|

|

|

|

|||||

|

|

|

Sonos, Inc. SONO is scheduled to report first-quarter fiscal 2026 results on Feb. 3, after market close.

For the quarter, SONO anticipates revenues between $510 million and $560 million, implying a year-over-year decline of 7% to growth of 2%. The Zacks Consensus Estimate for revenues is pegged at $538.7 million, indicating a decline of 2.2% from the year-ago reported number.

The consensus estimate for earnings is pegged at 81 cents. It had reported 64 cents in the prior-year quarter.

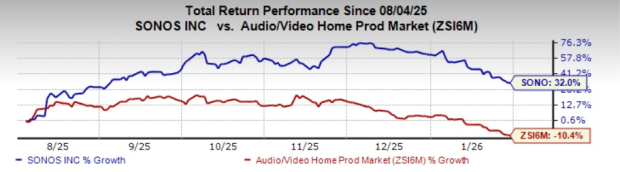

In the past six months, shares of SONO have soared 32% against the Zacks Audio Video Production industry’s decline of 10.4%.

Sonos continues to focus on driving growth through a differentiated and innovative product portfolio. On the last earnings call, the company emphasized a strategic shift from focusing on standalone, category-specific products to building a fully integrated, cohesive Sonos system, one that connects music, movies, voice, formats and AI-driven experiences across every room in the home. This new strategy is anchored in product innovation, both hardware and software, with Sonos planning to launch new hardware in the second half of fiscal 2026, including products designed for entirely new spaces and use cases the company does not currently serve.

Sonos is also investing heavily in software upgrades, AI-powered experiences and expanded support for formats like Dolby Atmos, Lossless Audio, Bluetooth, AirPlay and Spotify Connect, elevating the capabilities of the entire system. Recent product introductions, such as Arc Ultra and Sub 4, have contributed meaningfully to category momentum, helping push strong double-digit growth in home theater during the company’s last reported quarter.

Management, on the last earnings call, highlighted that ongoing enhancements and new products will attract new households, while fresh updates across the lineup will encourage existing customers to expand their systems, supporting an estimated $12 billion internal revenue opportunity.

Also, the company emphasized a renewed pricing strategy designed to attract high-quality households with strong repurchase tendencies, citing the Era 100 price reduction. Sonos plans to more aggressively engage its large installed base through targeted messaging, improved engagement and ongoing system updates that encourage multi-product adoption and repeat purchasing. Building on this momentum, Sonos has a robust product roadmap in place, stretching through fiscal 2026 and beyond.

Sonos anticipates stronger year-over-year comparisons, with new product launches concentrated in the second half of fiscal 2026. The company’s ongoing expansion of its direct-to-consumer initiatives, broader partner ecosystem and growing international presence are likely to have supported its first-quarter performance.

Sonos, Inc. price-eps-surprise | Sonos, Inc. Quote

For first-quarter fiscal 2026, the company expects GAAP gross margin of 44%–46% and non-GAAP gross margin of about 110 basis points (bps), both improving more than 100 bps year over year at the midpoint. GAAP operating expenses are expected to be between $152 million and $162 million, down about 19% year over year at the midpoint, with non-GAAP operating expenses about $16 million lower.

The company projects adjusted EBITDA between $94 million and $137 million, up 27% year over year, with a margin of around 22%, indicating about 500 bps of expansion.

However, Sonos’ fiscal first-quarter performance is likely to have been adversely impacted by multiple headwinds, which include cautious discretionary spending, higher promotions and uncertain tariff policy. Sonos continues to navigate these challenges that might hurt its margins and weaken its competitive edge.

On the last earnings call, Sonos stated that it continues to anticipate tariff rates on its products to be 20% for Vietnam and 19% for Malaysia. Although the company is working closely with contract manufacturers and channel partners to share these costs, it has determined that price increases on certain products will be necessary later in 2025. On the last earnings call, management highlighted that it anticipates the effective tariff rate will increase and level off in the second quarter, creating an additional 100 bp headwind compared with the first quarter.

Our proven model does not predict an earnings beat for SONO this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy), or 3 (Hold) increases the odds of an earnings beat. That is not the case here.

SONO has an Earnings ESP of 0.00% and a Zacks Rank #3. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Here are some stocks you may consider, as our model shows that these have the right combination of elements to beat on earnings this season.

Cirrus Logic, Inc. CRUS currently has an Earnings ESP of +5.90% and a Zacks Rank #1. You can see the complete list of today’s Zacks #1 Rank stocks here.

CRUS is scheduled to report quarterly earnings on Feb. 3. The Zacks Consensus Estimate for CRUS’ to-be-reported quarter’s earnings and revenues is pegged at $2.42 per share and $536.3 million, respectively. Shares of CRUS have gained 31.2% in the past year.

Advanced Micro Devices, Inc. AMD has an Earnings ESP of +2.01% and a Zacks Rank #2 at present. AMD is scheduled to report quarterly figures on Feb. 3. The Zacks Consensus Estimate for AMD’s to-be-reported quarter’s earnings and revenues is pegged at $1.32 per share and $9.67 billion, respectively. Shares of AMD have skyrocketed 107.1% in the past year.

Capri Holdings Limited CPRI presently has an Earnings ESP of +3.47% and a Zacks Rank #2. CPRI is scheduled to report quarterly numbers on Feb. 3. The Zacks Consensus Estimate for CPRI’s to-be-reported quarter’s earnings and revenues is pegged at 78 cents per share and $998.3 million, respectively. Shares of CPRI have risen 23.3% in the past six months.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 3 hours | |

| 3 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours | |

| 4 hours | |

| 5 hours | |

| 5 hours | |

| 5 hours | |

| 5 hours | |

| 6 hours | |

| 6 hours | |

| 8 hours | |

| 8 hours | |

| 9 hours |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite