|

|

|

|

|||||

|

|

|

Post Holdings, Inc. POST reported fiscal first-quarter 2026 results, wherein both the top and bottom lines increased year over year and came ahead of their respective Zacks Consensus Estimate.

The company reported adjusted earnings of $2.13 per share, beating the Zacks Consensus Estimate of $1.66. The bottom line increased from the adjusted earnings of $1.73 per share recorded in the year-ago quarter.

Post Holdings, Inc. price-consensus-eps-surprise-chart | Post Holdings, Inc. Quote

Net sales reached $2,174.6 million, reflecting an 10.1% increase year over year, which includes $224.6 million from acquisitions. Excluding acquisitions, Foodservice and Weetabix delivered organic growth, while Post Consumer Brands reported a decline and Refrigerated Retail was flat year over year. The net sales came in slightly higher than the Zacks Consensus Estimate of $2,165 million.

The gross profit of $638.5 million increased 7.3% year over year, while the gross margin contracted slightly to 29.4% from 30.1%.

Selling, general and administrative (SG&A) expenses increased 7.8% to $357.3 million. As a percentage of net sales, the metric was 16.4% compared with 16.8% reported in the year-ago period. SG&A expenses for the quarter included $4.3 million in integration costs primarily related to acquisitions.

The operating profit registered an increase of 11.3% to $238.4 million. The adjusted EBITDA was $418.2 million, an increase of 13.1% from $369.9 million in the year-ago quarter.

Post Consumer Brands: The segment reported net sales of $1,103.8 million, up 14.5% year over year. Results included $217.2 million attributable to 8th Avenue. Excluding this contribution, volumes declined 6.1% year over year. Pet food volumes fell 6.2% year over year, caused by reduced private-label and co-manufactured output, as well as distribution losses. Cereal and granola volumes decreased 5.1% year over year, pressured by overall category weakness and the decline in relative and absolute promotional activity. Segment profit rose 0.9% to $132.2 million, while adjusted EBITDA declined 0.7% to $203.3 million.

Foodservice: The segment net sales grew 8.5% year over year to $669.1 million. The quarter included a $6.6 million contribution from PPI. Excluding this benefit, volumes increased 7.7% year over year, supported by better production in protein-based shakes and customer service levels. Segment profit surged 36.5% year over year to $117.5 million, and adjusted EBITDA increased 30.5% year over year to $152.4 million.

Refrigerated Retail: The segment reported net sales of $266.6 million, unchanged from the prior year. Volumes declined 0.2% year over year, primarily caused by weakness in sausage and egg products, with an increase in side dish products due to the introduction of private label offerings partially offsetting the decline. Segment profit rose 25.6% year over year to $30.4 million, while adjusted EBITDA grew 20.4%year over year to $50.1 million.

Weetabix: The segment delivered net sales of $137.9 million, up 8.1% year over year. Results included a foreign-currency tailwind of roughly 400 basis points. Volumes rose 2.4% year over year, reflecting an increase in protein-based shakes and branded products. Segment profit rose 36.5% year over year to $21.7 million, while adjusted EBITDA rose 18.2% year over year to $33.1 million.

Post Holdings ended the quarter with cash and cash equivalents of $279.3 million, long-term debt of $7,457.9 million and total shareholders’ equity of $3,468.1 million.

In the first quarter of fiscal 2026, Post Holdings repurchased 3.7 million shares for $378.9 million. After the fiscal first-quarter end, the company repurchased 1.8 million shares for $175.4 million through Feb. 4, 2026. On Feb. 3, 2026, POST approved a new $500 million buyback program.

Post Holdings now expects adjusted EBITDA in the range of $1,550-$1,580 million, revised up from the previously guided range of $1,500-$1,540 million. Capital expenditures for the fiscal year are still expected to be in the previously guided range of $350 million to $390 million, reflecting continued investment in cage-free egg facility expansion and the completion of the precooked egg facility expansion in Iowa, Norwalk, totaling $80-$90 million.

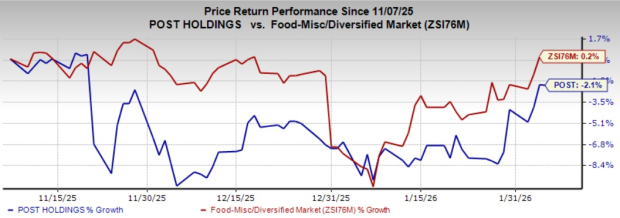

This Zacks Rank #4 (Sell) company’s shares have lost 2.1% in the past three months against the industry’s rise of 0.2%.

The Simply Good Foods Company SMPL, a consumer-packaged food and beverage company, engages in the development, marketing, and sale of snacks and meal replacements, and other products in North America and internationally. SMPL currently flaunts a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for Simply Good Foods' current fiscal-year sales implies a decline of 0.3%, and the same for current fiscal-year earnings implies growth of 1.6% from the year-ago reported figures. SMPL delivered a trailing four-quarter earnings surprise of 5.53%, on average.

Kimberly-Clark Corporation KMB, together with its subsidiaries, manufactures and markets personal care products in the United States. KMB currently carries a Zacks Rank #2 (Buy).

The Zacks Consensus Estimate for Kimberly-Clark's current fiscal-year sales and earnings implies a decline of 2.1% and 6.2%, respectively, from the year-ago actuals. KMB delivered a trailing four-quarter earnings surprise of 18.9%, on average.

Medifast, Inc. MED, through its subsidiaries, operates as a health and wellness company that provides habit-based and coach-guided lifestyle solutions to address obesity and support a healthy life in the United States. MED currently carries a Zacks Rank #2.

The Zacks Consensus Estimate for Medifast's current fiscal-year sales and earnings implies a decline of 36.7% and 156.5%, respectively, from the year-ago actuals. MED delivered a trailing four-quarter negative earnings surprise of 640%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-07 | |

| Aug-06 | |

| Aug-06 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 | |

| Aug-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite