|

|

|

|

|||||

|

|

|

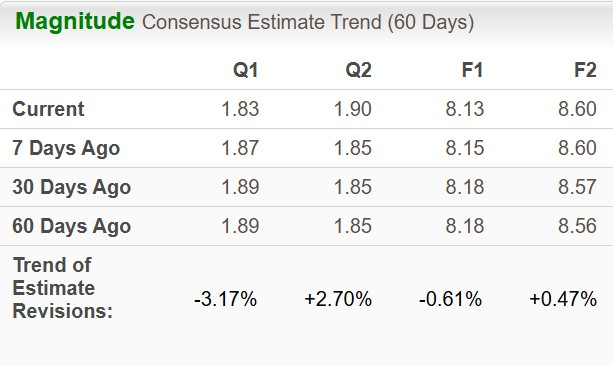

Biotech bigwig Gilead Sciences, Inc. GILD is scheduled to report fourth-quarter and full-year 2025 results on Feb. 10, after market close. The Zacks Consensus Estimate for fourth-quarter sales and earnings is pegged at $7.57 billion and $1.83 per share, respectively.

Earnings estimate for 2025 has decreased to $8.13 from $8.18 per share over the past 60 days, and that for 2026 has increased to $8.60 from $8.56 in the same time frame.

GILD has an excellent track record. Its earnings beat estimates in three of the trailing four quarters and missed in the remaining one, delivering an average surprise of 7.80%. In the last reported quarter, the company’s earnings beat estimates by 14.88%.

Per our proven model, the combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat.

Earnings ESP for GILD is -2.47%. The company currently carries a Zacks Rank #3. You can uncover the best stocks to buy or sell before they're reported with our Earnings ESP Filter.

Gilead has a market-leading HIV franchise, led by flagship HIV therapies — Biktarvy and Descovy.

Biktarvy sales and Descovy for pre-exposure prophylaxis (PrEP) have fueled GILD’s top-line growth over the past several quarters.

Biktarvy is the top revenue generator for GILD. Per the company, Biktarvy accounts for more than 52% share of the treatment market in the United States, and continues to be the market leader in major markets around the world. Roughly 75% of Descovy sales are for HIV prevention. Descovy accounts for more than 45% of the U.S. market share in PrEP market.

The top-line estimate for Biktarvy and Descovy is pegged at $3.8 billion and $703 million, respectively, and our model estimate for the same is pinned at $3.8 billion and $710 million.

GILD’s HIV portfolio received a boost with the FDA approval for its twice-yearly injectable HIV-1 capsid inhibitor, lenacapavir, for the prevention of HIV, under the brand name Yeztugo.

Yeztugo for PrEP raked in sales of $39 million in the third quarter. On the third-quarter earnings call, GILD stated that it achieved its 75% coverage goal for Yeztugo, nearly three months ahead of its target.

Hence, Yeztugo sales have likely registered a sequential increase in the fourth quarter.

Gilead expects HIV revenue growth in 2025 to be approximately 5% despite the $900 million headwind for this business associated with the Medicare Part D redesign.

Hence, HIV product sales in the fourth quarter have likely increased, driven by increased demand for Biktarvy and Descovy, along with incremental sales from Yeztugo.

The Liver Disease portfolio includes drugs for chronic hepatitis C virus, chronic hepatitis B virus (HBV) and chronic hepatitis delta virus.

Sales from this franchise increased in the third quarter, driven by higher demand for Livdelzi (seladelpar) for the treatment of primary biliary cholangitis (PBC) on the back of strong commercial execution and some new launches outside the country. The trend has likely prevailed in the fourth quarter.

Cell Therapy product sales (Yescarta and Tecartus) have likely decreased in the to-be-reported quarter due to competitive headwinds, both in the United States and internationally.

The Zacks Consensus Estimate and our model estimate for Cell Therapy product sales are pinned at $398 million and $384.3 million, respectively.

Trodelvy, indicated for second-line metastatic triple-negative breast cancer and pre-treated HR+/HER2- metastatic breast cancer, likely experienced strong demand in the fourth quarter, similar to the third quarter. The Zacks Consensus Estimate and our estimate for Trodelvy sales are pinned at $362 million and $342 million, respectively.

R&D expenses have likely remained flat year over year. SG&A expenses must have declined, as in the previous quarter.

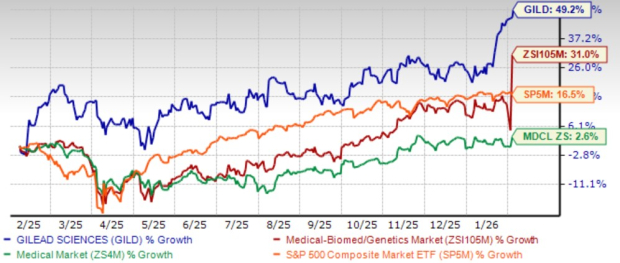

Shares of GILD have surged 49.2% in the past year compared with the industry’s growth of 31%. The stock has outperformed the sector and the S&P 500 in this time frame.

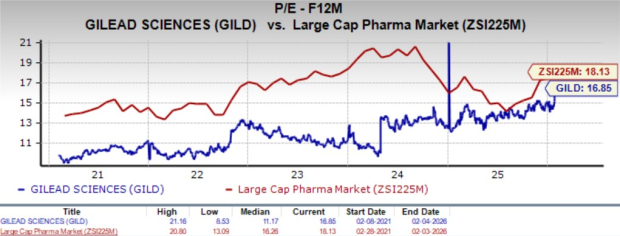

Going by the price/earnings ratio, GILD’s shares currently trade at 16.85x forward earnings, higher than its mean of 11.17x but lower than 18.13x for the large-cap pharma industry.

Gilead has a market-leading portfolio of HIV treatments and the franchise has put up a strong performance.

The company’s consistent efforts to develop additional innovative HIV treatments are being appreciated by investors. The initial uptake of Yeztugo is strong and further boosts HIV business.

Positive data from the phase III ARTISTRY-1 and ARTISTRY-2 (evaluating the investigational single-tablet regimen of bictegravir and lenacapavir for the treatment of HIV) studies is a significant boost for the company.

The approval of Livdelzi has expanded the liver-disease portfolio and the strong uptake of the drug has fuelled sales.

Trodelvy continues to gain market share in the second-line setting for metastatic breast cancer. GILD has already submitted two supplemental biologics license applications seeking approval of the drug for use in first-line metastatic patients. A potential approval in the first-line setting (regulatory decisions are expected in 2026) will boost Trodelvy sales.

However, the Cell Therapy franchise, comprising Yescarta and Tecartus, is currently under pressure due to competitive headwinds (both in the United States and Europe) that will likely weigh on the top line.

GILD’s strategic deals and acquisitions to diversify its business are encouraging.

Gilead Sciences is one of the largest biotechnology companies in the industry, and companies of this scale are often viewed as relatively safe havens for sector-focused investors. Continued innovation within its HIV portfolio should support growth despite intensifying competition from GSK plc GSK. The company’s strategic collaborations and acquisitions aimed at diversifying its revenue base are encouraging.

GILD has partnered with Merck MRK to evaluate the investigational combination of islatravir and lenacapavir for the treatment of HIV. It also entered into a collaboration with Merck in 2021 to study Trodelvy in combination with Keytruda in the ASCENT-04/KEYNOTE-D19 trial.

That said, we advise prospective investors to adopt a wait-and-watch approach as the Cell Therapy business continues to face competitive headwinds.

For existing shareholders, maintaining positions appears prudent, supported by Gilead’s decent dividend yield.

You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 10 hours | |

| Jul-23 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 | |

| Jul-20 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite