|

|

|

|

|||||

|

|

|

Sally Beauty Holdings, Inc. SBH reported fiscal first-quarter 2026 results, wherein the top line came slightly below the Zacks Consensus Estimate, while the bottom line beat the Zacks Consensus Estimate. Both increased year over year.

Sally Beauty’s adjusted earnings were 48 cents per share, which came above the Zacks Consensus Estimate of 47 cents. The metric increased 12% from 43 cents per share in the year-ago period.

Sally Beauty Holdings, Inc. price-consensus-eps-surprise-chart | Sally Beauty Holdings, Inc. Quote

The company reported consolidated net sales of $943 million compared with the Zacks Consensus Estimate of $944 million. The metric increased 0.6% from $937.9 million posted in the year-ago period. Consolidated comparable sales remained flat year over year.

Global e-commerce sales grew 11% to $111 million, forming 11.7% of total net sales.

The company’s adjusted gross margin expanded 50 basis points to 51.3%. Adjusted selling, general and administrative expenses rose to $404 million, up $6 million from last year.

Adjusted operating earnings were $80 million, which came at the higher end of the management’s guidance. The adjusted operating margin was at 8.5%.

Sally Beauty Supply: Net sales in this segment rose 1.2% year over year to $531.6 million. Comparable sales climbed 0.1%, while the operating margin declined by 50 basis points to 14.7%. The segment’s gross margin expanded 20 basis points to 59.8%.

Beauty Systems Group: Net sales declined 0.2% to $411.6 million. Comparable sales were down 0.2%, while the operating margin expanded 90 basis points to 13.1%, supported by a 50-basis-point improvement in gross margin to 40.2%.

SBH ended the fiscal first quarter with cash and cash equivalents of $157.2 million, long-term debt, including capital leases of $842.5 million and total stockholders’ equity of $823.6 million.

In the fiscal first quarter, cash flow from operations was $93 million, with free cash flow of $57 million. The company used cash to repay $20 million of term loan B debt and repurchased 1.4 million shares for $21 million, ending the quarter with net debt leverage of 1.5x.

The company raised the lower end of its fiscal 2026 EPS guidance. It now anticipates adjusted EPS of $2.02-$2.10 compared with the earlier view of $2.00-$2.10. Management expects consolidated net sales of $3.71-$3.77 billion and comparable sales growth is expected to be flat to up 1%. Adjusted operating earnings are anticipated to come in the range of $328-$342 million. Free cash flow is projected at $200 million, with roughly half allocated to capital expenditures of about $100 million.

For the second quarter of fiscal 2026, consolidated net sales are guided to be $895-$905 million, with comparable sales growth of 0.5-1.5%. Adjusted operating earnings are projected in the band of $68-$71 million, with SG&A returning to a more normalized quarterly pattern and stable expense trends over a two-year period. Adjusted EPS is expected to be 39-42 cents for the second quarter.

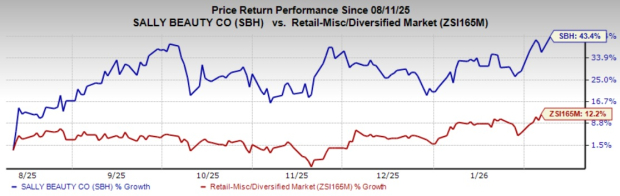

This Zacks Rank #3 (Hold) stock has lost 43.4% in the past six months against the industry’s growth of 12.2%.

Five Below, Inc. FIVE operates as a specialty value retailer in the United States. At present, Five Below currently sports a Zacks Rank of 1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for FIVE’s current fiscal-year sales and earnings implies growth of 22.4% and 25.8%, respectively, from the year-ago figures. FIVE delivered a trailing four-quarter earnings surprise of 62.1%, on average.

American Eagle Outfitters, Inc. AEO operates as a specialty beauty retailer in the United States, Mexico and Kuwait. At present, AEO flaunts a Zacks Rank of 1.

The Zacks Consensus Estimate for AEO’s current fiscal-year sales implies growth of 2.5%, and the same for earnings indicates a decline of 20.7% from the year-ago figures. American Eagle delivered a trailing four-quarter earnings surprise of 35.1%, on average.

Deckers Outdoors Corporation DECK, together with its subsidiaries, designs, markets and distributes footwear, apparel, and accessories for casual lifestyle use and high-performance activities in the United States and internationally. At present, Deckers sports a Zacks Rank of 1.

The Zacks Consensus Estimate for DECK’s current fiscal-year sales and earnings indicates growth of 8.5% and 7.9%, respectively, from the year-ago figures. DECK delivered a trailing four-quarter earnings surprise of 36.9%, on average.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 2 hours | |

| Jul-21 | |

| Jul-21 | |

| Jul-21 | |

| Jul-15 | |

| Jul-13 | |

| Jul-13 | |

| Jul-13 | |

| Jul-13 | |

| Jul-13 | |

| Jul-09 | |

| Jul-09 | |

| Jul-09 | |

| Jul-03 | |

| Jul-03 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite