|

|

|

|

|||||

|

|

|

Tempus AI TEM is slated to release fourth-quarter 2025 results on Feb. 24, after market close. During the quarter, the company advanced several strategic collaborations and product innovations that are expected to further strengthen its performance in 2026. The company released preliminary, unaudited fourth-quarter and full-year 2025 results on Jan. 11, 2026.

Per the preliminary announcement, revenues reached approximately $1.27 billion for the full year, reflecting a roughly 83% year-over-year increase, including about 30% organic growth (excluding Ambry).

Diagnostics revenues totaled approximately $955 million, up about 111% year over year, driven by oncology volume growth of approximately 26% and hereditary testing volume increase of around 29%. Data and applications revenues reached roughly $316 million, reflecting 31% growth year over year, fueled in part by an approximately 38% improvement in its Insights (data licensing) business.

According to the preliminary announcement, the company noted that its 2025 top line exceeded its initial expectations, with diagnostics achieving the highest oncology unit growth rate seen in years and accelerating for the third consecutive quarter. Meanwhile, the data and applications segment delivered record fourth-quarter revenues of approximately $100 million and full-year growth of about 31%, with data licensing expanding approximately 38%.

Tempus’ peers like Doximity, Inc. DOCS and Azenta, Inc. AZTA have also posted their quarterly results.

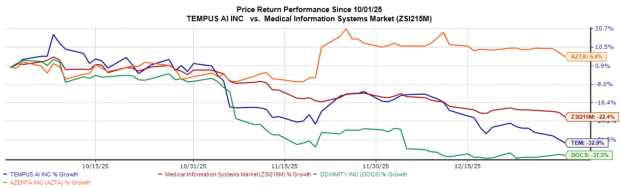

During the fourth quarter, TEM’s shares have plunged 32.9%, reflecting a sharp reversal in sentiment across the AI in medtech space. The stock’s decline is broadly in line with DOCS, down 37.3% over the same period. AZTA has fared relatively better, posting a single-digit gain of about 5.4%. The Zacks Medical Info Systems industry has lost 22.4% over the same period.

Image Source: Zacks Investment Research

Tempus has strengthened its strategic collaboration efforts through two notable partnerships aimed at advancing oncology research and precision medicine. The company entered a multi-year collaboration with Whitehawk Therapeutics, Inc. WHWK.

Under the agreement, Whitehawk will leverage Tempus’ proprietary, de-identified multimodal real-world dataset to advance biomarker-driven research and optimize clinical trial design. The collaboration is designed to enhance trial efficiency and support the development of Whitehawk’s oncology pipeline.

Tempus initiated a new research study, conducted in collaboration with the Institute for Follicular Lymphoma Innovation (“IFLI”), a global nonprofit foundation dedicated to accelerating innovative treatment options for patients with follicular lymphoma (FL). This engagement marks Tempus’ first study collaboration with a nonprofit foundation to create robust FL dataset. This study will also provide critical insights to inform the development and validation of comprehensive whole-genome sequencing approaches.

Tempus recorded Total Contract Value (“TCV”) of more than $1.1 billion as of Dec. 31, 2025. It signed data agreements with more than 70 customers across large and mid-sized pharmaceutical companies, including AstraZeneca, Pfizer and Eli Lilly. Financially, for the first time, Tempus reported positive adjusted EBITDA of $1.5 million in the third quarter of 2025. This represented a year-over-year improvement of $23.3 million.

In May, Tempus announced participation in nearly 1,500 research projects over the past decade. Leveraging the company’s AI-powered platform, it offers comprehensive suites of solutions supporting both clinical and therapeutic research.

Notable contributions include enabling approximately 1,000 biopharma-led research projects and nearly 500 provider-led initiatives through its diagnostic portfolio, de-identified multimodal datasets and biological modeling capabilities. Tempus’ diagnostic assays have generated clinically relevant insights across more than 200 projects, while its biological modeling laboratory has supported approximately 65 research initiatives.

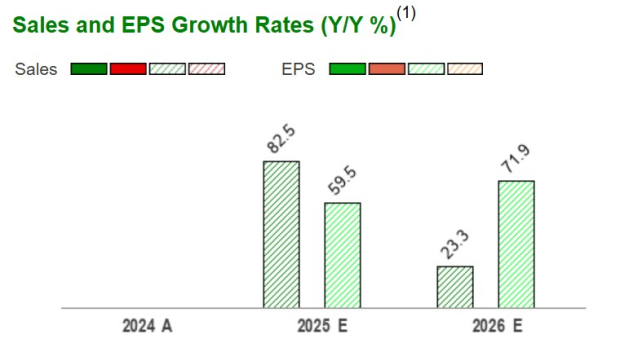

Per the Zacks Consensus Estimate, Tempus is expected to experience a huge 82.5% improvement in 2025 revenues. Earnings per share are expected to remain negative, but up 59.5% over 2024.

Image Source: Zacks Investment Research

Despite achieving positive adjusted EBITDA, GAAP losses persisted, reflecting substantial stock-based compensation, higher amortization of acquired intangibles related to the Ambry transaction, and a one-time loss associated with debt extinguishment. As a result, non-GAAP profitability continues to rely on adjustments that exclude significant and recurring non-cash items.

The absence of GAAP net loss guidance limits visibility into the timeline for achieving sustainable GAAP profitability. The current profitability inflection thesis remains largely non-GAAP-driven in the near term.

Although Tempus has developed and published several advanced AI-driven diagnostic algorithms, the absence of reimbursement frameworks for such tools within the U.S. healthcare system poses a significant structural hurdle. Due to this, the company’s AI business looks promising but unlikely to generate large revenues in the near term until payers adopt consistent reimbursement policies.

Tempus stock is not so cheap, as suggested by the Value Score of F.

The stock is currently trading at a price-to-book (P/B) ratio of 17.79X, which is higher than the industry average of 8.76X.

Image Source: Zacks Investment Research

Tempus continues to position itself as a high-growth, data-driven leader at the intersection of AI and precision medicine. Per unaudited preliminary results, the company delivered exceptional top-line expansion, accelerated diagnostics volumes and delivered record performance in its data and applications segment. Strategic collaborations, along with deepening relationships with major biopharma players, reinforce the strength and scalability of its platform. The company’s expanding Total Contract Value, improving adjusted EBITDA profile and robust revenue outlook underscore meaningful operational momentum in 2026.

TEM, carrying a Zacks Rank #4 (Sell) at present, already trades at elevated levels. Currently, the stock appears more appropriate for observation than aggressive buying. Investors who already have this stock in their portfolios are advised to maintain their position. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

This article originally published on Zacks Investment Research (zacks.com).

| 38 min | |

| 9 hours | |

| Aug-04 | |

| Aug-04 | |

| Aug-04 | |

| Jul-31 | |

| Jul-31 | |

| Jul-30 | |

| Jul-30 | |

| Jul-24 | |

| Jul-24 | |

| Jul-22 | |

| Jul-22 | |

| Jul-21 | |

| Jul-21 |

Join thousands of traders who make more informed decisions with our premium features. Real-time quotes, advanced visualizations, alerts, and much more.

Learn more about Finviz Elite