|

|

|

|

|||||

|

|

|

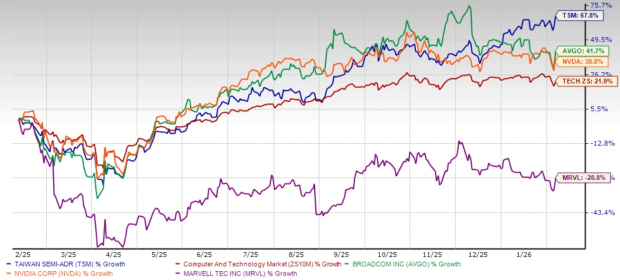

Taiwan Semiconductor Manufacturing Company TSM, also known as TSMC, has delivered a robust 67.8% gain over the past 12 months. The stock has been benefiting from the AI boom by manufacturing advanced chips for major AI clients like NVIDIA NVDA, Broadcom AVGO and Marvell Technology MRVL, which has led to record profits and a significant increase in revenues.

Shares of the company have outperformed the Zacks Computer and Technology sector’s gain of 27.9% over the past year. Taiwan Semiconductor is also among the top-performing semiconductor stocks, including Broadcom, NVIDIA and Marvell Technology. Over the past year, shares of Broadcom and NVIDIA have soared 41.7 % and 38.8%, respectively, while Marvell Technology has declined 28.8%.

This outperformance shows investors are becoming increasingly confident in Taiwan Semiconductor’s long-term story, even during a volatile market shaped by trade conflicts and geopolitical risks. We believe this momentum is grounded in strong fundamentals, and TSMC’s long-term outlook justifies a buy position for now.

Taiwan Semiconductor continues to lead the global chip foundry market. Its scale and technology make it the first choice for companies driving the AI boom. NVIDIA, Marvell and Broadcom all count on TSMC to build advanced graphics processing units (GPUs) and AI accelerators.

AI-related chip sales have become a major driver. In 2025, high-performance computing (HPC), which includes AI-related revenues, accounted for 58% of total revenues, up from 51% in 2024. Taiwan Semiconductor’s long-term forecasts depict that the momentum is far from over. Management expects AI revenues to increase at a CAGR of more than 50% in the five-year period from 2024 to 2029. That makes TSMC central to the AI supply chain.

To keep up with the growing demand for AI chips, Taiwan Semiconductor is spending aggressively. The company is set to invest between $52 billion and $56 billion in capital expenditures in 2026, far outpacing its $40.9 billion investment in 2025. The bulk of this spending is focused on advanced manufacturing processes, ensuring TSMC remains ahead of rivals in the chip manufacturing space.

TSM’s Resilient Financial Performance

Taiwan Semiconductor’s latest earnings report highlights just how dominant the company remains. In the recently concluded financial cycle for 2025, TSMC’s revenues jumped 35.9% year over year to $122.42 billion, while earnings per share (EPS) soared 51.3% to $10.65. This growth was powered by the booming demand for its advanced 3nm and 5nm nodes, which now account for more than 60% of total wafer sales. Gross margins improved 380 basis points to 59.9%, reflecting better cost efficiencies.

Taiwan Semiconductor Manufacturing Company Ltd. price-consensus-eps-surprise-chart | Taiwan Semiconductor Manufacturing Company Ltd. Quote

Buoyed by strong demand for its 3nm and 5nm chips, Taiwan Semiconductor anticipates continued revenue growth momentum in 2026. The company now forecasts 2026 revenues to increase approximately 30%. The Zacks Consensus Estimate for full-year 2026 revenues is pegged at $158.2 billion, indicating year-over-year growth of 29.2%.

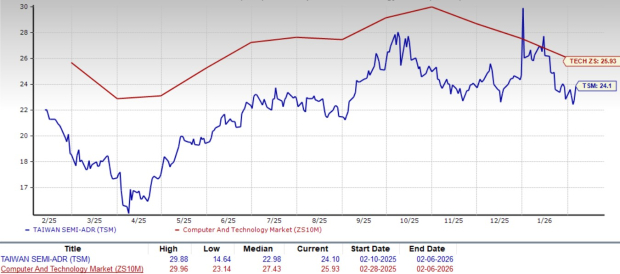

Despite a robust rally, Taiwan Semiconductor stock still looks reasonably priced. It trades at a forward 12-month price-to-earnings (P/E) multiple of 24.1, which is lower than the sector average of 25.93. This discount adds to the appeal for long-term investors.

Compared with other major semiconductor players, Taiwan Semiconductor has a lower P/E ratio than Broadcom and NVIDIA but a higher valuation than Marvell Technology. Currently, Broadcom, NVIDIA and Marvell Technology trade at P/E multiples of 29.55, 25.22 and 22.59, respectively.

Taiwan Semiconductor remains a cornerstone of the semiconductor industry. Its unmatched capabilities in advanced chip manufacturing, strong exposure to AI demand and expanding capacity give it a solid long-term trajectory. Given its valuation and growth backdrop, buying the stock makes the most sense right now.

Currently, Taiwan Semiconductor sports a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 1 hour | |

| 1 hour | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite