|

|

|

|

|||||

|

|

|

Amazon AMZN is scheduled to report fourth-quarter 2025 results on Feb. 5.

For the fourth quarter, the company projects net sales between $206 billion and $213 billion, suggesting 10% to 13% growth compared to the fourth quarter of 2024, with this guidance anticipating a favorable impact of approximately 190 basis points from foreign exchange rates.

The Zacks Consensus Estimate for net sales is pegged at $211.56 billion, indicating growth of 12.66% from the prior-year quarter’s reported figure.

The Zacks Consensus Estimate for fourth-quarter earnings is pegged at $1.98 per share, which indicates growth of 6.45% from the year-ago quarter.

The company has been benefiting from its dominant position in the e-commerce and cloud markets. It is also riding on strengthening generative AI capabilities.

Amazon has an impressive earnings surprise history. In the last reported quarter, the company delivered an earnings surprise of 23.42%. The company’s earnings beat the Zacks Consensus Estimate in each of the trailing four quarters, the average surprise being 22.47%.

Amazon.com, Inc. price-eps-surprise | Amazon.com, Inc. Quote

Our proven model does not predict an earnings beat for Amazon this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. You can uncover the best stocks to buy or sell before they are reported with our Earnings ESP Filter.

AMZN has an Earnings ESP of -1.05% and carries a Zacks Rank #2 at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

As Amazon is set to report its fourth-quarter 2025 earnings, multiple catalysts positioned the company for solid performance across its diversified business segments, supported by strategic initiatives in cloud computing, advertising, and e-commerce that are expected to have driven solid performance.

Amazon Web Services (“AWS”) is likely to have maintained its reacceleration trajectory in the fourth quarter after achieving 20% year-over-year growth in the third quarter to $33 billion. The Zacks consensus estimate for fourth-quarter AWS revenues indicates 21.6% year-over-year growth to $35.02 billion in the to-be-reported quarter.

The annual AWS re:Invent conference, held from Nov. 30 to Dec. 4, showcased significant innovations, including Graviton5 processors delivering 25% higher performance, Trainium3 UltraServers for AI model training, and Amazon Nova 2 foundation models. The introduction of Database Savings Plans, reducing costs by up to 35%, and AWS Transform capabilities for code modernization positioned the cloud segment favorably for enterprise adoption. This is expected to have strengthened AWS' competitive positioning in the rapidly expanding AI infrastructure market against its strong contenders like Microsoft MSFT, Alphabet GOOGL and Oracle ORCL.

Management's investment of approximately $125 billion in capital expenditures for 2025, with expectations to increase in 2026, underscored its commitment to AI infrastructure expansion.

Prime Big Deal Days on Oct. 7-8 provided a significant catalyst for the fourth quarter, expanding to 18 countries, including new markets in Colombia, Ireland, and Mexico. The exclusive member event kicked off the holiday shopping season ahead of Black Friday, driving traffic across categories including home goods, fashion, beauty, and technology.

Third-party seller services remain a significant growth driver with Zacks estimates pegged at $52.2 billion, indicating a 10.09% year-over-year increase. The company's focus on expanding selection with premium brands and enhancing delivery capabilities positioned the segment for continued growth in the fourth quarter.

Amazon's physical retail operations are expected to show healthy growth, with the Zacks Consensus Estimate projecting physical store sales of $5.87 billion, indicating a 5.3% year-over-year increase. Amazon's physical retail operations benefited from the completion of same-day perishable grocery delivery expansion to 2,300-plus cities and towns by year-end as planned. The introduction of Amazon Now ultra-fast deliveries in 30 minutes in select areas of Seattle and Philadelphia during the quarter enhanced the convenience proposition for household essentials and fresh groceries, strengthening competitive differentiation.

The online stores segment is likely to have gained traction from AI-powered shopping features, including Rufus assistant usage by 250 million customers and the Help Me Decide feature leveraging browsing activity and preferences. The expansion of Multi-Channel Fulfillment to sellers using Walmart, Shopify, and SHEIN broadened the ecosystem reach. The extended holiday return policy implemented from Nov. 1 through Dec. 31 balanced customer satisfaction with inventory management efficiency. Our consensus mark for revenues from online stores is pegged at $82.4 billion, indicating a 9.06% year-over-year increase.

The unBoxed 2025 conference in Nashville on Nov. 11-12 introduced Campaign Manager, Ads Agent, and Creative Agent, advancing Amazon's advertising capabilities. Partnerships with Netflix, Spotify, and SiriusXM, announced in the third quarter, are likely to have contributed to fourth-quarter advertising performance. Amazon's ad-supported monthly reach exceeded 300 million consumers in the United States, providing significant scale for brand partners. Our consensus mark for revenues from advertising services is pegged at $21.2 billion, indicating a 22.6% year-over-year increase.

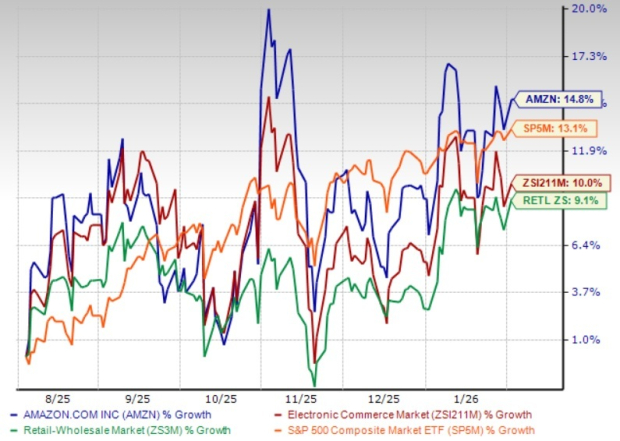

Shares of Amazon have gained 14.8% in the past six-month period compared with the broader Zacks Retail-Wholesale sector and the S&P 500 index’s return of 9.1% and 13.1%, respectively.

Now, let’s look at the value Amazon offers investors at current levels. AMZN is trading at a premium with a forward 12-month P/S of 3.23X compared with the Zacks Internet - Commerce industry’s 2.24X, reflecting a stretched valuation.

Amazon represents a compelling buy ahead of fourth-quarter 2025 results despite premium valuation and competitive pressures. AWS accelerated to 20% growth with a $200 billion backlog, while AI investments totaling $125 billion position the segment for sustained leadership. The advertising platform's 300 million consumer reach and AI-powered tools strengthen monetization capabilities. E-commerce benefits from enhanced AI shopping experiences and grocery expansion, reaching 2,300 cities. Strong holiday performance following Prime Big Deal Days and comprehensive re:Invent innovations demonstrate Amazon's diversified growth drivers across cloud computing, advertising, and retail segments, which justify investment despite elevated multiples and intense competition from technology peers.

Amazon's diversified business model, accelerating AWS growth, and strategic AI infrastructure investments position the company for robust fourth-quarter performance. The combination of strong revenue guidance, expanded advertising capabilities, and enhanced e-commerce experiences through AI-powered tools creates multiple growth catalysts. Despite premium valuation and competitive headwinds, Amazon's comprehensive ecosystem and innovation leadership make the stock an attractive buy ahead of earnings.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-25 | |

| Jul-25 | |

| Jul-25 | |

| Jul-25 | |

| Jul-25 |

Dow Jones Futures: Market Triggers Sell Signal; Apple Earnings, Iran News, Fed Meeting In Focus

AMZN MSFT

Investor's Business Daily

|

| Jul-25 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 | |

| Jul-24 |

What to watch next week: Big Tech earnings, the Fed, and Consumer Confidence

GOOGL MSFT

Yahoo Finance Video

|

| Jul-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite