|

|

|

|

|||||

|

|

|

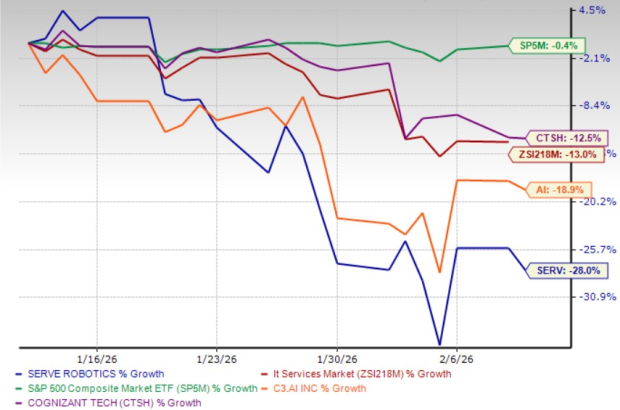

Shares of Serve Robotics Inc. SERV have plunged 28% over the past month, sharply underperforming the broader industry’s 13% decline and the S&P 500's 0.4% dip.

The pullback comes despite the company delivering triple-digit revenue growth, crossing the 1,000-robot deployment milestone and reiterating confidence in a steep revenue ramp in 2026. With management touting accelerating fleet expansion, improving utilization and a targeted $60–$80 million annualized run-rate ahead, investors are weighing whether the recent selloff reflects short-term volatility or signals deeper execution and profitability risks.

The stock has underperformed its industry peers, including C3.ai, Inc. AI and Cognizant Technology Solutions Corporation CTSH, down 18.9% and 12.5%, respectively, in the same time frame.

Serve Robotics’ recent 28% slide reflects a widening gap between ambitious long-term targets and near-term financial realities. While management highlighted rapid fleet expansion and a milestone of more than 1,000 deployed robots, revenue remains modest relative to spending. In third-quarter 2025, total revenue was just $687,000, even as GAAP operating expenses reached $30.4 million and adjusted EBITDA was negative $24.9 million. That imbalance underscores that Serve Robotics is still deeply in investment mode, prioritizing scale and infrastructure over profitability, a dynamic that can pressure sentiment, particularly in a risk-off market environment.

Another factor weighing on the stock is the heavy cash burn tied to expansion and acquisitions. The company continues to invest aggressively in R&D, which totaled $13.4 million in third-quarter 2025 on a GAAP basis, alongside spending on new market launches and M&A integrations. While management argues these investments will drive efficiency gains in 2026 and beyond, investors appear concerned about execution risk and the time required to translate technological progress into sustainable margins. The integration of Vayu Robotics, for instance, is still in early stages, and management acknowledged that it will take months before measurable autonomy benefits are visible.

Finally, expectations may have gotten ahead of fundamentals. Serve Robotics reaffirmed its goal of reaching a $60 million to $80 million annualized revenue run rate but indicated it is more than 12 months away. Full-year 2025 revenue guidance is just over $2.5 million, highlighting the steep growth curve required. With valuation largely tied to future scale, any doubts around utilization improvements, timing of revenue acceleration, or broader capital market conditions can amplify downside volatility, explaining why investors have turned cautious despite strong operational milestones.

Serve Robotics’ operational momentum remains strong despite the stock’s pullback. The company surpassed 1,000 deployed robots and is on track to reach 2,000 by year-end, a scale milestone management views as a tipping point for better utilization and efficiency. Delivery volumes jumped 66% sequentially in third-quarter 2025, restaurant partnerships rose 45% quarter over quarter to more than 3,600 locations and average daily operating hours per robot increased 12.5%, reflecting improving productivity and autonomy. These trends suggest stronger revenue generation per robot as the fleet expands.

Strategically, the DoorDash partnership broadens market reach and enables multi-platform utilization alongside Uber, which can enhance asset efficiency and delivery density. The Vayu acquisition is expected to accelerate AI model improvements and operational gains over time. With $211 million in cash and no debt, plus management targeting a $60–$80 million annualized revenue run rate beyond 2026, Serve Robotics has both the liquidity and roadmap to support long-term growth.

Serve Robotics’ 2026 loss per share estimates have widened from $1.79 to $1.83 over the past 60 days. This downward trend reflects weakening analyst confidence in the stock’s near-term prospects.

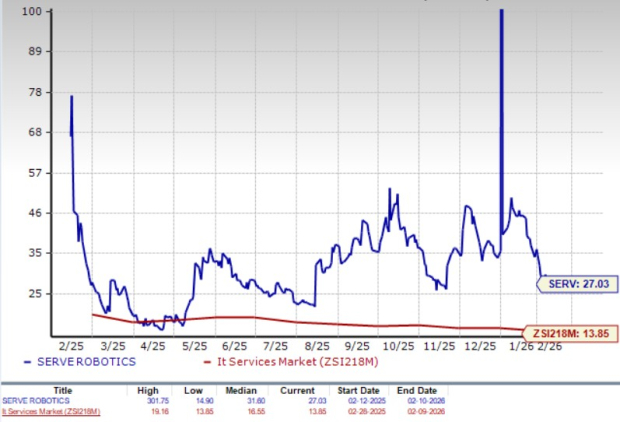

Serve Robotics stock is currently trading at a premium. SERV is currently trading at a forward 12-month price-to-sales (P/S) multiple of 27.03X, well above the industry average of 13.85X. Other industry players, such as C3.ai and Cognizant, have P/S of 4.98X and 1.61X, respectively.

Serve Robotics’ sharp pullback appears driven more by near-term financial strain and valuation concerns than by a breakdown in its long-term growth story. The company is clearly still in heavy investment mode, with spending far outpacing current revenue as it scales its fleet, enhances autonomy and integrates acquisitions.

While operational metrics such as expanding deployments, rising utilization and deeper platform partnerships signal meaningful progress, profitability remains distant and earnings expectations continue to drift lower. Given the premium valuation and execution risks tied to converting scale into sustainable margins, existing investors can consider holding the stock for its long-term automation opportunity and strong liquidity position, but fresh buying may be best deferred until revenue acceleration becomes more visible and losses show a clearer path toward narrowing.

SERV currently carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| Aug-06 | |

| Aug-05 | |

| Aug-04 | |

| Aug-04 | |

| Aug-01 | |

| Jul-31 | |

| Jul-31 | |

| Jul-31 | |

| Jul-30 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 | |

| Jul-29 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite