considering that Marvell's earnings are anticipated to increase by 80% in the current fiscal year, followed by healthy growth in the next couple of years as well, buying this stock is a no-brainer right now.

MRVL EPS Estimates for Current Fiscal Year data by YCharts

Before you buy stock in Marvell Technology, consider this:

The Motley Fool Stock Advisor analyst team just identified what they believe are the 10 best stocks for investors to buy now… and Marvell Technology wasn’t one of them. The 10 stocks that made the cut could produce monster returns in the coming years.

Consider when Netflix made this list on December 17, 2004... if you invested $1,000 at the time of our recommendation, you’d have $450,256!* Or when Nvidia made this list on April 15, 2005... if you invested $1,000 at the time of our recommendation, you’d have $1,171,666!*

Now, it’s worth noting Stock Advisor’s total average return is 942% — a market-crushing outperformance compared to 196% for the S&P 500. Don't miss the latest top 10 list, available with Stock Advisor, and join an investing community built by individual investors for individual investors.

*Stock Advisor returns as of February 1, 2026.

Harsh Chauhan has no position in any of the stocks mentioned. The Motley Fool has positions in and recommends Amazon, Micron Technology, Microsoft, Nvidia, and Taiwan Semiconductor Manufacturing. The Motley Fool recommends Broadcom, Gartner, and Marvell Technology. The Motley Fool has a disclosure policy.

| Aug-10 | |

| Aug-10 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-04 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite