|

|

|

|

|||||

|

|

|

EMCOR Group, Inc. EME reported an exceptional operating margin of 9.1% for the first nine months of 2025, driven by the successful management of its project portfolio. The company’s strategy focuses on high-demand, high-return sectors such as data centers, health care, manufacturing, transportation and water infrastructure. Specifically, the Network and Communications sector reached a record $4.3 billion in Remaining Performance Obligations (RPOs), nearly doubling year over year, backed by robust data center demand. This high-value project mix is a primary reason for the margin expansion seen in their Industrial and Building Services segments.

By selectively pursuing complex projects in resilient markets, EMCOR has both protected margins and, as of Sept. 30, 2025, built a record $12.61 billion total backlog, enhancing long-term visibility. While project selection creates the opportunity for higher returns, management continues to stress that disciplined execution remains the core driver of performance. The company’s use of advanced construction technologies — such as Virtual Design and Construction, Building Information Modeling and extensive prefabrication — has improved labor productivity, planning accuracy and cost control.

Although the shift toward large-scale, mission-critical data center and industrial projects provides a meaningful structural tailwind, management emphasized that sustained margin strength ultimately hinges on execution quality. Record RPOs and robust data center demand are driving backlog growth and longer-duration projects, placing a premium on disciplined planning, efficient resource allocation and consistent execution.

EMCOR’s ability to scale successfully into new geographies, expanding electrically from just four data center markets in 2019 to more than 16 today, further underscores its capacity to execute reliably at scale and support elevated margins over time.

EMCOR operates in a highly competitive public infrastructure market alongside established peers such as Quanta Services, Inc. PWR and Sterling Infrastructure, Inc. STRL, particularly in data center-related projects.

Quanta Services represents a relevant peer with a strong margin profile, underpinned by its exposure to electrical infrastructure and high-demand end markets. Similar to EMCOR, Quanta Services is benefiting from secular tailwinds tied to AI, data centers, electrification, grid modernization and power generation investment. It is continuing to support solid earnings, cash generation and sustained project momentum.

On the other hand, Sterling is experiencing accelerating momentum in mission-critical projects, supported by strong demand across data centers, manufacturing and e-commerce distribution. In the third quarter of 2025, Sterling delivered 32% year-over-year revenue growth, driven by a 58% increase in its E-Infrastructure segment, including 42% organic growth. This acceleration was led by the data center market, where revenues surged more than 125% year over year as customers increasingly shifted toward larger, more complex and multi-phase projects.

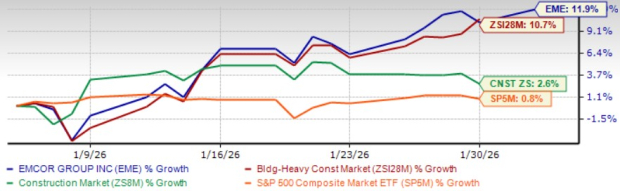

Shares of this Connecticut-based infrastructure service provider have gained 11.9% in the past month, outperforming the Zacks Building Products - Heavy Construction industry, the broader Construction sector and the S&P 500 Index.

EME stock is currently trading at a premium compared with its industry peers, with a forward 12-month price-to-earnings (P/E) ratio of 26.54, as evidenced by the chart below.

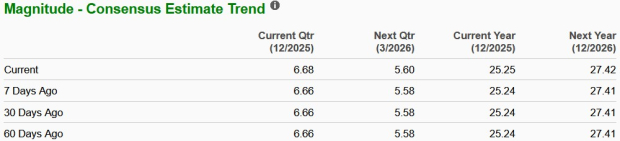

EME’s earnings estimates for 2026 have trended upward in the past seven days to $27.42 per share. The Zacks Consensus Estimate for EME’s 2026 revenues and EPS indicates 5.4% and 8.6% year-over-year growth, respectively.

EMCOR currently carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-08 | |

| Aug-06 |

Dow Jones Futures: Market Pauses With Jobs Report Due; Cloudflare, Sezzle Lead Earnings Movers

PWR

Investor's Business Daily

|

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 | |

| Jul-30 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite