|

|

|

|

|||||

|

|

|

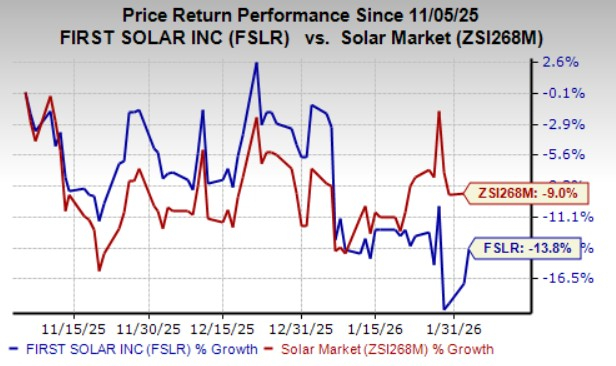

First Solar, Inc. FSLR shares have fallen 13.8% over the past three months, underperforming the Zacks Solar industry’s decline of 9%. However, the company is capitalizing on strong demand by expanding its U.S. manufacturing capacity, positioning itself to capture greater market opportunities.

Other solar stocks, such as SolarEdge Technologies SEDG and Canadian Solar Inc. CSIQ, have also underperformed the industry in the past three months. Shares of SEDG have fallen 20.8%, while those of CSIQ have dropped 20% during the same time frame.

Let's examine the factors and assess the stock's investment prospects to make an informed decision.

First Solar is seeing strong demand in the United States, fueled by the rising adoption of its advanced thin-film solar modules. The company may also benefit indirectly from the artificial intelligence boom, as the fast buildout of data centers to power artificial intelligence workloads is driving higher electricity use, which is increasing the need for renewable energy sources like solar.

The company has recently started operations at its fourth and fifth U.S. manufacturing plants and completed capacity expansions at its existing Ohio facilities. Since the last earnings call, it has secured 2.7 gigawatts (GW) of additional gross bookings, taking its total backlog to 54.5 GW through 2030, underscoring strong demand for First Solar’s products.

First Solar’s well-established operations across the United States, India, Malaysia and Vietnam provide it with a solid global footprint. Its planned 3.7 GW U.S. module finishing line, set to begin operations in the fourth quarter of 2026, is expected to further expand production capacity and support sustained revenue growth. These expansion initiatives strengthen long-term capacity visibility and add greater stability to the company’s revenue outlook.

In November 2025, First Solar announced that it would establish a $330 million facility in Gaffney, SC, to onshore final production for Series 6 Plus modules from its international fleet. The company also inaugurated a $1.1 billion AI-enabled manufacturing facility in Iberia Parish, LA, which is expected to add 3.5 GW of annual nameplate capacity once fully ramped. These moves will lift its U.S. manufacturing footprint to 14 GW in 2026 and 17.7 GW in 2027, enhancing production scale, improving supply-chain localization and strengthening its ability to meet rising domestic demand for advanced solar modules.

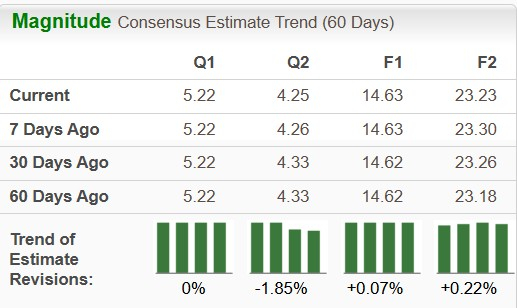

The Zacks Consensus Estimate for 2026 earnings per share (EPS) indicates an increase of 0.22% over the past 60 days. FSLR’s long-term (three to five years) earnings growth rate is 33.5%.

The Zacks Consensus Estimate for SolarEdge Technologies’ 2026 EPS calls for a decline of 21.43% in the past 60 days. The bottom-line estimate for Canadian Solar’s 2026 EPS indicates no change.

First Solar is contending with multiple challenges, including rising trade tensions and tariff risks tied to new reciprocal duties on countries where it has manufacturing operations. U.S. tariffs ranging from 19% to 25% on several of these countries and as high as 50% on India could restrict the company’s ability to sell certain modules in the United States and potentially disrupt activities at some international facilities.

The risk of a global solar module oversupply, driven largely by aggressive capacity expansion in China, may lead to price volatility and intensifying competition, which could weigh on First Solar’s financial performance.

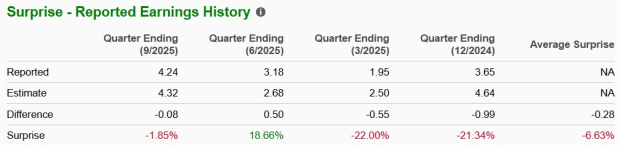

FSLR beat on earnings in one of the trailing four quarters and missed in the remaining three, delivering a negative average surprise of 6.63%.

SolarEdge Technologies outpaced earnings in three of the trailing four quarters and missed in one, delivering a negative average surprise of 24.89%. Canadian Solar surpassed earnings in two of the trailing four quarters and missed in two, delivering a negative average surprise of 173.69%.

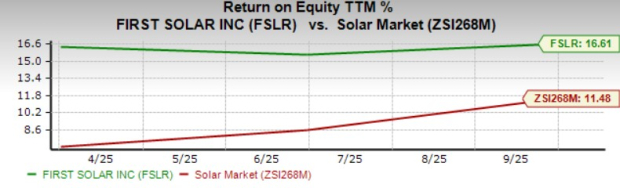

The company’s trailing 12-month return on equity of 16.61% is higher than the industry average of 11.48%. Return on equity, a profitability measure, reflects how effectively a company utilizes its shareholders’ funds to generate income.

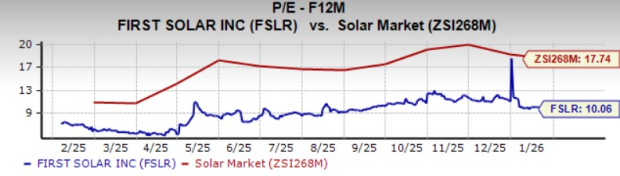

First Solar is currently trading at 10.06X, a discount compared to its industry’s 17.74X on a forward 12-month P/E basis.

First Solar is witnessing solid demand in the United States for its thin-film solar modules and is poised to benefit from rising power needs fueled by AI-driven data center expansion. Its ongoing capacity additions are expected to support long-term revenue growth while reinforcing its competitive position globally.

Considering its current price underperformance and financial pressures, new investors should wait and look for a better entry point. Those who already have this Zacks Rank #3 (Hold) stock in their portfolio may continue to retain it, considering the company’s impressive earnings growth projection and better ROE. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 | |

| Aug-05 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite