|

|

|

|

|||||

|

|

|

Alphabet (GOOGL) recently delivered a quarterly report that underscored why the company remains firmly positioned among the market’s most dominant businesses. While broader equities have experienced a spike in volatility this week, it shouldn’t distract you from Alphabet’s latest results highlighting durable growth, expanding competitive advantages and continued leadership across multiple high-value business segments.

Alphabet reported fourth-quarter and full year results that exceeded expectations, with revenue climbing 18% and annual sales surpassing $400 billion for the first time. The strength was broad-based, spanning digital advertising, cloud computing and artificial intelligence initiatives.

The report also outlined an aggressive spending plan aimed at expanding Alphabet’s AI infrastructure and capabilities. Management appears intent on investing at a scale that could widen the competitive moat, leveraging the company’s substantial cash flow to fund data centers, advanced compute and next-generation models. This financial flexibility represents a structural advantage over key competitors such as OpenAI, which must rely more heavily on external capital to support its own infrastructure buildout.

The report reinforces Alphabet’s evolution from what some investors once viewed as a lagging member of the “Magnificent Seven” into a premium leader within mega-cap technology. The company continues to demonstrate exceptional scale, operational depth and the ability to monetize emerging technologies.

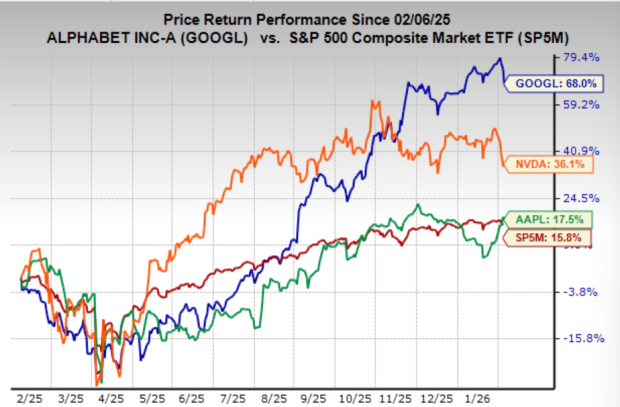

Over the past year, Alphabet has notably outperformed most of its Magnificent Seven counterparts, a cohort that has quietly seen more mixed performance than headlines might suggest. Even strong performers such as Nvidia (NVDA) and Apple (AAPL) have trailed Alphabet by a meaningful margin.

Alphabet has transitioned from an undervalued opportunity to a premium multiple stock. Shares currently trade around 30.1xforward earnings, above the company’s five-year median but still reasonable given its growth profile, diversified business offerings and industry dominance.

For context, several mega-cap peers command even higher valuations. Nvidia trades near 39.3x forward earnings, while Apple sits around 33.1x.

Perhaps the most important data point in the release was 17% growth in Search. For much of the past year, investors debated whether generative AI would cannibalize Google’s core business. Instead, the opposite appears to be unfolding.

AI is driving greater user engagement, higher query volume and improved monetization, suggesting Search is entering an expansionary phase rather than facing disruption. For a business that still represents Alphabet’s economic engine, this development should reassure long-term investors.

Google Cloud posted an impressive 48% growth rate alongside expanding margins, signaling that the segment has moved beyond the “prove-it” stage. Enterprise demand tied to AI workloads continues to accelerate, strengthening Google’s position alongside industry leaders Amazon Web Services and Microsoft Azure.

Cloud is increasingly central to Alphabet’s investment thesis, providing both diversification beyond advertising and a powerful platform for AI deployment.

Alphabet is also beginning to quantify traction in generative AI. The Gemini app now boasts roughly 750 million monthly active users, while the company is processing approximately 10 billion tokens per minute through its API.

Meanwhile, YouTube has quietly grown into a media powerhouse, generating more than $60 billion in annual revenue across advertising and subscriptions. The company also reported 325 million paid subscriptions across consumer services, further reinforcing the durability of its ecosystem and reducing reliance on a single revenue stream.

Management guided toward $175 billion to $185 billion in capital expenditures for 2026 — a figure that approaches half of current annual revenue. While striking, the aggressive spending plan reflects Alphabet’s determination to lead the AI infrastructure buildout rather than follow it.

The company maintains a fortress balance sheet, though investors should note that approximately $25 billion in additional debt was added, indicating Alphabet is willing to lever modestly to fund its next phase of growth.

Despite its operational momentum, near-term stock performance could remain sensitive to broader market conditions, particularly if volatility persists across technology and AI equities.

Still, the latest results reinforce a central takeaway: Alphabet is executing at an exceptionally high level across its core businesses while simultaneously investing for the next era of computing. Few companies possess the scale, technical leadership and platform reach that Alphabet commands today.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| 4 hours | |

| 6 hours | |

| 7 hours | |

| 8 hours | |

| 8 hours | |

| 10 hours | |

| Jul-25 | |

| Jul-25 | |

| Jul-25 | |

| Jul-25 | |

| Jul-25 | |

| Jul-25 | |

| Jul-25 | |

| Jul-25 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite