|

|

|

|

|||||

|

|

|

Solid-state battery innovator QuantumScape Corp. QS is slated to release fourth-quarter 2025 results on Feb. 11, after market close. The Zacks Consensus Estimate for the to-be-reported quarter’s loss per share is pegged at 16 cents. The loss estimate for the to-be-reported quarter has remained stable over the past 60 days and implies an improvement from the year-ago period’s loss of 22 cents per share.

For 2025, the Zacks Consensus Estimate pegs QuantumScape’s loss at 75 cents per share, implying a 17% year-over-year improvement. For 2026, the consensus calls for a further narrowing of losses to 63 cents per share. Over the past four quarters, QuantumScape beat bottom-line estimates once and met expectations in the remaining three quarters.

Our proprietary model does not conclusively predict an earnings beat for QuantumScape this earnings season. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the odds of an earnings beat. That’s not the case here. You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

QS has an Earnings ESP of 0.00% and a Zacks Rank #3.

You can see the complete list of today’s Zacks #1 Rank stocks here.

QuantumScape’s fourth-quarter results are expected to reflect steady operational progress and early signs of commercialization. A key development is the commencement of shipment of its latest solid-state lithium-metal cells built using the Cobra separator process. Management has confirmed that multiple OEM partners are actively evaluating these B1 cells, indicating rising engagement and growing confidence in QuantumScape’s technology roadmap.

Another important signal came in the third quarter of 2025, when QuantumScape reported $12.8 million in customer billings. These billings, primarily tied to joint development work with Volkswagen’s VWAGY PowerCo, mark early commercial activity. While the company does not yet recognize these billings as revenues, the metric is meaningful for investors. It shows that automakers are willing to pay for QuantumScape’s development efforts, supporting the viability of its capital-light, licensing-focused business model.

The progress is further reinforced by a major operational milestone achieved in December. The company completed the installation of core equipment at its Eagle Line pilot production facility in San Jose, which was formally inaugurated last week.

The Eagle Line integrates QuantumScape’s Cobra process, which is roughly 25 times more productive than the earlier Raptor line. After shipping initial Cobra-built B1 samples, the Eagle Line now enables higher-volume production, strengthening QuantumScape’s ability to support partner evaluations and future scale-up efforts.

Shares of QS have declined 48% over the past three months, underperforming the industry.

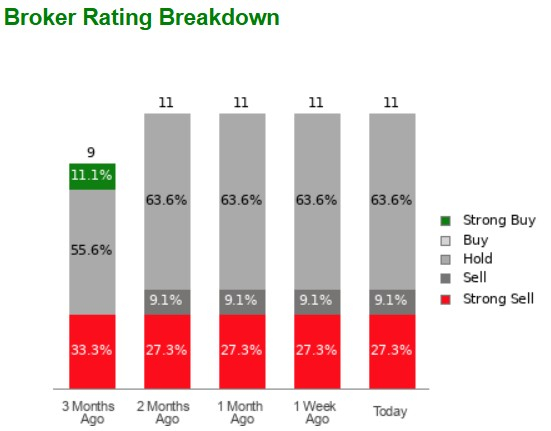

QuantumScape currently has an average brokerage recommendation (ABR) of 3.64 on a scale of 1 to 5 (Strong Buy to Strong Sell), calculated based on the actual recommendations (Buy, Hold, Sell, etc.) made by 11 brokerage firms.

Last year, the company moved closer to real-world validation, achieving a series of operational, technology and partnership milestones. A major breakthrough was the advancement of its Cobra separator process, which materially improves productivity and supports higher-volume manufacturing.

Partnership momentum has also picked up. Volkswagen’s PowerCo remains a central pillar of the story. In July, PowerCo committed up to $131 million in milestone-based payments over the next two years to support development of the QSE-5 pilot line in San Jose, following an earlier $130 million licensing agreement. These commitments underscore Volkswagen’s long-term belief in QuantumScape’s technology. The start of B1 sample deliveries and the first customer billings reported in the third quarter marked another turning point, signaling early steps toward monetization.

QuantumScape’s progress was visibly showcased at the IAA Mobility Show in Munich, where the company and Volkswagen unveiled a Ducati V21L motorcycle powered by QSE-5 cells. Operationally, the completion and inauguration of the Eagle Line pilot facility now shift the focus toward ramping output and refining manufacturing processes. Joint development agreements with two additional global automakers and partnerships with Murata Manufacturing and Corning to enable high-volume ceramic separator production also bode well.

That said, risks remain. QuantumScape continues to burn cash, is yet to reach full-scale production, and its stock already doubled in 2025, suggesting that much of the optimism may be priced in. While the recent pullback looks reasonable, the shares are not clearly undervalued. The stock carries a Value Score of F.

For existing investors, continued execution supports staying invested, while new entrants may prefer to wait for a better entry point and more clarity.

Key watchpoints from the upcoming earnings release include updates on Cobra-based sample shipments, as well as progress on licensing and monetization. Any clearer guidance on when QSE-5 transitions from pilot production to pre-commercial scale will be critical in shaping long-term revenue expectations.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Jul-14 | |

| Jul-08 | |

| Jul-07 | |

| Jun-25 | |

| Jun-22 | |

| Jun-18 | |

| Jun-18 | |

| Jun-18 | |

| Jun-18 | |

| Jun-08 | |

| May-13 | |

| May-13 | |

| May-08 | |

| Apr-30 | |

| Apr-24 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite